Vous aimerez peut-être aussi

- Reddit - FAR NotesDocument232 pagesReddit - FAR Notesneha jainPas encore d'évaluation

- Accounting Principles Volume 1 Canadian 7th Edition Geygandt Solutions ManualDocument93 pagesAccounting Principles Volume 1 Canadian 7th Edition Geygandt Solutions Manualgeralddiaznqmcrpgodk100% (12)

- Blocher8e EOC SM Ch04 FinalDocument46 pagesBlocher8e EOC SM Ch04 FinalDiah ArmelizaPas encore d'évaluation

- Bain Interactive Interview Briefing PackDocument19 pagesBain Interactive Interview Briefing PackDavid MiguelPas encore d'évaluation

- Project For Business Finance - Qantas Airways and Ausenco LTDDocument32 pagesProject For Business Finance - Qantas Airways and Ausenco LTDBabur FarrukhPas encore d'évaluation

- Capital Budgeting Techniques PDFDocument57 pagesCapital Budgeting Techniques PDFMecheal ThomasPas encore d'évaluation

- Risk and Rate of ReturnDocument67 pagesRisk and Rate of ReturnHONG RY80% (5)

- Asset Pricing ModelDocument15 pagesAsset Pricing ModelEnp Gus AgostoPas encore d'évaluation

- Activity Guide D102261 PDFDocument170 pagesActivity Guide D102261 PDFmanpreetgilPas encore d'évaluation

- Target CostingDocument4 pagesTarget CostingPriya KudnekarPas encore d'évaluation

- Chapter 4 DerivativesDocument38 pagesChapter 4 DerivativesTamrat KindePas encore d'évaluation

- Transfer PricingDocument57 pagesTransfer PricingbijoyendasPas encore d'évaluation

- Cost ManagementDocument18 pagesCost ManagementGeo Rublico ManilaPas encore d'évaluation

- KOCH6Document63 pagesKOCH6Swati SoniPas encore d'évaluation

- Cost Benefit AnalysisDocument99 pagesCost Benefit AnalysisAmulay OberoiPas encore d'évaluation

- 1 Verification of Opening Balances 0fDocument21 pages1 Verification of Opening Balances 0fVusal QuliyevPas encore d'évaluation

- Cash Flow Estimation and Capital BudgetingDocument29 pagesCash Flow Estimation and Capital BudgetingShehroz Saleem QureshiPas encore d'évaluation

- Target Costing PresentationDocument14 pagesTarget Costing PresentationAks SinhaPas encore d'évaluation

- QuestionsDocument10 pagesQuestionsYat Kunt ChanPas encore d'évaluation

- Lecture 5: Interest Rate Risk (Part I) : DR Lixiong Guo Semester 2, 2015Document31 pagesLecture 5: Interest Rate Risk (Part I) : DR Lixiong Guo Semester 2, 2015studentPas encore d'évaluation

- Standard Costing and Variance Analysis: Fall 2007 CrossonDocument20 pagesStandard Costing and Variance Analysis: Fall 2007 CrossonBernard SalongaPas encore d'évaluation

- Target Costing Presentation FinalDocument57 pagesTarget Costing Presentation FinalMr Dampha100% (1)

- CH 8Document16 pagesCH 8emanmamdouh596Pas encore d'évaluation

- Lecture 2: Exchange Rates and The Foreign Exchange Market: TopicsDocument79 pagesLecture 2: Exchange Rates and The Foreign Exchange Market: TopicsSalvio MachaPas encore d'évaluation

- 3.sales Variance AnalysisDocument38 pages3.sales Variance Analysiskamasuke hegdePas encore d'évaluation

- BM Introduction To BankingDocument36 pagesBM Introduction To BankingNatasha OliviaPas encore d'évaluation

- PPT-4 Parity Conditions and Currency ForecastingDocument42 pagesPPT-4 Parity Conditions and Currency ForecastingKamal KantPas encore d'évaluation

- Balance Scorecard and BenchmarkingDocument12 pagesBalance Scorecard and BenchmarkingGaurav Sharma100% (1)

- Chapter 7Document53 pagesChapter 7Baby KhorPas encore d'évaluation

- Overhead VariancesDocument11 pagesOverhead VariancesDanica VillagantePas encore d'évaluation

- Inventory Management Rev. 1Document26 pagesInventory Management Rev. 1Ryan AbellaPas encore d'évaluation

- Part Seven: THE Management of Financial InstitutionsDocument40 pagesPart Seven: THE Management of Financial InstitutionsIrakli SaliaPas encore d'évaluation

- Machine Tooling Business PlanDocument35 pagesMachine Tooling Business PlanDeepak DileepPas encore d'évaluation

- Income TaxDocument98 pagesIncome TaxGunjan Maheshwari50% (2)

- Product Life Cycle Costing / Whole Life Cycle Costing /life Cycle CostingDocument23 pagesProduct Life Cycle Costing / Whole Life Cycle Costing /life Cycle CostingTapiwa Tbone MadamombePas encore d'évaluation

- Unit-3 Capital BudgetingDocument83 pagesUnit-3 Capital BudgetingAashutosh MishraPas encore d'évaluation

- MCS Assignment - 3Document13 pagesMCS Assignment - 3MIRAL PATELPas encore d'évaluation

- Seventeenth Edition, Global Edition: Strategy, Balanced Scorecard, and Strategic Profitability AnalysisDocument41 pagesSeventeenth Edition, Global Edition: Strategy, Balanced Scorecard, and Strategic Profitability AnalysisAlanood WaelPas encore d'évaluation

- Finance Assignment InstructionDocument7 pagesFinance Assignment InstructionJe-Ta CllPas encore d'évaluation

- Duration GAP AnalysisDocument5 pagesDuration GAP AnalysisShubhash ShresthaPas encore d'évaluation

- International Finance Lecture SlidesDocument27 pagesInternational Finance Lecture Slidesmaryam ashfaqPas encore d'évaluation

- FS AnalysisDocument1 pageFS AnalysisJoePas encore d'évaluation

- MC DonaldDocument15 pagesMC DonaldShreya Patel100% (1)

- 07 X07 A ResponsibilityDocument12 pages07 X07 A ResponsibilityMark Anthony Bulahan100% (1)

- Profit Planning and Activity Based BudgetingDocument50 pagesProfit Planning and Activity Based BudgetingShaiannah Veylaine Recinto ApostolPas encore d'évaluation

- Topic 2 Lecture 3 Discounted Cash Flow ValuationDocument44 pagesTopic 2 Lecture 3 Discounted Cash Flow ValuationSyaimma Syed AliPas encore d'évaluation

- Price Spread, Marketing Channel of Banana in Southern Tamil NaduDocument5 pagesPrice Spread, Marketing Channel of Banana in Southern Tamil NaduEditor IJTSRDPas encore d'évaluation

- 2015 Utilization of Waste Plastic Water Bottle As A Modifier For Asphalt Mixture PropertiesDocument20 pages2015 Utilization of Waste Plastic Water Bottle As A Modifier For Asphalt Mixture PropertiesKhalil ZaaimiaPas encore d'évaluation

- CH 13Document28 pagesCH 13ReneePas encore d'évaluation

- Capital BudgetingDocument9 pagesCapital BudgetingHamoudy DianalanPas encore d'évaluation

- Sample Exam Ch12Document5 pagesSample Exam Ch12zeemeyours100% (1)

- International FInanceDocument3 pagesInternational FInanceJemma JadePas encore d'évaluation

- Chapter Five: The Financial Statements of Banks and Their Principal CompetitorsDocument58 pagesChapter Five: The Financial Statements of Banks and Their Principal CompetitorsYoussef Youssef Ahmed Abdelmeguid Abdel LatifPas encore d'évaluation

- Module IV - Working Capital ManagementDocument50 pagesModule IV - Working Capital ManagementAshwin DholePas encore d'évaluation

- Capital Investment Decisions The Discounted Cash Flow ApproachDocument6 pagesCapital Investment Decisions The Discounted Cash Flow ApproachSimon MtsvorePas encore d'évaluation

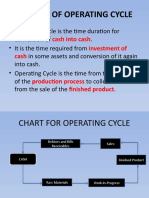

- Concept of Operating Cycle: Cash Into Cash Investment of CashDocument6 pagesConcept of Operating Cycle: Cash Into Cash Investment of CashVenket RamanaPas encore d'évaluation

- FAR - DerivativesDocument1 pageFAR - DerivativesralphalonzoPas encore d'évaluation

- Discounting Cash FlowsDocument5 pagesDiscounting Cash FlowsDriton BinaPas encore d'évaluation

- Hierarchy of VariancesDocument1 pageHierarchy of VariancesQaisar AbbasPas encore d'évaluation

- Management Accounting Chap 003Document67 pagesManagement Accounting Chap 003kenha2000Pas encore d'évaluation

- Strategic Management Environment Analysis WorkshopDocument21 pagesStrategic Management Environment Analysis WorkshopMuhammad Yorga PermanaPas encore d'évaluation

- Management Accounting-Nature and ScopeDocument13 pagesManagement Accounting-Nature and ScopePraveen SinghPas encore d'évaluation

- 6 Dividend DecisionDocument31 pages6 Dividend Decisionambikaantil4408Pas encore d'évaluation

- Costing ExerciseDocument4 pagesCosting ExerciseKien WahPas encore d'évaluation

- Capital BudgetingDocument31 pagesCapital BudgetinggulafridiPas encore d'évaluation

- Presented By: Ubaid Azam Wardag Babar Mustafa Muhammad UsmanDocument13 pagesPresented By: Ubaid Azam Wardag Babar Mustafa Muhammad UsmanShahid AshrafPas encore d'évaluation

- Chapter 08Document17 pagesChapter 08Yuxuan SongPas encore d'évaluation

- Cost Behavior and CVP Analysis PDFDocument22 pagesCost Behavior and CVP Analysis PDFJohn Carlo D. EngayPas encore d'évaluation

- Pricing Decisions and Cost ManagementDocument22 pagesPricing Decisions and Cost ManagementDr. Alla Talal YassinPas encore d'évaluation

- Integrating HR Strategy With Business Strategy: Strategic HRMDocument50 pagesIntegrating HR Strategy With Business Strategy: Strategic HRMTarun KumarPas encore d'évaluation

- Strategy, Balanced Scorecard and Strategic Profitability AnalysisDocument33 pagesStrategy, Balanced Scorecard and Strategic Profitability AnalysisWijdan saleemPas encore d'évaluation

- Topic 2 Part I: Financial StatementsDocument79 pagesTopic 2 Part I: Financial StatementsJohn TomPas encore d'évaluation

- Account Title Unadjusted TB: Moises Dondoyano Information Systems CompanyDocument5 pagesAccount Title Unadjusted TB: Moises Dondoyano Information Systems CompanyJovie FabrosPas encore d'évaluation

- MLM Facts and FiguresDocument19 pagesMLM Facts and FiguresVikas AgrawalPas encore d'évaluation

- Financial Analysis of TNPLDocument23 pagesFinancial Analysis of TNPLarunprakaash100% (1)

- Managerial Accounting 10Document63 pagesManagerial Accounting 10Dheeraj Suntha100% (3)

- SSS 2018 AR 120519 Spread FINALDocument51 pagesSSS 2018 AR 120519 Spread FINALFrederick CasPas encore d'évaluation

- List of Ratio Analysis Formulas and ExplanationsDocument18 pagesList of Ratio Analysis Formulas and ExplanationsCharish Jane Antonio CarreonPas encore d'évaluation

- S4capital Annual Report and Accounts 2021Document172 pagesS4capital Annual Report and Accounts 2021ignaciaPas encore d'évaluation

- Financial RatiosDocument27 pagesFinancial RatiosVenz LacrePas encore d'évaluation

- Tax Suggested Combine June 19Document295 pagesTax Suggested Combine June 19nilanjana100% (1)

- Accounting For Specialized Institution Set 2 Scheme of ValuationDocument19 pagesAccounting For Specialized Institution Set 2 Scheme of ValuationTitus Clement100% (1)

- Evaluating Firm Performance - ReportDocument5 pagesEvaluating Firm Performance - ReportJeane Mae BooPas encore d'évaluation

- Tata Analysis ProjectDocument60 pagesTata Analysis ProjectSeema YadavPas encore d'évaluation

- TUTORIAL SOLUTIONS (Week 4A)Document8 pagesTUTORIAL SOLUTIONS (Week 4A)Peter100% (1)

- Financial Statements Based On Philippine Accounting Standards (Pas)Document34 pagesFinancial Statements Based On Philippine Accounting Standards (Pas)eli broquezaPas encore d'évaluation

- Ratio Analysis - Easy To RememberDocument3 pagesRatio Analysis - Easy To RememberKhushbuJ100% (5)

- Valuation OTA UpdatedDocument8 pagesValuation OTA UpdatedbhajusudipPas encore d'évaluation

- Comprehensive Three Part Revenue Recognition Van Hatten Industri PDFDocument1 pageComprehensive Three Part Revenue Recognition Van Hatten Industri PDFAnbu jaromiaPas encore d'évaluation

- 3 Annual Worth MethodDocument29 pages3 Annual Worth MethodAngel NaldoPas encore d'évaluation