Vous aimerez peut-être aussi

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

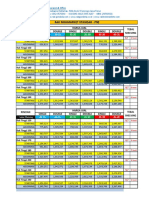

- Rak Minimarket Standar - P90: Single Double Single Double Single Double Rincian Harga Jual Tebal ShelvingDocument6 pagesRak Minimarket Standar - P90: Single Double Single Double Single Double Rincian Harga Jual Tebal ShelvingAndi HadisaputraPas encore d'évaluation

- Resume Vikas SAP SDDocument2 pagesResume Vikas SAP SDVikas AnandPas encore d'évaluation

- ApekshaDocument2 pagesApekshaShubh TripathiPas encore d'évaluation

- Inv 10 CH QDocument15 pagesInv 10 CH QSrini KumarPas encore d'évaluation

- 01 - SAP System ArchitectureDocument56 pages01 - SAP System ArchitectureDinbandhu TripathiPas encore d'évaluation

- CNS-223-1I Implement Citrix ADC 13.x: Getting Started Lab ManualDocument24 pagesCNS-223-1I Implement Citrix ADC 13.x: Getting Started Lab ManualМаријан СтанићPas encore d'évaluation

- Excel Lesson PDFDocument30 pagesExcel Lesson PDFNergiz MemmedzadePas encore d'évaluation

- Alert System For Fishermen Crossing Border PDFDocument5 pagesAlert System For Fishermen Crossing Border PDFtechmindzPas encore d'évaluation

- 360.88 Virtual Teams 2Document8 pages360.88 Virtual Teams 2karyna the educatorPas encore d'évaluation

- ANSYS Fluent Migration Manual 16.0Document38 pagesANSYS Fluent Migration Manual 16.0hafidzfbPas encore d'évaluation

- Assignment # 1Document4 pagesAssignment # 1Asad SarwarPas encore d'évaluation

- Assignment (Data Models of DBMS)Document5 pagesAssignment (Data Models of DBMS)sumaira shabbirPas encore d'évaluation

- Offset PrintingDocument5 pagesOffset PrintingajiitrPas encore d'évaluation

- India Insurance Perspective PDFDocument24 pagesIndia Insurance Perspective PDFaishwarya raikarPas encore d'évaluation

- Machine Learning Driven Interpretation of Computational Uid Dynamics Simulations To Develop Student IntuitionDocument1 pageMachine Learning Driven Interpretation of Computational Uid Dynamics Simulations To Develop Student IntuitionADVOKASI PPI MALAYSIAPas encore d'évaluation

- OchureDocument15 pagesOchurePrincipal MsecPas encore d'évaluation

- 2014 Axeda Stack Image FileDocument1 page2014 Axeda Stack Image FileCasey LeePas encore d'évaluation

- LogDocument11 pagesLogFarrel NevlinPas encore d'évaluation

- Automation KivaDocument25 pagesAutomation KivaAnirudh KowthaPas encore d'évaluation

- List of Experiments and Record of Progressive Assessment: Date of Performance Date of SubmissionDocument37 pagesList of Experiments and Record of Progressive Assessment: Date of Performance Date of SubmissionIqbal HassanPas encore d'évaluation

- Dowody Do SkargiDocument6 pagesDowody Do Skargisimom 123Pas encore d'évaluation

- CoWIN OverviewDocument26 pagesCoWIN OverviewAfroz AlamPas encore d'évaluation

- CH 3 SQLDocument44 pagesCH 3 SQLRobel HaftomPas encore d'évaluation

- Tokenization Everything You Need To KnowDocument21 pagesTokenization Everything You Need To KnowJose Alberto Lopez PatiñoPas encore d'évaluation

- Dog Breed Classificationusing Convolutional Neural NetworkDocument54 pagesDog Breed Classificationusing Convolutional Neural NetworkLike meshPas encore d'évaluation

- Verilog A Model To CadenceDocument56 pagesVerilog A Model To CadenceJamesPas encore d'évaluation

- Basic Fonts1 - DafontDocument12 pagesBasic Fonts1 - DafontTech StarPas encore d'évaluation

- Intercopmany IdocDocument24 pagesIntercopmany Idocnelsondarla12Pas encore d'évaluation

- Csc101 Ict Lab Manual v2.0Document117 pagesCsc101 Ict Lab Manual v2.0Asjad HashmiPas encore d'évaluation

- Intersecting Surfaces and SolidsDocument5 pagesIntersecting Surfaces and Solidswallesm123Pas encore d'évaluation