Vous aimerez peut-être aussi

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Problem Session-1 - 02.03.2012Document72 pagesProblem Session-1 - 02.03.2012dewiPas encore d'évaluation

- TUTOR 9 CH22 The Short-Run Trade Off Between Inflation and UnemploymentDocument6 pagesTUTOR 9 CH22 The Short-Run Trade Off Between Inflation and Unemploymentcharlie simoPas encore d'évaluation

- Spring06 1102H Practice MCfinalDocument6 pagesSpring06 1102H Practice MCfinalcharlie simoPas encore d'évaluation

- Spring06 1102H Practice MC2Document2 pagesSpring06 1102H Practice MC2charlie simoPas encore d'évaluation

- Tutorial 13 SolutionsDocument3 pagesTutorial 13 SolutionsMartin EnilovPas encore d'évaluation

- ContentsDocument152 pagesContentsEmad RashidPas encore d'évaluation

- Supp Ques 16Document5 pagesSupp Ques 16charlie simoPas encore d'évaluation

- Supp Ques 16Document3 pagesSupp Ques 16charlie simoPas encore d'évaluation

- Problem Session-3 29.03.2012Document14 pagesProblem Session-3 29.03.2012charlie simoPas encore d'évaluation

- ContentsDocument10 pagesContentscharlie simoPas encore d'évaluation

- Problem Session-1 02.03.2012Document12 pagesProblem Session-1 02.03.2012charlie simoPas encore d'évaluation

- Chapter 002 Why Corporations Need Financial Markets and InstitutionsDocument34 pagesChapter 002 Why Corporations Need Financial Markets and InstitutionsMaria ConnerPas encore d'évaluation

- E202 F 07 Quiz 08Document11 pagesE202 F 07 Quiz 08charlie simoPas encore d'évaluation

- Practice Midterm Answers - MacroeconomicsDocument17 pagesPractice Midterm Answers - Macroeconomicsjas497100% (1)

- ECON202 2011 SampleMidterm2 FatimaDocument6 pagesECON202 2011 SampleMidterm2 Fatimacharlie simoPas encore d'évaluation

- Midterm Exam 2 SolutionsDocument8 pagesMidterm Exam 2 SolutionsEugene HwangPas encore d'évaluation

- AP Macro Practice MC Chapts 35Document22 pagesAP Macro Practice MC Chapts 35charlie simoPas encore d'évaluation

- Answers To Homework 5 Summer 2012Document14 pagesAnswers To Homework 5 Summer 2012charlie simoPas encore d'évaluation

- PLEDGE: I Have Neither Given Nor Received Unauthorized Help On This Quiz. SIGNED - PRINT NAMEDocument2 pagesPLEDGE: I Have Neither Given Nor Received Unauthorized Help On This Quiz. SIGNED - PRINT NAMEcharlie simoPas encore d'évaluation

- Chapter 16 Monetary System Practice Test 2 With AnswersDocument7 pagesChapter 16 Monetary System Practice Test 2 With Answerscharlie simoPas encore d'évaluation

- CH21Document4 pagesCH21charlie simoPas encore d'évaluation

- Chpter 21 Problems Solution Chinese VersionDocument6 pagesChpter 21 Problems Solution Chinese Versioncharlie simoPas encore d'évaluation

- AP Macro Practice MC Chapts 35Document22 pagesAP Macro Practice MC Chapts 35charlie simoPas encore d'évaluation

- Chapter 21 Answersmultiple ChoicesDocument5 pagesChapter 21 Answersmultiple Choicescharlie simoPas encore d'évaluation

- AP Macro Practice MC Chapts22Document2 pagesAP Macro Practice MC Chapts22charlie simoPas encore d'évaluation

- Answer Key4Document6 pagesAnswer Key4charlie simoPas encore d'évaluation

- Chapter 3Document9 pagesChapter 3charlie simoPas encore d'évaluation

- Answer Key 9Document4 pagesAnswer Key 9Maja TorloPas encore d'évaluation

- Lecture 05 FullDocument40 pagesLecture 05 Fullcharlie simoPas encore d'évaluation

- Lecture 04 FullDocument43 pagesLecture 04 Fullcharlie simoPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (894)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- FWC Stadium Requirements Handbook-V1.0 - LaidoutDocument1 310 pagesFWC Stadium Requirements Handbook-V1.0 - LaidoutRodrigo SimoninPas encore d'évaluation

- Screenshot 2022-08-25 at 11.49.54 AMDocument2 pagesScreenshot 2022-08-25 at 11.49.54 AMRAHUL VERMAPas encore d'évaluation

- Accounting Focus NoteDocument24 pagesAccounting Focus NoteLorelyn Ebrano AltizoPas encore d'évaluation

- Practical No 1Document4 pagesPractical No 149 Roshni PoojaryPas encore d'évaluation

- Drug Policy of OdishaDocument150 pagesDrug Policy of OdishaprayasdansanaPas encore d'évaluation

- AcademyCloudFoundations Module 01Document47 pagesAcademyCloudFoundations Module 01Dhivya rajanPas encore d'évaluation

- Mod. PCM/EV: PCM Switching and Transmission SystemDocument2 pagesMod. PCM/EV: PCM Switching and Transmission SystemShahoodulHassanPas encore d'évaluation

- M1A Version 4.6 Nov 2020Document190 pagesM1A Version 4.6 Nov 2020shaun loiPas encore d'évaluation

- Proposed Benefits MatrixDocument3 pagesProposed Benefits MatrixmunyekiPas encore d'évaluation

- tpdv100 Trading Places International Brendan Bucks OfferDocument2 pagestpdv100 Trading Places International Brendan Bucks Offerapi-232026023Pas encore d'évaluation

- Financial Institutions Management A Risk Management Approach 9th Edition Saunders Test BankDocument36 pagesFinancial Institutions Management A Risk Management Approach 9th Edition Saunders Test Banknopalsmuggler8wa100% (20)

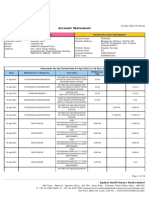

- Account Statement: Customer Information Branch/Account InformationDocument12 pagesAccount Statement: Customer Information Branch/Account InformationRohit kumarPas encore d'évaluation

- Inventory and Purchase Order ReceiptsDocument51 pagesInventory and Purchase Order ReceiptsPriya NimmagaddaPas encore d'évaluation

- Road Safety: by Dilip and RohitDocument8 pagesRoad Safety: by Dilip and RohitRohit SharmaPas encore d'évaluation

- Agriculture Retail Lending - A Presentation by Our Agriculture OfficersDocument25 pagesAgriculture Retail Lending - A Presentation by Our Agriculture OfficersrtkobPas encore d'évaluation

- Kamakoti FebDocument164 pagesKamakoti FebClaudia ShanPas encore d'évaluation

- e-StatementBRImo 063001000846564 May2023 20230602 081751Document6 pagese-StatementBRImo 063001000846564 May2023 20230602 081751Irene StevaniPas encore d'évaluation

- Instructions PDFDocument14 pagesInstructions PDFsaihejPas encore d'évaluation

- Account Statement For Account:2962002100013400: Branch DetailsDocument3 pagesAccount Statement For Account:2962002100013400: Branch DetailsBest Auto TechPas encore d'évaluation

- Travel Demand Forecasting I. Trip GenerationDocument5 pagesTravel Demand Forecasting I. Trip GenerationJaper WeakPas encore d'évaluation

- Hotel Pre Opening Full ChecklistDocument24 pagesHotel Pre Opening Full ChecklistDeo Patria HerdriantoPas encore d'évaluation

- Pertemuan #10 Andri Budiwidodo, S.Si., M.IkomDocument38 pagesPertemuan #10 Andri Budiwidodo, S.Si., M.IkomK60 NGUYỄN XUÂN HOAPas encore d'évaluation

- Bill Statement 01 2024Document3 pagesBill Statement 01 2024Satyabrat DasPas encore d'évaluation

- CH11 (SCM)Document70 pagesCH11 (SCM)babyPas encore d'évaluation

- Order To Cash FlowDocument10 pagesOrder To Cash FlowBalaji ShindePas encore d'évaluation

- APPS Rating and ReviewsDocument83 pagesAPPS Rating and ReviewsApurbh Singh KashyapPas encore d'évaluation

- Hotel Reservation Confirmation SampleDocument2 pagesHotel Reservation Confirmation SampleNabin ShakyaPas encore d'évaluation

- Vallabhi 2018 PDFDocument196 pagesVallabhi 2018 PDFSateesh KotyadaPas encore d'évaluation

- Mobile BankingDocument19 pagesMobile BankingIbe CollinsPas encore d'évaluation

- Airbnb's CRM Implementation and Customer-Facing ProcessesDocument9 pagesAirbnb's CRM Implementation and Customer-Facing Processesrohit nilawarPas encore d'évaluation