Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Case Study KelloggsDocument4 pagesCase Study KelloggsSiti Aishah100% (1)

- Cemex Transforming A Basic Industry CompanyDocument5 pagesCemex Transforming A Basic Industry CompanyManoj Doley0% (1)

- Difference - The One-Page Method For Reimagining Your Business and Reinventing Your Marketing PDFDocument115 pagesDifference - The One-Page Method For Reimagining Your Business and Reinventing Your Marketing PDFGandhi WasuvitchayagitPas encore d'évaluation

- Task 2: Conference Schedule Project: Greenwichcollege - Edu.auDocument7 pagesTask 2: Conference Schedule Project: Greenwichcollege - Edu.auLei ShenPas encore d'évaluation

- Retail franchise-LEVI'SDocument14 pagesRetail franchise-LEVI'Snealabrata200867% (3)

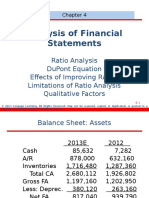

- Analysis of Financial StatementsDocument35 pagesAnalysis of Financial StatementsNicsPas encore d'évaluation

- How Brasilata Achieves Extraordinary Productivity and Innovation Through Organizational Behavior PracticesDocument30 pagesHow Brasilata Achieves Extraordinary Productivity and Innovation Through Organizational Behavior PracticesNicsPas encore d'évaluation

- Implications For The Accounting ProfessionDocument21 pagesImplications For The Accounting ProfessionNicsPas encore d'évaluation

- Nervous SystemDocument15 pagesNervous SystemNicsPas encore d'évaluation

- Endocrine System - LectureDocument5 pagesEndocrine System - LectureNicsPas encore d'évaluation

- Customer Centered Brand Management - Rust, Zeithaml, Lemon PDFDocument10 pagesCustomer Centered Brand Management - Rust, Zeithaml, Lemon PDFHai NguyenPas encore d'évaluation

- Bagnol FSDocument55 pagesBagnol FSRosemarie EspinaPas encore d'évaluation

- Priprema Za Kolokvijum 2 Engleski JezikDocument23 pagesPriprema Za Kolokvijum 2 Engleski JezikDarko ĐurićPas encore d'évaluation

- International Marketing Strategy - Case StudyDocument4 pagesInternational Marketing Strategy - Case StudyndumiePas encore d'évaluation

- Inventory Management: Presented ByDocument11 pagesInventory Management: Presented ByChandan DuttaPas encore d'évaluation

- Strategic Management Report On Unilever PakistanDocument23 pagesStrategic Management Report On Unilever PakistanAbdur RehmanPas encore d'évaluation

- Navbharat TimesDocument14 pagesNavbharat TimesswatantraPas encore d'évaluation

- A Feasibility Study Business Plan On PouDocument8 pagesA Feasibility Study Business Plan On PouKoghorong ShepherdPas encore d'évaluation

- Market Testing Kelompok 6Document23 pagesMarket Testing Kelompok 6RutCahayaHutapeaPas encore d'évaluation

- Vitasoy Celebrates Its 70th PDFDocument5 pagesVitasoy Celebrates Its 70th PDFgary3lauPas encore d'évaluation

- Personal SWOT Analysis and Analysis of Wal-MartDocument10 pagesPersonal SWOT Analysis and Analysis of Wal-MartAli RehmatPas encore d'évaluation

- Case Study On Sunsilk GogDocument28 pagesCase Study On Sunsilk GogPrithwish KotianPas encore d'évaluation

- BhelDocument28 pagesBhelRahul SahuPas encore d'évaluation

- Projec FNL 1 PDFDocument101 pagesProjec FNL 1 PDFJøhn CharleyPas encore d'évaluation

- Entrepreneurial Marketing Performance of Cottage Industries in Kendal RegencyDocument4 pagesEntrepreneurial Marketing Performance of Cottage Industries in Kendal RegencyOzal KhanPas encore d'évaluation

- Nestlé Caja Roja Case StudyDocument7 pagesNestlé Caja Roja Case StudyNerea EscribanoPas encore d'évaluation

- Elektrisiteit 1eDocument6 pagesElektrisiteit 1eSanthosh RMPas encore d'évaluation

- Red OakDocument187 pagesRed OakmattpaulsPas encore d'évaluation

- 974559Document14 pages974559SourabhPawadePas encore d'évaluation

- Hero Motocorp Industry & Market Leader AnalysisDocument20 pagesHero Motocorp Industry & Market Leader AnalysisNivetha0% (1)

- Bibliography FINALDocument5 pagesBibliography FINALMina Klee ChapmanPas encore d'évaluation

- IzzebookDocument28 pagesIzzebookapi-251024168Pas encore d'évaluation

- Vice President Receivables Manager in Delaware Maryland Resume John TonettiDocument3 pagesVice President Receivables Manager in Delaware Maryland Resume John TonettijohntonettiPas encore d'évaluation

- Marketing 5th Edition Grewal Solutions ManualDocument25 pagesMarketing 5th Edition Grewal Solutions Manualaureliaeirayetu6s100% (26)

- HULDocument49 pagesHULsaq4u100% (1)