Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Goodrich Rabobank 01Document25 pagesGoodrich Rabobank 01asdadsPas encore d'évaluation

- Retail Store Survey ChecklistDocument2 pagesRetail Store Survey ChecklistArnold RadaPas encore d'évaluation

- Retail Store Team Member Return ChecklistDocument2 pagesRetail Store Team Member Return ChecklistArnold RadaPas encore d'évaluation

- TEST I-INSTRUCTION: Answer The Following Questions Below. Write Your Answer OnDocument2 pagesTEST I-INSTRUCTION: Answer The Following Questions Below. Write Your Answer OnArnold RadaPas encore d'évaluation

- Activity 2 Assessment of Learning 2Document1 pageActivity 2 Assessment of Learning 2Arnold RadaPas encore d'évaluation

- Inventory Shrinkage, Spoilage Breakage and Shortage OverageDocument3 pagesInventory Shrinkage, Spoilage Breakage and Shortage OverageArnold RadaPas encore d'évaluation

- 2016 SSS Guidebook MaternityDocument1 page2016 SSS Guidebook MaternityArnold RadaPas encore d'évaluation

- Supplemental AffidavitDocument1 pageSupplemental AffidavitArnold RadaPas encore d'évaluation

- FM-Math, Time Value of MoneyDocument2 pagesFM-Math, Time Value of Moneymaher213Pas encore d'évaluation

- Green Belt CertificationDocument4 pagesGreen Belt Certificationdeepak231982Pas encore d'évaluation

- Law Syllabus LL.M Final 1st Year 2ndDocument14 pagesLaw Syllabus LL.M Final 1st Year 2ndAnkitaPas encore d'évaluation

- Hec Group of Institutions, Haridwar Test Series - 2 (2020-2021) Financial Market and InstitutionDocument8 pagesHec Group of Institutions, Haridwar Test Series - 2 (2020-2021) Financial Market and InstitutionSamarth Agarwal0% (1)

- Chapter 8 Managing Your Credit: Personal Finance, 6e (Madura)Document27 pagesChapter 8 Managing Your Credit: Personal Finance, 6e (Madura)Huỳnh Lữ Thị NhưPas encore d'évaluation

- Crypto 101Document81 pagesCrypto 101Dat LePas encore d'évaluation

- (Semi-III) - BFG 301 Final Sept 17Document176 pages(Semi-III) - BFG 301 Final Sept 17Mohsin ShaikhPas encore d'évaluation

- Burning Issues in Banking SectorDocument17 pagesBurning Issues in Banking SectorbhavyaPas encore d'évaluation

- SKSE Securities LimitedDocument2 pagesSKSE Securities LimitedsunitdavePas encore d'évaluation

- Maham-Fee-Voucher-2023-2nd Semester-554988Document1 pageMaham-Fee-Voucher-2023-2nd Semester-554988sahabfarooqui60Pas encore d'évaluation

- Format 9A: Applicable For Individual Loans Switchover From Existing Negative Spreadover RPLR To Higher Negative SpreadDocument1 pageFormat 9A: Applicable For Individual Loans Switchover From Existing Negative Spreadover RPLR To Higher Negative SpreadANANDARAJPas encore d'évaluation

- TR6 Challan: Posts & TelegraphsDocument2 pagesTR6 Challan: Posts & TelegraphsParas RawatPas encore d'évaluation

- eIPO FAQDocument2 pageseIPO FAQvizag_vinodPas encore d'évaluation

- Us Govt Sues Both Goldman Sachs and Credit Suisse - Read Both Lawsuits HereDocument258 pagesUs Govt Sues Both Goldman Sachs and Credit Suisse - Read Both Lawsuits Here83jjmackPas encore d'évaluation

- 2 Lease of Bank Instrument - Pof Block Funds 002aDocument1 page2 Lease of Bank Instrument - Pof Block Funds 002aapi-255857738Pas encore d'évaluation

- SPOILER 1knetflix 1 1Document24 pagesSPOILER 1knetflix 1 1inrikzeraPas encore d'évaluation

- Cashless SocietyDocument65 pagesCashless SocietyAnonymous 4RApes100% (5)

- 1 PDFDocument4 pages1 PDFVishal BawanePas encore d'évaluation

- Zeta Launches All New Super Card - India's Most Secure Payment SystemDocument3 pagesZeta Launches All New Super Card - India's Most Secure Payment SystemAshish LakwaniPas encore d'évaluation

- Poi & PoaDocument14 pagesPoi & PoaKoundinyasa NishanthPas encore d'évaluation

- MCQ in Engineering Economics Part 11 ECE Board ExamDocument19 pagesMCQ in Engineering Economics Part 11 ECE Board ExamDaryl GwapoPas encore d'évaluation

- Problems Ledger Account 1 5 UnsolvedDocument11 pagesProblems Ledger Account 1 5 UnsolvedNeeraj Gugle0% (1)

- Pib ApplyDocument1 pagePib ApplykrishkpePas encore d'évaluation

- Dan Sheppard - Retail Shop Assistant: Cash Receipts Process MapDocument4 pagesDan Sheppard - Retail Shop Assistant: Cash Receipts Process MapErika EludoPas encore d'évaluation

- Mexico Payments SystemsDocument35 pagesMexico Payments SystemsVelocity_PDPas encore d'évaluation

- Dragnet ClauseDocument2 pagesDragnet ClauseAlarm GuardiansPas encore d'évaluation

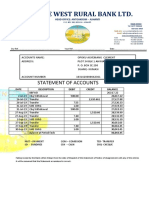

- Statement of Accounts AmansieDocument1 pageStatement of Accounts AmansieAgyei MichimelandPas encore d'évaluation

- Cash and Cash Equivalent TheoryDocument1 pageCash and Cash Equivalent TheoryExcelsia Grace A. ParreñoPas encore d'évaluation

- Card Cancellation DisclaimerDocument1 pageCard Cancellation Disclaimerambermikaela.siPas encore d'évaluation