Vous aimerez peut-être aussi

- Summary of Ahmed Siddiqui & Nicholas Straight's The Anatomy of the SwipeD'EverandSummary of Ahmed Siddiqui & Nicholas Straight's The Anatomy of the SwipePas encore d'évaluation

- How To File TDS On The Sale of PropertyDocument12 pagesHow To File TDS On The Sale of PropertyManjukesanPas encore d'évaluation

- Agent Banking Uganda Handbook: A simple guide to starting and running a profitable agent banking business in UgandaD'EverandAgent Banking Uganda Handbook: A simple guide to starting and running a profitable agent banking business in UgandaPas encore d'évaluation

- Multiple Form 26QB For Multiple Buyers, Sellers & Other FAQSDocument5 pagesMultiple Form 26QB For Multiple Buyers, Sellers & Other FAQSprashantgeminiPas encore d'évaluation

- Tax Deducted at Source - I: KPPM & AssociatesDocument63 pagesTax Deducted at Source - I: KPPM & AssociatesSaksham JoshiPas encore d'évaluation

- Process of 26QBDocument15 pagesProcess of 26QBthetrilight2023Pas encore d'évaluation

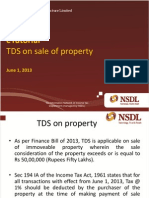

- Etutorial - TDS On Property - Etax-Immediately PDFDocument24 pagesEtutorial - TDS On Property - Etax-Immediately PDFkunalji_jainPas encore d'évaluation

- Guidance Note On TDS On Property, Payment Procedure & Points To RememberDocument6 pagesGuidance Note On TDS On Property, Payment Procedure & Points To RememberAman VermaPas encore d'évaluation

- NG Rtgs Ver 16th June14Document3 pagesNG Rtgs Ver 16th June14Supreeth SharmaPas encore d'évaluation

- Guidelines For TDS Deduction On Purchase of Immovable PropertyDocument4 pagesGuidelines For TDS Deduction On Purchase of Immovable Propertymib_santoshPas encore d'évaluation

- TDS On Purchase of Immovable Property in India - V1Document9 pagesTDS On Purchase of Immovable Property in India - V1prathinareddyPas encore d'évaluation

- TDSDocument18 pagesTDSPratik NaikPas encore d'évaluation

- Maharashtra State Electricity Distribution Co. Ltd. bill detailsDocument2 pagesMaharashtra State Electricity Distribution Co. Ltd. bill detailsShubham GuptaPas encore d'évaluation

- Merchant Integration Services IN-DL66770927172413R: E-StampDocument6 pagesMerchant Integration Services IN-DL66770927172413R: E-StampKalp TermailPas encore d'évaluation

- Etutorial - TDS On PropertyDocument20 pagesEtutorial - TDS On PropertyarunkumarsundarPas encore d'évaluation

- AX Educted at Ource - I: KPPM & AssociatesDocument67 pagesAX Educted at Ource - I: KPPM & AssociatesSaksham JoshiPas encore d'évaluation

- Section 194C: TDS On ContractDocument5 pagesSection 194C: TDS On ContractwaghulePas encore d'évaluation

- Generate Multiple Demand Drafts from Deposit AccountDocument40 pagesGenerate Multiple Demand Drafts from Deposit Accountmevrick_guyPas encore d'évaluation

- CC Mitc21122022Document28 pagesCC Mitc21122022jeetPas encore d'évaluation

- Academic Fees Payment GuidelinesDocument2 pagesAcademic Fees Payment GuidelinesCrackPODPas encore d'évaluation

- TDS FAQsDocument4 pagesTDS FAQsMaxiPas encore d'évaluation

- TDS Understanding NotesDocument6 pagesTDS Understanding NotesnaysarPas encore d'évaluation

- SEZONLINE_ONLINE_DUTY_PAYMENT_USER_MANUALDocument12 pagesSEZONLINE_ONLINE_DUTY_PAYMENT_USER_MANUALDUX Durgesh YadavPas encore d'évaluation

- Import Data Processing & Monitoring System - Proposed Process and Estimated ImpactDocument6 pagesImport Data Processing & Monitoring System - Proposed Process and Estimated ImpactSachin BanePas encore d'évaluation

- Get a 3000 personal loan at 29.95% interestDocument4 pagesGet a 3000 personal loan at 29.95% interestSiddhantPas encore d'évaluation

- Cbci Payment Center AgreementDocument16 pagesCbci Payment Center AgreementmrsjpendletonPas encore d'évaluation

- FreoPay KFS MYMT2021123100529522Document2 pagesFreoPay KFS MYMT2021123100529522McLarenPas encore d'évaluation

- Loan Sanction-Letter181240016761170869Document3 pagesLoan Sanction-Letter181240016761170869Sanjay MohapatraPas encore d'évaluation

- Tax Planning and ProceduresDocument32 pagesTax Planning and ProceduresSujata DongrePas encore d'évaluation

- Merchant Emi TNCDocument5 pagesMerchant Emi TNCsoban moriwalaPas encore d'évaluation

- FAQs on cash withdrawal TDS rulesDocument2 pagesFAQs on cash withdrawal TDS rulesSuryanarayana DPas encore d'évaluation

- TDS TediousDocument30 pagesTDS Tediousxavier albuquerquePas encore d'évaluation

- RMC No. 004-21 - Guidlines in Filing Tax Return and Required AttachmentsDocument9 pagesRMC No. 004-21 - Guidlines in Filing Tax Return and Required AttachmentsVence EugalcaPas encore d'évaluation

- Tax. 23Document18 pagesTax. 23RahulPas encore d'évaluation

- New TDS rules under Finance Act 2009Document8 pagesNew TDS rules under Finance Act 2009sheetalneelkPas encore d'évaluation

- Merchant integration services formDocument6 pagesMerchant integration services formbaraniPas encore d'évaluation

- Reference Guide South African Revenue Service Payment Rules: Effective Date 09.11.2010Document8 pagesReference Guide South African Revenue Service Payment Rules: Effective Date 09.11.2010biccard7338Pas encore d'évaluation

- Tax Information NetworkDocument1 pageTax Information NetworkVyapar NitiPas encore d'évaluation

- Proposal AgregatorDocument20 pagesProposal Agregatorvier emPas encore d'évaluation

- Kargo Payment Policy GuideDocument5 pagesKargo Payment Policy GuideRichard WijayaPas encore d'évaluation

- NRI TDS On PropertyDocument3 pagesNRI TDS On PropertyJatin AgarwalPas encore d'évaluation

- Tax Deducted at SourceDocument5 pagesTax Deducted at Sourceshubhra_jais6888Pas encore d'évaluation

- Faqs On GSTDocument18 pagesFaqs On GSTmsanrxlPas encore d'évaluation

- GST Faq PDFDocument18 pagesGST Faq PDFsiva moorthyPas encore d'évaluation

- TDS Awareness Programme SummaryDocument60 pagesTDS Awareness Programme SummarymahadevavrPas encore d'évaluation

- Export Advance Payment - Branch ProposalDocument2 pagesExport Advance Payment - Branch ProposalKumar SwamyPas encore d'évaluation

- Channel Incentive Policy 20-21Document5 pagesChannel Incentive Policy 20-21kushrohitPas encore d'évaluation

- CORS Subscription Plans-13Document11 pagesCORS Subscription Plans-13kkumar.amitPas encore d'évaluation

- TDS Tutorial - AdhirajDocument8 pagesTDS Tutorial - AdhirajShailendraShuklaPas encore d'évaluation

- Summary of Rates and FeesDocument2 pagesSummary of Rates and Fees7fr8cr5wt2Pas encore d'évaluation

- For Tds On Non SalaryDocument39 pagesFor Tds On Non SalaryicahimanshumehtaPas encore d'évaluation

- How To Book Property Under SchemesDocument15 pagesHow To Book Property Under SchemesHarshit BhatiaPas encore d'évaluation

- Tds-Legal OpinionDocument2 pagesTds-Legal OpinionSATYANARAYANA MOTAMARRIPas encore d'évaluation

- Central University of South Bihar: Project WorkDocument17 pagesCentral University of South Bihar: Project WorkPriyaranjan SinghPas encore d'évaluation

- TDS at A Glance 2013-14 BookDocument34 pagesTDS at A Glance 2013-14 Bookajad babuPas encore d'évaluation

- TDS Rates and Important DatesDocument3 pagesTDS Rates and Important DatesSadhvi BansalPas encore d'évaluation

- Acrobat Document - TDS - OfflineDocument28 pagesAcrobat Document - TDS - OfflineLuxna SureshPas encore d'évaluation

- BO in FinacleDocument9 pagesBO in FinacleShailendra MishraPas encore d'évaluation

- Debit Card Service ChargesDocument3 pagesDebit Card Service ChargesVinodkumar ShethPas encore d'évaluation

- Covenants News Article PDFDocument3 pagesCovenants News Article PDFprafulvg123Pas encore d'évaluation

- India Skill Report-2019Document56 pagesIndia Skill Report-2019Roshan SuhailPas encore d'évaluation

- Covenants News Article PDFDocument3 pagesCovenants News Article PDFprafulvg123Pas encore d'évaluation

- GroupsDocument1 pageGroupsprafulvg123Pas encore d'évaluation

- TDS Process DocumentationDocument14 pagesTDS Process Documentationprafulvg123Pas encore d'évaluation

- GMLR EC Report PDFDocument136 pagesGMLR EC Report PDFprafulvg123Pas encore d'évaluation

- ESM 17 18 EngDocument309 pagesESM 17 18 EnglovelynaturePas encore d'évaluation

- BharatMala CorridorsDocument26 pagesBharatMala Corridorskarthickpadmanaban100% (1)

- Indias Changing Automobile FinanceDocument6 pagesIndias Changing Automobile FinanceAnshul GuptaPas encore d'évaluation

- BrochureDocument23 pagesBrochureprafulvg123Pas encore d'évaluation

- BrochureDocument23 pagesBrochureprafulvg123Pas encore d'évaluation

- Know Your Ward Data FinalDocument174 pagesKnow Your Ward Data Finalprafulvg123Pas encore d'évaluation

- The Indian Contract Act 1872Document47 pagesThe Indian Contract Act 1872Dilfaraz KalawatPas encore d'évaluation

- Request For ESCO Contract II PDFDocument22 pagesRequest For ESCO Contract II PDFjoechengshPas encore d'évaluation

- Marie Curie Presentation Financial ReportingDocument28 pagesMarie Curie Presentation Financial ReportingArmantoCepongPas encore d'évaluation

- AP-5906 ReceivablesDocument5 pagesAP-5906 Receivablesjhouvan100% (1)

- Internship Report AB BankDocument85 pagesInternship Report AB BankDhoni KhanPas encore d'évaluation

- Credit Card NumbersDocument3 pagesCredit Card NumbersAnonymous 4LxqXiX67% (3)

- Updated NullDocument1 965 pagesUpdated Nullazsial4456Pas encore d'évaluation

- Comparative Analysis of HDFC Bank and SBIDocument37 pagesComparative Analysis of HDFC Bank and SBIsiddhantkamdarPas encore d'évaluation

- My Card Place PDFDocument3 pagesMy Card Place PDFDIGITAL PATRIOTSPas encore d'évaluation

- A Simple Explanation of How Money Moves Around The Banking System - Richard Gendal BrownDocument12 pagesA Simple Explanation of How Money Moves Around The Banking System - Richard Gendal BrownAlijaNuhićPas encore d'évaluation

- Capital Market and NSDL Book 3Document103 pagesCapital Market and NSDL Book 3mhussainPas encore d'évaluation

- Preparing SFP of Single Propriertorship BusinessDocument18 pagesPreparing SFP of Single Propriertorship Businessjudith100% (2)

- Philippine Interpretations Committee Operating ProceduresDocument5 pagesPhilippine Interpretations Committee Operating ProceduresJere Mae Bertuso TaganasPas encore d'évaluation

- Vedika Project ReportDocument86 pagesVedika Project ReportVedika KeshariPas encore d'évaluation

- Sindh ABS 0910Document86 pagesSindh ABS 0910Wajiha SaeedPas encore d'évaluation

- Philippine Supreme Court Rules on Inheritance Tax CaseDocument9 pagesPhilippine Supreme Court Rules on Inheritance Tax CaseChristianneDominiqueGravosoPas encore d'évaluation

- For Resident Individual Account Holder: Page 1 of 6Document6 pagesFor Resident Individual Account Holder: Page 1 of 6MOHAN SPas encore d'évaluation

- Truth in LendingDocument5 pagesTruth in LendingJexelle Marteen Tumibay PestañoPas encore d'évaluation

- Firstsem SPCL DC2016Document138 pagesFirstsem SPCL DC2016Gelo LeañoPas encore d'évaluation

- MECO vs Yatco: Tax on Insurance Premiums Paid to Foreign CorpsDocument5 pagesMECO vs Yatco: Tax on Insurance Premiums Paid to Foreign CorpsVida MariePas encore d'évaluation

- Bank of MaharashtraDocument91 pagesBank of MaharashtraArun Savukar67% (3)

- Case-Metropolitan Bank v. CA 194 SCRA 169Document5 pagesCase-Metropolitan Bank v. CA 194 SCRA 169Ouro BorosPas encore d'évaluation

- Strategies Adopted and Swot AnalysisDocument12 pagesStrategies Adopted and Swot AnalysisMehul KhonaPas encore d'évaluation

- Problem 10 and 13Document2 pagesProblem 10 and 13jiiPas encore d'évaluation

- ToR Audit TenderDocument9 pagesToR Audit TenderIslamicRelief AlbaniaPas encore d'évaluation

- Parabolic SARDocument2 pagesParabolic SARprivatelogic100% (2)

- 397 SCRA 651 - Producers Bank of The Philippines Vs Hon. Court of AppealsDocument3 pages397 SCRA 651 - Producers Bank of The Philippines Vs Hon. Court of AppealsRengie GaloPas encore d'évaluation

- Final Reports by SunilDocument34 pagesFinal Reports by Sunilryu_clan100% (3)

- Foia 2011.10.106Document115 pagesFoia 2011.10.106Judicial Watch, Inc.Pas encore d'évaluation

- SAP Process - Cash Sales and Rush OrderDocument2 pagesSAP Process - Cash Sales and Rush OrderpraveennbsPas encore d'évaluation