Vous aimerez peut-être aussi

- General AverageDocument30 pagesGeneral Averageأحمد شكورPas encore d'évaluation

- Salvage and Towage PDFDocument3 pagesSalvage and Towage PDFHrw MakriPas encore d'évaluation

- Seaworthiness and Reasoanable DispacthDocument14 pagesSeaworthiness and Reasoanable DispacthKaiyisah MalikPas encore d'évaluation

- Explanation Why We Need Loi For ComminglingDocument7 pagesExplanation Why We Need Loi For ComminglingJayakumar SankaranPas encore d'évaluation

- Blue Chip Stocks TipsDocument16 pagesBlue Chip Stocks TipsPinal MehtaPas encore d'évaluation

- FIN036 AssignmentDocument25 pagesFIN036 AssignmentSandeep BholahPas encore d'évaluation

- General Power of AttorneyDocument2 pagesGeneral Power of AttorneyDred OplePas encore d'évaluation

- Towage - Guidance - UK P&I ClubDocument12 pagesTowage - Guidance - UK P&I ClubnostremarumPas encore d'évaluation

- Marine InsuranceDocument44 pagesMarine InsuranceMitanshu Chadha100% (1)

- 70 Marine Hull InsDocument14 pages70 Marine Hull InsFaheemPas encore d'évaluation

- Marine InsuranceDocument16 pagesMarine InsuranceCAJaideepPas encore d'évaluation

- Chapter 7 - InsuranceDocument29 pagesChapter 7 - InsuranceDe GawanPas encore d'évaluation

- Marine InsuranceDocument43 pagesMarine InsuranceGourav Mukherjee100% (2)

- Marine InsuranceDocument33 pagesMarine InsuranceSitiPas encore d'évaluation

- Shipping Practice - With a Consideration of the Law Relating TheretoD'EverandShipping Practice - With a Consideration of the Law Relating TheretoPas encore d'évaluation

- Introduction To P and I InsuranceDocument56 pagesIntroduction To P and I InsuranceChan_abm100% (1)

- York Antwerp RulesDocument15 pagesYork Antwerp Rulessaurabh1906Pas encore d'évaluation

- Marine Perils and P&I SlideDocument17 pagesMarine Perils and P&I SlideDalilaPas encore d'évaluation

- Marine InsuranceDocument60 pagesMarine Insurancepmsaravanan2000100% (1)

- Marine InsuranceDocument62 pagesMarine Insurancepisourie25Pas encore d'évaluation

- Marine Cargo Underwriting & Causes of Loss PDFDocument53 pagesMarine Cargo Underwriting & Causes of Loss PDFAnil PatelPas encore d'évaluation

- LO4 - 2d Insurance H&M-P&IDocument28 pagesLO4 - 2d Insurance H&M-P&ISapna DasPas encore d'évaluation

- Classification Society - Capt - Saujanya SinhaDocument3 pagesClassification Society - Capt - Saujanya SinhaJitender MalikPas encore d'évaluation

- Cos Charter PartyDocument61 pagesCos Charter PartyFroilan EspinosaPas encore d'évaluation

- Ship BreakingDocument110 pagesShip Breakingreebenthomas100% (1)

- 9 Elements of Marine Insurance ContractDocument2 pages9 Elements of Marine Insurance ContractFaheemPas encore d'évaluation

- P & I Club InsuranceDocument20 pagesP & I Club Insurancesxy_sadiPas encore d'évaluation

- Ship Master's BusinessDocument5 pagesShip Master's BusinessDaniel M. MartinPas encore d'évaluation

- Valuation of Marine VesselsDocument41 pagesValuation of Marine VesselsReza Babakhani100% (1)

- Lof and Scopic HistoryDocument22 pagesLof and Scopic HistoryBansal SunilPas encore d'évaluation

- 3 - Module 3Document68 pages3 - Module 3Hossam SaidPas encore d'évaluation

- MarineDocument48 pagesMarineoxynetPas encore d'évaluation

- Marine and Hull InsuranceDocument12 pagesMarine and Hull InsuranceHarish NageshwaranPas encore d'évaluation

- Marine Insurance Executive Summary: Individual or Organization That Requires Insurance."Document72 pagesMarine Insurance Executive Summary: Individual or Organization That Requires Insurance."Bhaskar ChauhanPas encore d'évaluation

- Marine InsuranceDocument40 pagesMarine Insuranceswastina100% (2)

- S - What Is ISMDocument14 pagesS - What Is ISMJahidur RahmanPas encore d'évaluation

- Certificate in CharteringDocument51 pagesCertificate in CharteringΘάνος ΜητροφανάκηςPas encore d'évaluation

- Marine InsuranceDocument87 pagesMarine Insurancegaurav goelPas encore d'évaluation

- General AverageDocument25 pagesGeneral AverageMohamed Salah El Din100% (1)

- Maritime Law Cases PDFDocument38 pagesMaritime Law Cases PDFKris Antonnete DaleonPas encore d'évaluation

- Differences Between Towage and SalvageDocument5 pagesDifferences Between Towage and SalvageGirish Menon100% (1)

- Marinecargo Insurance 1 To 209Document209 pagesMarinecargo Insurance 1 To 209Awadhesh Yadav0% (1)

- Safety Management System (SMS) Guidelines: What Is An SMS?Document10 pagesSafety Management System (SMS) Guidelines: What Is An SMS?diegocely700615Pas encore d'évaluation

- How To Handle Cargo ClaimsDocument3 pagesHow To Handle Cargo Claimspinko11Pas encore d'évaluation

- Marine Cargo InsuranceDocument72 pagesMarine Cargo InsuranceKhanh Duyen Nguyen HuynhPas encore d'évaluation

- 30 LettersofProtest PDFDocument52 pages30 LettersofProtest PDFjaPas encore d'évaluation

- Diploma in Cargo SurveyingDocument8 pagesDiploma in Cargo SurveyingGeorge MasvoulasPas encore d'évaluation

- Bill of LadingDocument25 pagesBill of LadingChristian SimeonPas encore d'évaluation

- Cargo InsuranceDocument18 pagesCargo InsuranceYam ChaulagainPas encore d'évaluation

- 03.legislative FrameworkDocument22 pages03.legislative Frameworkmingo622Pas encore d'évaluation

- Ic s01 Marine Cargo and Hull InsuranceDocument59 pagesIc s01 Marine Cargo and Hull InsuranceRanjithPas encore d'évaluation

- Institute Marine Cargo ClausesDocument13 pagesInstitute Marine Cargo ClausesAnonymous hO4rU6sf100% (1)

- Analysis of Maritime Inspection RegimesDocument39 pagesAnalysis of Maritime Inspection RegimesVinod DsouzaPas encore d'évaluation

- Ship Op Compiled NotesDocument132 pagesShip Op Compiled NotesMithunPas encore d'évaluation

- Hull InsuranceDocument73 pagesHull InsurancePrashant PawarPas encore d'évaluation

- ESP - Booklet For Bulk Carriers (Including Ore Carriers) - tcm155-206340Document71 pagesESP - Booklet For Bulk Carriers (Including Ore Carriers) - tcm155-206340Jusak Sonang SiahaanPas encore d'évaluation

- Marine Survey Practice - Surveyor Guide Notes For Ship Stability, Inclining Test ProcedureDocument11 pagesMarine Survey Practice - Surveyor Guide Notes For Ship Stability, Inclining Test ProcedureshahjadaPas encore d'évaluation

- Insurable Interest in Maritime LawDocument18 pagesInsurable Interest in Maritime LawSebin JamesPas encore d'évaluation

- Importance of Classification SocietiesDocument3 pagesImportance of Classification SocietiesUmairPas encore d'évaluation

- Simplifying SCOPIC Clause and Salvage ConventionDocument3 pagesSimplifying SCOPIC Clause and Salvage ConventionGaurav Ojha100% (1)

- Rebranding The Unique YouDocument20 pagesRebranding The Unique YouSunday Oluwole100% (1)

- Audit Report Summary and ConclusionDocument13 pagesAudit Report Summary and ConclusionSunday OluwolePas encore d'évaluation

- Marine Cargo Claims ProcedureDocument16 pagesMarine Cargo Claims ProcedureSunday Oluwole100% (1)

- Oil & Gas Accounting, May 2011Document9 pagesOil & Gas Accounting, May 2011Sunday Oluwole50% (2)

- FND - Pilot Question & AnswerDocument118 pagesFND - Pilot Question & AnswerSunday OluwolePas encore d'évaluation

- 2008 Nigeria Insurance DigestDocument152 pages2008 Nigeria Insurance DigestSunday Oluwole100% (1)

- Standard CostingDocument52 pagesStandard CostingSunday Oluwole0% (1)

- 2.3 Audit AssuranceDocument27 pages2.3 Audit AssurancemohedPas encore d'évaluation

- Act 276 Islamic Banking Act 1983Document46 pagesAct 276 Islamic Banking Act 1983Adam Haida & CoPas encore d'évaluation

- LIC's JEEVAN RAKSHAK (UIN: 512N289V01) - : Policy DocumentDocument11 pagesLIC's JEEVAN RAKSHAK (UIN: 512N289V01) - : Policy DocumentSaravanan DuraiPas encore d'évaluation

- Oceanic Bank International PLC - Revised Financial Statement For The 15 Month Period Ended December 31, 2008Document1 pageOceanic Bank International PLC - Revised Financial Statement For The 15 Month Period Ended December 31, 2008Oceanic Bank International PLC50% (2)

- New ResumeDocument2 pagesNew ResumeDana McgrottyPas encore d'évaluation

- Finance of International Trade Related Treasury OperationsDocument1 pageFinance of International Trade Related Treasury OperationsMuhammad KamranPas encore d'évaluation

- Class Notes On Income Tax On CorporationsDocument3 pagesClass Notes On Income Tax On CorporationsJeremie R. PlazaPas encore d'évaluation

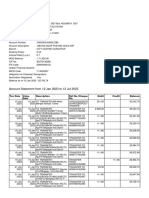

- Account Statement From 12 Jan 2023 To 12 Jul 2023Document10 pagesAccount Statement From 12 Jan 2023 To 12 Jul 2023SouravDeyPas encore d'évaluation

- What Is A Continuing Guarantee and What Are Its Modes of RevocationDocument4 pagesWhat Is A Continuing Guarantee and What Are Its Modes of RevocationNitya Nand Pandey100% (1)

- Fin MarDocument2 pagesFin MarKoleen Mae LindayenPas encore d'évaluation

- Questionnaire: Brand Loyalty and Relationship Marketing in State Bank of India's Banking System. IDocument6 pagesQuestionnaire: Brand Loyalty and Relationship Marketing in State Bank of India's Banking System. IAanand SharmaPas encore d'évaluation

- PldtbillDocument4 pagesPldtbilljen marquesPas encore d'évaluation

- Comparative Financial Statement Analysis of The Big Three Banks Operating in Finland 2015-2016Document49 pagesComparative Financial Statement Analysis of The Big Three Banks Operating in Finland 2015-2016Eugene Rugo APas encore d'évaluation

- Credit CardDocument15 pagesCredit Cardsrdagpnt100% (1)

- Complete Handouts Batch 2021-1-200Document200 pagesComplete Handouts Batch 2021-1-200CHAITANYAPas encore d'évaluation

- Development Financial InstitutionsDocument21 pagesDevelopment Financial Institutionsviveksharma51Pas encore d'évaluation

- PAT Agency Digest3Document6 pagesPAT Agency Digest3bcarPas encore d'évaluation

- Elite Choice: Variable AnnuitiesDocument2 pagesElite Choice: Variable AnnuitiesMelony LiangPas encore d'évaluation

- Import Form 2018Document6 pagesImport Form 2018tejasg82100% (2)

- Tybbi Auditing-II 2021Document88 pagesTybbi Auditing-II 2021Anonymous HackerPas encore d'évaluation

- PDFDocument3 pagesPDFArchanaNitinPas encore d'évaluation

- DSRD Ar05Document132 pagesDSRD Ar05djon888Pas encore d'évaluation

- Tira Ar 2010Document151 pagesTira Ar 2010harpzPas encore d'évaluation

- Working Paper 173 PDFDocument40 pagesWorking Paper 173 PDFRam IyerPas encore d'évaluation

- Acct 201 - Chapter 3Document31 pagesAcct 201 - Chapter 3Huy TranPas encore d'évaluation

- Enriquez Vs Sun LifeDocument1 pageEnriquez Vs Sun LifeJoel MilanPas encore d'évaluation

- Banking System in CambodiaDocument41 pagesBanking System in CambodiaYuthea Em100% (3)