Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (120)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Gocardless Direct Debit GuideDocument53 pagesGocardless Direct Debit GuideGregory CarterPas encore d'évaluation

- Time Value of MoneyDocument54 pagesTime Value of MoneyJoyce Ann Basilio100% (5)

- Account Summary Payment Information: New Balance $1,339.26Document6 pagesAccount Summary Payment Information: New Balance $1,339.26donghyuck leePas encore d'évaluation

- Shareholder's EquityDocument31 pagesShareholder's EquityAmmie Lemie100% (2)

- Question Bank For University Questions For 2 YearsDocument6 pagesQuestion Bank For University Questions For 2 Yearssubakarthi100% (1)

- Reporting of Counterfeit NotesDocument12 pagesReporting of Counterfeit Notesaksh_teddy100% (1)

- How To Manage Your Small Business EffectivelyDocument3 pagesHow To Manage Your Small Business EffectivelyMudFlap gaming100% (1)

- Analyzing Common Business Transaction Using Debit and CreditDocument5 pagesAnalyzing Common Business Transaction Using Debit and CreditMarlyn Lotivio100% (1)

- Financial Ratio AnalysisDocument53 pagesFinancial Ratio AnalysisLaurentia Nurak100% (4)

- Global Financial Management: Activity - 1 - Case StudyDocument18 pagesGlobal Financial Management: Activity - 1 - Case StudysubakarthiPas encore d'évaluation

- Basics of Accounting Level IIDocument63 pagesBasics of Accounting Level IIArun MinnasandranPas encore d'évaluation

- Money Market InstrumentsDocument10 pagesMoney Market InstrumentssubakarthiPas encore d'évaluation

- Global Financial Management: Activity - 1 - Case StudyDocument18 pagesGlobal Financial Management: Activity - 1 - Case StudysubakarthiPas encore d'évaluation

- Share TerminologyDocument33 pagesShare TerminologysubakarthiPas encore d'évaluation

- Sensex & NiftyDocument5 pagesSensex & NiftysubakarthiPas encore d'évaluation

- Global MarketDocument9 pagesGlobal MarketsubakarthiPas encore d'évaluation

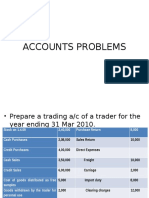

- Accounts ProblemsDocument3 pagesAccounts ProblemssubakarthiPas encore d'évaluation

- Income Tax QuizDocument69 pagesIncome Tax QuizsubakarthiPas encore d'évaluation

- Unit - IiDocument110 pagesUnit - IisubakarthiPas encore d'évaluation

- DerivativesDocument62 pagesDerivativessubakarthi100% (1)

- Dip Guidelines 2009Document384 pagesDip Guidelines 2009manmachine85Pas encore d'évaluation

- DerivativesDocument62 pagesDerivativessubakarthi100% (1)

- Accounts ProblemsDocument3 pagesAccounts ProblemsmnsasirekhaPas encore d'évaluation

- Case StudyDocument17 pagesCase Studysubakarthi0% (1)

- Unit - IDocument21 pagesUnit - IsubakarthiPas encore d'évaluation

- Question BankDocument21 pagesQuestion BanksubakarthiPas encore d'évaluation

- Cost of CapitalDocument23 pagesCost of CapitalsubakarthiPas encore d'évaluation

- Corporate Finance: BA8014 - REGULATION - 2013Document36 pagesCorporate Finance: BA8014 - REGULATION - 2013subakarthiPas encore d'évaluation

- Unit - VDocument44 pagesUnit - VsubakarthiPas encore d'évaluation

- A Study On Ratio Analysis of Sri Vengadalakshmi SpinnersDocument10 pagesA Study On Ratio Analysis of Sri Vengadalakshmi SpinnerssubakarthiPas encore d'évaluation

- P.O Box 1770, Rahim Pur Khichian Said Pur Road Sialkot-Pakistanphone:-+92-52 - 4268188,4260850-1 Fax: - +92-52-4262852Document56 pagesP.O Box 1770, Rahim Pur Khichian Said Pur Road Sialkot-Pakistanphone:-+92-52 - 4268188,4260850-1 Fax: - +92-52-4262852adeelbajwaPas encore d'évaluation

- Sunedison MemoDocument67 pagesSunedison MemoAnonymous 5Ukh0DZPas encore d'évaluation

- Internship Report On Social Islami Bank Limited 1Document56 pagesInternship Report On Social Islami Bank Limited 1sakib100% (3)

- Why Marc Faber Is Such A BearDocument6 pagesWhy Marc Faber Is Such A BearrobintanwhPas encore d'évaluation

- Communication Challenges in BFSI NBFC SectorsDocument15 pagesCommunication Challenges in BFSI NBFC SectorsShivam GuptaPas encore d'évaluation

- CSR&SD 0118 l1 Intro To CSRDocument27 pagesCSR&SD 0118 l1 Intro To CSRUditPas encore d'évaluation

- Innocents Abroad Currencies and International Stock ReturnsDocument39 pagesInnocents Abroad Currencies and International Stock ReturnsShivaniPas encore d'évaluation

- 2022 October LNUDocument16 pages2022 October LNUShari AngelPas encore d'évaluation

- FafsaDocument5 pagesFafsaapi-244239127Pas encore d'évaluation

- Lobal Investments: Discover Your Real Cost of Capital-And Your Real RiskDocument6 pagesLobal Investments: Discover Your Real Cost of Capital-And Your Real RiskAdamSmith1990Pas encore d'évaluation

- Assignment September 2020 Semester: Subject Code MKM602 Subject Title Marketing Management Level Master'S DegreeDocument15 pagesAssignment September 2020 Semester: Subject Code MKM602 Subject Title Marketing Management Level Master'S Degreemahnoor arifPas encore d'évaluation

- Sick Unit ProjectsDocument62 pagesSick Unit ProjectsPratik Shah100% (1)

- Functions of National Small Industries Corporation (NSIC)Document14 pagesFunctions of National Small Industries Corporation (NSIC)Naveen Jacob JohnPas encore d'évaluation

- Revenue Memo Ruling 02-2002Document20 pagesRevenue Memo Ruling 02-2002Annie SibayanPas encore d'évaluation

- The Companies Ordinance 2017 Company Limited by Shares Articles of Association of Al-Abbas Seed PROCESSING Private Limited CompaniesDocument7 pagesThe Companies Ordinance 2017 Company Limited by Shares Articles of Association of Al-Abbas Seed PROCESSING Private Limited Companiesabbs khanPas encore d'évaluation

- 1 s2.0 S1572308923000323 MainDocument13 pages1 s2.0 S1572308923000323 MainAnditio Yudha PurwonoPas encore d'évaluation

- 4th Sem All Model Answers (Agrounder)Document111 pages4th Sem All Model Answers (Agrounder)Words You Can FeelPas encore d'évaluation

- Gill Wilkins Technology Transfer For Renewable Energy Overcoming Barriers in Developing CountriesDocument256 pagesGill Wilkins Technology Transfer For Renewable Energy Overcoming Barriers in Developing CountriesmshameliPas encore d'évaluation

- The Importance of Forex Reserves For RBI, Economy: Job Scene BrightensDocument16 pagesThe Importance of Forex Reserves For RBI, Economy: Job Scene BrightensVidhi SharmaPas encore d'évaluation

- Internship Report On General Banking of Janata Bank LimitedDocument35 pagesInternship Report On General Banking of Janata Bank LimitedMd. Tareq AzizPas encore d'évaluation

- Quiz Conceptual Framework WITH ANSWERSDocument25 pagesQuiz Conceptual Framework WITH ANSWERSasachdeva17100% (1)

- Government Expenditure: Economy of MalaysiaDocument17 pagesGovernment Expenditure: Economy of MalaysiaTk Kendrick LauPas encore d'évaluation