Vous aimerez peut-être aussi

- Economics: Private and Public ChoiceD'EverandEconomics: Private and Public ChoiceÉvaluation : 2.5 sur 5 étoiles2.5/5 (12)

- Chapter 3 Money and Monetary PolicyDocument35 pagesChapter 3 Money and Monetary PolicyZaid Harithah100% (1)

- MicroeconomicsDocument76 pagesMicroeconomicsAgostina DanielPas encore d'évaluation

- EC 102 Revisions Lectures - Macro - 2015Document54 pagesEC 102 Revisions Lectures - Macro - 2015TylerTangTengYangPas encore d'évaluation

- ECN 2215 - Topic - 2 PDFDocument54 pagesECN 2215 - Topic - 2 PDFKalenga AlexPas encore d'évaluation

- CH 19. Macroeconomic Goals and InstrumentsDocument25 pagesCH 19. Macroeconomic Goals and InstrumentsJutt TheMagician100% (1)

- S5M IS-LM ModelDocument34 pagesS5M IS-LM ModelManoranjan DashPas encore d'évaluation

- Consumption: 1. Define Carefully The Following and Give An Example of EachDocument9 pagesConsumption: 1. Define Carefully The Following and Give An Example of EachSashwot BasnetPas encore d'évaluation

- Forex ProblemsDocument17 pagesForex ProblemsFoo Chuan Mao100% (1)

- Chapter 6 - Macroeconomics Big PictureDocument37 pagesChapter 6 - Macroeconomics Big Picturemajor raveendraPas encore d'évaluation

- The Quantity Theory of MoneyDocument37 pagesThe Quantity Theory of MoneyLuciano PatruccoPas encore d'évaluation

- Theory of Scientific ManagementDocument8 pagesTheory of Scientific ManagementAmba Datt PantPas encore d'évaluation

- E201 Ch01 Ten Principles of EconomicsDocument24 pagesE201 Ch01 Ten Principles of EconomicsshamsaPas encore d'évaluation

- Assignment On Intermediate Macro Economic (ECN 303) - USEDDocument6 pagesAssignment On Intermediate Macro Economic (ECN 303) - USEDBernardokpePas encore d'évaluation

- Macroeconomic PrinciplesDocument128 pagesMacroeconomic PrinciplesTsitsi Abigail100% (2)

- Factors Affecting DemandDocument7 pagesFactors Affecting DemandDina Navarro DiestroPas encore d'évaluation

- The Phillips CurveDocument6 pagesThe Phillips CurveAppan Kandala VasudevacharyPas encore d'évaluation

- CH 3 Macroeconomics AAUDocument90 pagesCH 3 Macroeconomics AAUFaris Khalid100% (1)

- Unit 14 InflationDocument14 pagesUnit 14 InflationRajveer SinghPas encore d'évaluation

- Quantity Theory of MoneyDocument6 pagesQuantity Theory of MoneyBernard OkpePas encore d'évaluation

- Speculative Currency AttacksDocument4 pagesSpeculative Currency AttacksSuhas KandePas encore d'évaluation

- Macro EconomicsDocument291 pagesMacro EconomicsCH Mehboob AhmadPas encore d'évaluation

- Economics 20000 SyllabusDocument3 pagesEconomics 20000 SyllabusJulie BrightPas encore d'évaluation

- University of Chicago ECON 20300 Problem SetDocument23 pagesUniversity of Chicago ECON 20300 Problem SetR. KrogerPas encore d'évaluation

- Chapter 6 Mankiw (Macroeconomics)Document36 pagesChapter 6 Mankiw (Macroeconomics)andrew myintmyat100% (1)

- Principles of EconomicsDocument50 pagesPrinciples of EconomicsRomar M. DavidPas encore d'évaluation

- Parkinmacro15 1300Document17 pagesParkinmacro15 1300Avijit Pratap RoyPas encore d'évaluation

- By: Domodar N. Gujarati: Prof. M. El-SakkaDocument19 pagesBy: Domodar N. Gujarati: Prof. M. El-SakkarohanpjadhavPas encore d'évaluation

- Importance of Time Value of Money in Financial ManagementDocument16 pagesImportance of Time Value of Money in Financial Managementtanmayjoshi969315Pas encore d'évaluation

- Parkinmacro11 (28) 1200Document19 pagesParkinmacro11 (28) 1200nikowawa100% (1)

- Answers To Summer 2010 Perfect Competition QuestionsDocument7 pagesAnswers To Summer 2010 Perfect Competition QuestionsNikhil Darak100% (1)

- Fiscal Policy in Dynamic EconomiesDocument27 pagesFiscal Policy in Dynamic EconomiesFelipe Males LemaPas encore d'évaluation

- Household Behavior Consumer ChoiceDocument40 pagesHousehold Behavior Consumer ChoiceRAYMUND JOHN ROSARIOPas encore d'évaluation

- Phillips CurveDocument37 pagesPhillips CurveJayati KaamraPas encore d'évaluation

- Macroeconomics Anforme TextbookDocument64 pagesMacroeconomics Anforme TextbookScott Jefferson100% (1)

- Money Supply and Money Demand (File 4)Document21 pagesMoney Supply and Money Demand (File 4)Sadaqatullah NoonariPas encore d'évaluation

- A Science and Its History: Chapter 1Document14 pagesA Science and Its History: Chapter 1dfarias1989Pas encore d'évaluation

- Edited PPT The Colonial Origins of Comparative Development-An Empirical InvestigationDocument34 pagesEdited PPT The Colonial Origins of Comparative Development-An Empirical InvestigationJad ZoghaibPas encore d'évaluation

- Liquidity Preference TheoryDocument34 pagesLiquidity Preference Theorygoldenguy90100% (2)

- Mankiw (1995) - The Growth of NationsDocument53 pagesMankiw (1995) - The Growth of NationsAnonymous WFjMFHQ100% (1)

- Friedmans Restatement of Quantity Theory of MoneuDocument7 pagesFriedmans Restatement of Quantity Theory of MoneuRitesh kumarPas encore d'évaluation

- Feenstra Taylor Chapter 1Document10 pagesFeenstra Taylor Chapter 1sankalpakashPas encore d'évaluation

- Chapter 1 PDFDocument15 pagesChapter 1 PDFRodina MuhammedPas encore d'évaluation

- Cmrmiranda Powerpoint Presentation November2011 Macro EconomicsDocument15 pagesCmrmiranda Powerpoint Presentation November2011 Macro EconomicsjameskagomePas encore d'évaluation

- Principles of Macroeconomics Practice AssignmentDocument4 pagesPrinciples of Macroeconomics Practice AssignmentAnonymous xUb9GnoFPas encore d'évaluation

- International Accounting Chap 006Document39 pagesInternational Accounting Chap 006ChuckPas encore d'évaluation

- Economic Models:: Basic Mathematical Tools Applied in EconomicsDocument28 pagesEconomic Models:: Basic Mathematical Tools Applied in EconomicsGaurav AroraPas encore d'évaluation

- Harvard Economics 2020a Problem Set 3Document2 pagesHarvard Economics 2020a Problem Set 3JPas encore d'évaluation

- Book ChapterDocument9 pagesBook ChapterSiskawpPas encore d'évaluation

- Hecksher Ohlin ModelDocument49 pagesHecksher Ohlin ModelPaula Mae EspirituPas encore d'évaluation

- The Data of Macroeconomics: AcroeconomicsDocument54 pagesThe Data of Macroeconomics: Acroeconomicsaditya prudhviPas encore d'évaluation

- Macroeconomics Final Exam Fall 2014Document4 pagesMacroeconomics Final Exam Fall 2014Andrew HuPas encore d'évaluation

- CH 13 Macroeconomics KrugmanDocument6 pagesCH 13 Macroeconomics KrugmanMary Petrova100% (2)

- Ch. 4 Demand For MoneyDocument13 pagesCh. 4 Demand For Moneycoldpassion100% (1)

- Macro 95 Ex 2Document17 pagesMacro 95 Ex 2Engr Fizza AkbarPas encore d'évaluation

- The Politics of Inflation: A Comparative AnalysisD'EverandThe Politics of Inflation: A Comparative AnalysisRichard MedleyPas encore d'évaluation

- The Economists' Voice 2.0: The Financial Crisis, Health Care Reform, and MoreD'EverandThe Economists' Voice 2.0: The Financial Crisis, Health Care Reform, and MorePas encore d'évaluation

- Intermediate Macroeconomics (Ecn 2215) : Money and Inflation Lecture Notes by Charles M. Banda Notes Extracted From MankiwDocument25 pagesIntermediate Macroeconomics (Ecn 2215) : Money and Inflation Lecture Notes by Charles M. Banda Notes Extracted From MankiwYande ZuluPas encore d'évaluation

- The Open EconomyDocument44 pagesThe Open EconomyahmeddanafPas encore d'évaluation

- Digital CashDocument44 pagesDigital CashahmeddanafPas encore d'évaluation

- Time Series ARIMA Models PDFDocument22 pagesTime Series ARIMA Models PDFahmeddanafPas encore d'évaluation

- Chapter 3 Summary: Second, of Course, If You Drop The (Common) Intercept From The Model, You Can Have AsDocument1 pageChapter 3 Summary: Second, of Course, If You Drop The (Common) Intercept From The Model, You Can Have AsahmeddanafPas encore d'évaluation

- The Data of MacroeconomicsDocument40 pagesThe Data of MacroeconomicsahmeddanafPas encore d'évaluation

- National IncomeDocument37 pagesNational IncomeahmeddanafPas encore d'évaluation

- Paul Krugman - Économie Internationale. Nouveaux Horizons.2009Document1 pagePaul Krugman - Économie Internationale. Nouveaux Horizons.2009ahmeddanafPas encore d'évaluation

- Economic CrisisDocument312 pagesEconomic CrisisahmeddanafPas encore d'évaluation

- Derivatives MarketsDocument9 pagesDerivatives MarketsahmeddanafPas encore d'évaluation

- International FinanceDocument32 pagesInternational FinanceahmeddanafPas encore d'évaluation

- Instructor'S Manual: International TradeDocument206 pagesInstructor'S Manual: International Tradebigeaz50% (4)

- Libya of TomorrowDocument136 pagesLibya of TomorrowahmeddanafPas encore d'évaluation

- Does Teacher Training Pupil LearningDocument28 pagesDoes Teacher Training Pupil LearningahmeddanafPas encore d'évaluation

- Libya Lost Opportunities and Renewed HopesDocument16 pagesLibya Lost Opportunities and Renewed HopesahmeddanafPas encore d'évaluation

- Macbook Air 13 Inch User's GuideDocument76 pagesMacbook Air 13 Inch User's GuideahmeddanafPas encore d'évaluation

- Libya of TomorrowDocument136 pagesLibya of TomorrowahmeddanafPas encore d'évaluation

- Why Do Countries Float The Way They FloatDocument40 pagesWhy Do Countries Float The Way They FloatahmeddanafPas encore d'évaluation

- Limits of Floating Exchange RatesDocument52 pagesLimits of Floating Exchange RatesahmeddanafPas encore d'évaluation

- Libya of TomorrowDocument136 pagesLibya of TomorrowahmeddanafPas encore d'évaluation

- Exercicios Do Capitulo 8 (Finanças Empresariais)Document3 pagesExercicios Do Capitulo 8 (Finanças Empresariais)Gonçalo AlmeidaPas encore d'évaluation

- Name: Instructor: Accounting Principles Primer On Using Excel in AccountingDocument14 pagesName: Instructor: Accounting Principles Primer On Using Excel in Accountingranim m7mdPas encore d'évaluation

- Equity Valuation of MaricoDocument18 pagesEquity Valuation of MaricoPriyanka919100% (1)

- The Letter of Credit ProcessDocument1 pageThe Letter of Credit ProcessGirish RanganathanPas encore d'évaluation

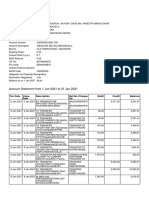

- Sbi Account Jan 2021Document2 pagesSbi Account Jan 2021Manoj GaurPas encore d'évaluation

- Foreign Exchange MarketsDocument19 pagesForeign Exchange MarketsniggerPas encore d'évaluation

- HS Business Administration Core Sample ExamDocument33 pagesHS Business Administration Core Sample ExamCherie LeePas encore d'évaluation

- Buildium Outstanding BalancesDocument34 pagesBuildium Outstanding BalancesJulian KurtPas encore d'évaluation

- Corporate FinanceDocument18 pagesCorporate FinanceNishakdasPas encore d'évaluation

- Subunit 3.6 Efficiency Ratio AnalysisDocument30 pagesSubunit 3.6 Efficiency Ratio AnalysisSteam MainPas encore d'évaluation

- Hedge Funds: Origins and Evolution: John H. MakinDocument17 pagesHedge Funds: Origins and Evolution: John H. MakinHiren ShahPas encore d'évaluation

- Cca CPP HcaDocument1 pageCca CPP Hcahusse fokPas encore d'évaluation

- Final Project NPA MANAGEMENT IN BANKSDocument88 pagesFinal Project NPA MANAGEMENT IN BANKSmanish223283% (18)

- Exam On Foreign Currency Transaction 40Document6 pagesExam On Foreign Currency Transaction 40nigusPas encore d'évaluation

- Penjelasan Tentang Saving-Investment GapDocument40 pagesPenjelasan Tentang Saving-Investment GapbahrulPas encore d'évaluation

- Credit Risk ManagementDocument4 pagesCredit Risk ManagementinspectorsufiPas encore d'évaluation

- Money PadDocument15 pagesMoney PadSubhash PbsPas encore d'évaluation

- Narrative ReportDocument3 pagesNarrative ReportKrissie Jane MorinPas encore d'évaluation

- IIM Udaipur Placements DecodedDocument4 pagesIIM Udaipur Placements DecodedUjjwalPratapSinghPas encore d'évaluation

- Eaton Case Study 2023Document19 pagesEaton Case Study 2023Paskal100% (1)

- Concepts in Financial ManagementDocument3 pagesConcepts in Financial ManagementfeilohPas encore d'évaluation

- Account Titles UsedDocument40 pagesAccount Titles Usedmaria cacaoPas encore d'évaluation

- Individual Assignment OneDocument3 pagesIndividual Assignment OnefeyselPas encore d'évaluation

- Wk8 Laura Martin REPORTDocument18 pagesWk8 Laura Martin REPORTNino Chen100% (2)

- Afar 08Document14 pagesAfar 08RENZEL MAGBITANGPas encore d'évaluation

- "Bank Lending, A Significant Effort To Financing Sme'': Eliona Gremi PHD CandidateDocument6 pages"Bank Lending, A Significant Effort To Financing Sme'': Eliona Gremi PHD CandidateAnduela MemaPas encore d'évaluation

- Bitcoin RoughDocument19 pagesBitcoin RoughSaloni Jain 1820343Pas encore d'évaluation

- The Pony Express: Read The Article Below Then Answer The Questions That FollowDocument12 pagesThe Pony Express: Read The Article Below Then Answer The Questions That FollowHower XuPas encore d'évaluation

- Analysis of Credit Risk, Liquidity and Profitability of The Trade Bank of Iraq For The Period (2012-2021)Document25 pagesAnalysis of Credit Risk, Liquidity and Profitability of The Trade Bank of Iraq For The Period (2012-2021)Ali Abdulhassan AbbasPas encore d'évaluation

- Asset Classes and Financial InstrumentsDocument33 pagesAsset Classes and Financial Instrumentskaylakshmi8314Pas encore d'évaluation