Vous aimerez peut-être aussi

- Time Value of MoneyDocument27 pagesTime Value of MoneyAisah Reem0% (1)

- Case ALDIDocument2 pagesCase ALDIerp_sitepuPas encore d'évaluation

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsD'EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsPas encore d'évaluation

- IB Economics SL15 - Economic IntegrationDocument2 pagesIB Economics SL15 - Economic IntegrationTerran100% (3)

- Real Estate Math Express: Rapid Review and Practice with Essential License Exam CalculationsD'EverandReal Estate Math Express: Rapid Review and Practice with Essential License Exam CalculationsPas encore d'évaluation

- Time Value Money Questions AnswersDocument10 pagesTime Value Money Questions AnswersBabar Ali71% (7)

- Finance for Non-Financiers 1: Basic FinancesD'EverandFinance for Non-Financiers 1: Basic FinancesPas encore d'évaluation

- Time Value of MoneyDocument54 pagesTime Value of MoneyBibhudatta SinghSamantPas encore d'évaluation

- Civil Engineering Cost Analysis ReviewDocument67 pagesCivil Engineering Cost Analysis ReviewAnonymous PkeI8e84Rs100% (1)

- Ch#5 Time Value of MoneyDocument43 pagesCh#5 Time Value of MoneyRafeh AkramPas encore d'évaluation

- RSI UnlimitedDocument2 pagesRSI UnlimitedjedilovagPas encore d'évaluation

- House On Elm Tracy With MapDocument5 pagesHouse On Elm Tracy With MapIzhkarPas encore d'évaluation

- A National Customer Satisfaction Barometer The Swedish ExpeDocument16 pagesA National Customer Satisfaction Barometer The Swedish Expejoannakam100% (1)

- Chapter 5 - Time Value of MoneyDocument12 pagesChapter 5 - Time Value of MoneyDenise LabordoPas encore d'évaluation

- Module - 3act2 - Financial ManagementDocument21 pagesModule - 3act2 - Financial ManagementAngelene Buenafe100% (1)

- Ch.4 - 13ed TVMMasterDocument111 pagesCh.4 - 13ed TVMMasterAfolabi Eniola AbiolaPas encore d'évaluation

- Chapter 04Document41 pagesChapter 04Muntasir SizanPas encore d'évaluation

- The Time Value of Money ExplainedDocument76 pagesThe Time Value of Money ExplainedMañuel É PrasetiyoPas encore d'évaluation

- FIN301-Time Value of MoneyDocument49 pagesFIN301-Time Value of MoneyAbdullah Alosaimi100% (1)

- Chapter 4: Time Value of MoneyDocument32 pagesChapter 4: Time Value of MoneyJasPas encore d'évaluation

- Ch4 PDFDocument49 pagesCh4 PDFGustavo JimenezxPas encore d'évaluation

- Gitman Im ch04Document27 pagesGitman Im ch04debeesantoshPas encore d'évaluation

- Time Value of MoneyDocument71 pagesTime Value of MoneyCHARAK RAYPas encore d'évaluation

- Corporate Finance Week 1 Slide SolutionsDocument4 pagesCorporate Finance Week 1 Slide SolutionsKate BPas encore d'évaluation

- FM - Assignment I - Kubra FatimaDocument15 pagesFM - Assignment I - Kubra FatimaFaryal MughalPas encore d'évaluation

- Chapter 4 QuestionsDocument49 pagesChapter 4 QuestionsJames TaylorPas encore d'évaluation

- Assignment No - 01 (Financial Management (FIN 501)Document9 pagesAssignment No - 01 (Financial Management (FIN 501)aajakirPas encore d'évaluation

- Time Value of Money: Future Value Present Value Rates of Return AmortizationDocument83 pagesTime Value of Money: Future Value Present Value Rates of Return Amortizationbh5029Pas encore d'évaluation

- Topic: Time Value of Money: BY Kajal VipaniDocument50 pagesTopic: Time Value of Money: BY Kajal VipaniAakarshak nandwaniPas encore d'évaluation

- Time Value of MoneyDocument79 pagesTime Value of Moneyvipul khemkaPas encore d'évaluation

- Mini CaseDocument18 pagesMini CaseZeeshan Iqbal0% (1)

- Exam FM Sample SolutionsDocument21 pagesExam FM Sample SolutionssinodakingPas encore d'évaluation

- Edu 2009 Fall Exam FM SolDocument20 pagesEdu 2009 Fall Exam FM Solcl85ScribPas encore d'évaluation

- Solution - Chapter 5Document16 pagesSolution - Chapter 5Diva Tertia AlmiraPas encore d'évaluation

- Ch8 ProblemsDocument4 pagesCh8 Problemsนายฉัตรวิโรจน์ ตรีกาญจนาPas encore d'évaluation

- Ch4 SolutionDocument18 pagesCh4 SolutionJoe KuoPas encore d'évaluation

- Ch5 - SolutionsDocument13 pagesCh5 - Solutionschama2020Pas encore d'évaluation

- Society of Actuaries/Casualty Actuarial Society: Exam FM Sample SolutionsDocument26 pagesSociety of Actuaries/Casualty Actuarial Society: Exam FM Sample SolutionsRyan Shee Soon TeckPas encore d'évaluation

- Solution Manual For Corporate Finance Online 2nd Edition Stanley Eakins William McnallyDocument38 pagesSolution Manual For Corporate Finance Online 2nd Edition Stanley Eakins William Mcnallyoldstermeacocklko8h8100% (12)

- Tugas04_AKM 1-D_23013010276_Bagas Arya Satya DinataDocument13 pagesTugas04_AKM 1-D_23013010276_Bagas Arya Satya DinataBagas Arya Satya DinataPas encore d'évaluation

- Excercise Time Value of Money-Wt Solution NEWDocument6 pagesExcercise Time Value of Money-Wt Solution NEWJeremiah JohnPas encore d'évaluation

- Ch04 ShowDocument95 pagesCh04 ShowpakistanPas encore d'évaluation

- TVM Chapter 3 SummaryDocument186 pagesTVM Chapter 3 SummaryMukesh AroraPas encore d'évaluation

- Chapter 5 - Solution ManualDocument16 pagesChapter 5 - Solution ManualYukti SutavaniPas encore d'évaluation

- Liquidity Maturity Risk Return Current Account/demand Deposit Saving Account/profit and Loss Sharing Fixed Account/term DepositDocument10 pagesLiquidity Maturity Risk Return Current Account/demand Deposit Saving Account/profit and Loss Sharing Fixed Account/term DepositRuman MahmoodPas encore d'évaluation

- 10 - Mixed Cash Flows and AnnuitiesDocument4 pages10 - Mixed Cash Flows and AnnuitiesAli AfzalPas encore d'évaluation

- The Time Value of MoneyDocument14 pagesThe Time Value of MoneyBudi RistantoPas encore d'évaluation

- Time Value of Money: Future Value Present Value Annuities Rates of Return AmortizationDocument52 pagesTime Value of Money: Future Value Present Value Annuities Rates of Return AmortizationMuhammad TalhaPas encore d'évaluation

- Edu 2015 Exam FM Sol TheoryDocument38 pagesEdu 2015 Exam FM Sol TheoryTom YanPas encore d'évaluation

- Lecture 4 PDFDocument94 pagesLecture 4 PDFsyingPas encore d'évaluation

- CH 03Document86 pagesCH 03Ahsan AliPas encore d'évaluation

- Interest Theory SolutionsDocument38 pagesInterest Theory Solutionsshivanithapar13Pas encore d'évaluation

- Chap 6 Notes To Accompany The PP TransparenciesDocument8 pagesChap 6 Notes To Accompany The PP TransparenciesChantal AouadPas encore d'évaluation

- The Time Value of MoneyDocument51 pagesThe Time Value of Moneymajid_mathPas encore d'évaluation

- Time Value of MoneyDocument30 pagesTime Value of MoneyReyhan HarahapPas encore d'évaluation

- Time Value of MoneyDocument7 pagesTime Value of MoneyKaila Clarisse CortezPas encore d'évaluation

- Solution Ch05Document14 pagesSolution Ch05sovuthyPas encore d'évaluation

- Assignment No - 01 (Financial Management (FIN 501)Document9 pagesAssignment No - 01 (Financial Management (FIN 501)aajakirPas encore d'évaluation

- Chapter 9: Other Analysis TechniquesDocument33 pagesChapter 9: Other Analysis TechniquesKamPas encore d'évaluation

- Understanding and Appreciating The Time Value of MoneyDocument68 pagesUnderstanding and Appreciating The Time Value of MoneyEsther LuehPas encore d'évaluation

- Chapter 9 Capital Budgeting PDFDocument112 pagesChapter 9 Capital Budgeting PDFtharinduPas encore d'évaluation

- Solution Manual For Cfin 3 3rd Edition by BesleyDocument3 pagesSolution Manual For Cfin 3 3rd Edition by BesleyAndrewMartinezjrqo100% (44)

- L4 Financial MathematicDocument156 pagesL4 Financial Mathematicfikri86Pas encore d'évaluation

- Laboratory Exercises in Astronomy: Solutions and AnswersD'EverandLaboratory Exercises in Astronomy: Solutions and AnswersPas encore d'évaluation

- My First Padded Board Books of Times Tables: Multiplication Tables From 1-20D'EverandMy First Padded Board Books of Times Tables: Multiplication Tables From 1-20Pas encore d'évaluation

- Chap 11 (PT 1) BBDocument43 pagesChap 11 (PT 1) BBTaVuKieuNhiPas encore d'évaluation

- Chapter 27 BBDocument23 pagesChapter 27 BBTaVuKieuNhiPas encore d'évaluation

- Market Efficiency BBDocument11 pagesMarket Efficiency BBTaVuKieuNhiPas encore d'évaluation

- Chapter 14 BBDocument69 pagesChapter 14 BBTaVuKieuNhiPas encore d'évaluation

- Chapter 24 BBDocument25 pagesChapter 24 BBTaVuKieuNhiPas encore d'évaluation

- Chap 9 BBDocument69 pagesChap 9 BBTaVuKieuNhiPas encore d'évaluation

- Chapter 23BBDocument27 pagesChapter 23BBTaVuKieuNhi100% (1)

- Estimating The Cost of CapitalDocument50 pagesEstimating The Cost of CapitalTaVuKieuNhiPas encore d'évaluation

- Capital Markets and The Pricing of Risk: Chapter 10 (Part I)Document43 pagesCapital Markets and The Pricing of Risk: Chapter 10 (Part I)TaVuKieuNhiPas encore d'évaluation

- Chapter 17 BBDocument48 pagesChapter 17 BBTaVuKieuNhiPas encore d'évaluation

- Chap 11 BB (PT 2 New)Document59 pagesChap 11 BB (PT 2 New)TaVuKieuNhiPas encore d'évaluation

- Capital Markets and The Pricing of Risk: Chapter 10 (Part 2)Document66 pagesCapital Markets and The Pricing of Risk: Chapter 10 (Part 2)TaVuKieuNhiPas encore d'évaluation

- Financial Management: Chapter 1 The CorporationDocument38 pagesFinancial Management: Chapter 1 The CorporationTaVuKieuNhiPas encore d'évaluation

- Introduction To APA Style 6th Ed 2010Document32 pagesIntroduction To APA Style 6th Ed 2010Wided SassiPas encore d'évaluation

- Formula SheetDocument3 pagesFormula SheetTaVuKieuNhiPas encore d'évaluation

- Tutorial 1Document2 pagesTutorial 1TaVuKieuNhi100% (1)

- Chapter 9: Stocks ValuationDocument35 pagesChapter 9: Stocks ValuationTaVuKieuNhiPas encore d'évaluation

- Introduction To APA Style 6th Ed 2010Document32 pagesIntroduction To APA Style 6th Ed 2010Wided SassiPas encore d'évaluation

- Leaders Eat LastDocument6 pagesLeaders Eat LastTaVuKieuNhi25% (4)

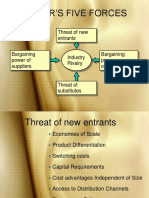

- Porter's Five ForcesDocument9 pagesPorter's Five ForcesTaVuKieuNhiPas encore d'évaluation

- Malaysian Judicial Structure ExplainedDocument21 pagesMalaysian Judicial Structure ExplainedIz'aan AzalanPas encore d'évaluation

- Unemployment and Inflation: Chapter Summary and Learning ObjectivesDocument27 pagesUnemployment and Inflation: Chapter Summary and Learning Objectivesvivianguo23Pas encore d'évaluation

- Item Rate Boq: Sac Code Basic Price (RS.) Rate of GST (In %)Document1 pageItem Rate Boq: Sac Code Basic Price (RS.) Rate of GST (In %)sachinsaklani23Pas encore d'évaluation

- Order Details - Carter'sDocument4 pagesOrder Details - Carter'sSura SeyidovaPas encore d'évaluation

- Pricing strategies to maximize revenue and salesDocument13 pagesPricing strategies to maximize revenue and salesgracePas encore d'évaluation

- Midterm Exam 1 Practice - SolutionDocument6 pagesMidterm Exam 1 Practice - SolutionbobtanlaPas encore d'évaluation

- Journal Article on Causes and Costs of Urban SprawlDocument24 pagesJournal Article on Causes and Costs of Urban SprawlvalogyPas encore d'évaluation

- Glomac BerhadDocument11 pagesGlomac BerhadAiman Abdul BaserPas encore d'évaluation

- Tata AIG Life Lakshya Plus Ensures ADocument10 pagesTata AIG Life Lakshya Plus Ensures Aapi-23693749Pas encore d'évaluation

- Cooper Industries ADocument16 pagesCooper Industries AEshesh GuptaPas encore d'évaluation

- WK5 - S1 - Intro To Supply Chain Management - 2223 - Tri 1Document55 pagesWK5 - S1 - Intro To Supply Chain Management - 2223 - Tri 1patricia njokiPas encore d'évaluation

- Final PPT Anand Rathi ReportDocument25 pagesFinal PPT Anand Rathi ReportKamlesh Kumar Maurya100% (1)

- IOIPROPDocument40 pagesIOIPROPSaifuliza Omar83% (6)

- Chapter II Review of LiteratureDocument31 pagesChapter II Review of LiteratureHari PriyaPas encore d'évaluation

- Helmet Manufacturing Industry-293269 PDFDocument68 pagesHelmet Manufacturing Industry-293269 PDFJaydeep MoharanaPas encore d'évaluation

- Yummy Ice Cream Presentation SummaryDocument34 pagesYummy Ice Cream Presentation SummaryUsamaPas encore d'évaluation

- Case HimontDocument24 pagesCase Himontssaurabh88Pas encore d'évaluation

- Mary River Financial SubmissionDocument10 pagesMary River Financial SubmissionNunatsiaqNewsPas encore d'évaluation

- Tutorial 9 Problem SetDocument6 pagesTutorial 9 Problem SetPeter Jackson0% (1)

- Name: E-Mail: Cell Phone Number:: Balance Sheet Initial 1st MonthDocument3 pagesName: E-Mail: Cell Phone Number:: Balance Sheet Initial 1st MonthEmiliano Mancilla SilvaPas encore d'évaluation

- Ainaro NCB - R 190023Document79 pagesAinaro NCB - R 190023filomeno martinsPas encore d'évaluation

- Low Income Housing Tax Credits: March 4, 2013Document31 pagesLow Income Housing Tax Credits: March 4, 2013Michael ShavolianPas encore d'évaluation

- Marketing StrategyDocument7 pagesMarketing StrategyAnonymous oklXbtc8Pas encore d'évaluation

- The Dinkum Index - Q211Document13 pagesThe Dinkum Index - Q211economicdelusionPas encore d'évaluation

- Valeura PDFDocument11 pagesValeura PDFRodrigo RodrigoPas encore d'évaluation

- Chapter 2 Cost Concepts and Design Economics PART 2 With AssignmentDocument30 pagesChapter 2 Cost Concepts and Design Economics PART 2 With AssignmentrplagrosaPas encore d'évaluation