Vous aimerez peut-être aussi

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideD'EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuidePas encore d'évaluation

- Chapter 13Document11 pagesChapter 13Maya HamdyPas encore d'évaluation

- Company AccountingDocument28 pagesCompany AccountingBeanka PaulPas encore d'évaluation

- Chapter 18 Shareholders' Equity: Paid-In Capital Fundamental Share RightsDocument9 pagesChapter 18 Shareholders' Equity: Paid-In Capital Fundamental Share RightsSteeeeeeeephPas encore d'évaluation

- Chapter 13Document13 pagesChapter 13Mondy MondyPas encore d'évaluation

- IASSS16e Ch13.Ab - AzDocument28 pagesIASSS16e Ch13.Ab - AzLovely DungcaPas encore d'évaluation

- Financial Accounting: Sources of Capital - Equity and DebtDocument25 pagesFinancial Accounting: Sources of Capital - Equity and DebtJHANVI LAKRAPas encore d'évaluation

- CAPE Recording Capital Stock & Reverses TransactionDocument49 pagesCAPE Recording Capital Stock & Reverses TransactionOckouri BarnesPas encore d'évaluation

- Excercises Dividend PolicyDocument30 pagesExcercises Dividend PolicyHero CoursePas encore d'évaluation

- Retained Earnings and Treasury TransactionsDocument25 pagesRetained Earnings and Treasury TransactionsMark LouiePas encore d'évaluation

- Reporting and Analyzing Stockholders' EquityDocument3 pagesReporting and Analyzing Stockholders' EquityAreeba QureshiPas encore d'évaluation

- Company Financial Statements TopicsDocument40 pagesCompany Financial Statements TopicsThương ĐỗPas encore d'évaluation

- Chapter 7 Stockholers Equity FinalDocument77 pagesChapter 7 Stockholers Equity FinalSampanna ShresthaPas encore d'évaluation

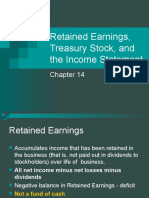

- Retained Earnings, Treasury Stock, and The Income StatementDocument43 pagesRetained Earnings, Treasury Stock, and The Income Statementshiawsyan_chanPas encore d'évaluation

- Lecture - 9 - Income - and - Equity - NUS ACC1002 2020 SpringDocument43 pagesLecture - 9 - Income - and - Equity - NUS ACC1002 2020 SpringZenyuiPas encore d'évaluation

- EquityDocument34 pagesEquityVe DekPas encore d'évaluation

- Finance Management 4Document26 pagesFinance Management 4charithPas encore d'évaluation

- Capital Structure and ReservesDocument40 pagesCapital Structure and ReservesEverjoice ChatoraPas encore d'évaluation

- Intermediate AccountingDocument69 pagesIntermediate AccountingYuan ZhongPas encore d'évaluation

- Shareholders' EquityDocument120 pagesShareholders' EquitySsewa AhmedPas encore d'évaluation

- ch11 2Document58 pagesch11 2X YlmarixePas encore d'évaluation

- Af210 WeekDocument30 pagesAf210 WeekAvisha SinghPas encore d'évaluation

- Dividend PolicyDocument52 pagesDividend PolicyANISH KUMARPas encore d'évaluation

- Corporations Part 3Document20 pagesCorporations Part 3Miss LunaPas encore d'évaluation

- Owners' Equity Chapter SummaryDocument29 pagesOwners' Equity Chapter SummaryTPas encore d'évaluation

- Dividend Policy Dividend PolicyDocument42 pagesDividend Policy Dividend Policyshanzah amirPas encore d'évaluation

- Equity FinancingDocument53 pagesEquity FinancingGaluh Boga KuswaraPas encore d'évaluation

- Dividend Decision and Stock Dividend-Repurchase-SplitDocument56 pagesDividend Decision and Stock Dividend-Repurchase-SplitA MerchantPas encore d'évaluation

- Chapter 17 1Document26 pagesChapter 17 1Diệu Linh NguyễnPas encore d'évaluation

- The Corporate Form of OrganizationDocument7 pagesThe Corporate Form of OrganizationRabie HarounPas encore d'évaluation

- Corporation Is: Separate Legal Entity Created by Law: Corporations and Stockholders EquityDocument25 pagesCorporation Is: Separate Legal Entity Created by Law: Corporations and Stockholders EquityCPas encore d'évaluation

- Chapter (14) Corporations: Dividends, Retained Earnings, and Income Reporting DividendsDocument11 pagesChapter (14) Corporations: Dividends, Retained Earnings, and Income Reporting DividendsMondy MondyPas encore d'évaluation

- Tutorial 2Document6 pagesTutorial 2杰克 l孙Pas encore d'évaluation

- Chapter 10 - Accounting For Equity: Learning ObjectivesDocument11 pagesChapter 10 - Accounting For Equity: Learning ObjectivesBình Trần ThanhPas encore d'évaluation

- 16 Dividend PolicyDocument32 pages16 Dividend Policyraniiqasari2023Pas encore d'évaluation

- Company Accounts TheoryDocument9 pagesCompany Accounts TheoryEshal KhanPas encore d'évaluation

- Accounting For Corporations IIIDocument25 pagesAccounting For Corporations IIIibrahim mohamedPas encore d'évaluation

- Accounting For Corporations IIDocument25 pagesAccounting For Corporations IIibrahim mohamedPas encore d'évaluation

- Share CapitalDocument6 pagesShare CapitalAashi DharwalPas encore d'évaluation

- C450 - Shareholder's Equity - Lecture NotesDocument13 pagesC450 - Shareholder's Equity - Lecture NotesFreelansirPas encore d'évaluation

- Financial Reporting and Analysis: - Session 12-Professor Raluca Ratiu, PHDDocument45 pagesFinancial Reporting and Analysis: - Session 12-Professor Raluca Ratiu, PHDDaniel YebraPas encore d'évaluation

- Common and Preferred Stock TypesDocument12 pagesCommon and Preferred Stock TypesAmna ImranPas encore d'évaluation

- Accounting Capital+Stock+TransactionsDocument17 pagesAccounting Capital+Stock+TransactionsOckouri BarnesPas encore d'évaluation

- Dividend PolicyDocument52 pagesDividend PolicyKlaus Mikaelson100% (1)

- Statement of Equity ChangesDocument7 pagesStatement of Equity ChangesHikmət RüstəmovPas encore d'évaluation

- RECORDING Shares 1 Issue & DividendsDocument4 pagesRECORDING Shares 1 Issue & DividendsDonald SPas encore d'évaluation

- FIN 451 Corporate Finance Ii: Uses of Free Cash FlowDocument5 pagesFIN 451 Corporate Finance Ii: Uses of Free Cash FlowDaniel GarciaPas encore d'évaluation

- Meeting 9 - Company Financial StatementsDocument42 pagesMeeting 9 - Company Financial StatementsHelen FebrianaPas encore d'évaluation

- Chap 13Document33 pagesChap 13Boo LePas encore d'évaluation

- Securities Industries Essentials Summary NotesDocument163 pagesSecurities Industries Essentials Summary NotesBAnne LabelPas encore d'évaluation

- Dividend Decision and Stock Dividend-Repurchase-SplitDocument56 pagesDividend Decision and Stock Dividend-Repurchase-SplitRoshniPas encore d'évaluation

- Introduction To Accounting 2 Organization and Capital Stock TransactionsDocument17 pagesIntroduction To Accounting 2 Organization and Capital Stock Transactionsalice horanPas encore d'évaluation

- sheet 5 E1 ازهرDocument9 pagessheet 5 E1 ازهرmagdy kamelPas encore d'évaluation

- Issue of Shares ProblemsDocument37 pagesIssue of Shares ProblemsgeddadaarunPas encore d'évaluation

- Chapter 17 Corporate FinanceDocument27 pagesChapter 17 Corporate Financecherryl marianoPas encore d'évaluation

- Dividends and Other PayoutsDocument26 pagesDividends and Other Payoutsmger2000Pas encore d'évaluation

- Accounting 3 & 4 - Shareholders' Equity, Retained Earnings, and DividendsDocument10 pagesAccounting 3 & 4 - Shareholders' Equity, Retained Earnings, and DividendsLaurio, Genebabe TagubarasPas encore d'évaluation

- 110 Corporate Finance PDFDocument23 pages110 Corporate Finance PDFMohit WaniPas encore d'évaluation

- CFMP - Bloomberg Course: Your GuideDocument47 pagesCFMP - Bloomberg Course: Your GuideWilliam BoschPas encore d'évaluation

- INTERNAL CONTROL SYSTEM GUIDEDocument64 pagesINTERNAL CONTROL SYSTEM GUIDETeal JacobsPas encore d'évaluation

- Accounting, Unit 1 - Topic 1Document68 pagesAccounting, Unit 1 - Topic 1Teal JacobsPas encore d'évaluation

- Address: 4 East Avenue, Ocho Rios City: St. Ann Telephone: (876) 534-7869 Fax: (876) 544-6708Document2 pagesAddress: 4 East Avenue, Ocho Rios City: St. Ann Telephone: (876) 534-7869 Fax: (876) 544-6708Teal JacobsPas encore d'évaluation

- Definition of Literary Terms and ConceptsDocument8 pagesDefinition of Literary Terms and ConceptsTeal JacobsPas encore d'évaluation

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Spanish Action 789Document2 pagesSpanish Action 789Teal JacobsPas encore d'évaluation

- National Health Fund Human Resource Department 25 Dominica Drive Kingston 5Document2 pagesNational Health Fund Human Resource Department 25 Dominica Drive Kingston 5Teal JacobsPas encore d'évaluation

- Green Pond High School BAS Snack Corner SBADocument35 pagesGreen Pond High School BAS Snack Corner SBAbeenie manPas encore d'évaluation

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- National Health Fund Human Resource Department 25 Dominica Drive Kingston 5Document2 pagesNational Health Fund Human Resource Department 25 Dominica Drive Kingston 5Teal JacobsPas encore d'évaluation

- Problem Solving Mark Scheme Grade 11Document3 pagesProblem Solving Mark Scheme Grade 11Teal JacobsPas encore d'évaluation

- Science RevisionDocument3 pagesScience RevisionTeal JacobsPas encore d'évaluation

- Episode 607: Specific Heat Capacity: Changes Phase From A Solid To A Liquid or Liquid To A GasDocument19 pagesEpisode 607: Specific Heat Capacity: Changes Phase From A Solid To A Liquid or Liquid To A GasMuhamadMarufPas encore d'évaluation

- 122 Lab Sample Report Rev 2Document7 pages122 Lab Sample Report Rev 2Teal JacobsPas encore d'évaluation

- Dashy's Boutique Christmas Sale Announcement - Up to 30% Off Top BrandsDocument2 pagesDashy's Boutique Christmas Sale Announcement - Up to 30% Off Top BrandsTeal JacobsPas encore d'évaluation

- 6-3 The Specific Heat of Four Different MetalsDocument3 pages6-3 The Specific Heat of Four Different MetalsTeal JacobsPas encore d'évaluation

- 1102 Lab 1 CalorimetryDocument28 pages1102 Lab 1 CalorimetryTeal JacobsPas encore d'évaluation

- 2013 May Past Paper (Security Measures)Document1 page2013 May Past Paper (Security Measures)Teal JacobsPas encore d'évaluation

- 122 Lab Sample Report Rev 2Document7 pages122 Lab Sample Report Rev 2Teal JacobsPas encore d'évaluation

- CH 6Document57 pagesCH 6SegniPas encore d'évaluation

- FAR04-14 - Basic SHEDocument9 pagesFAR04-14 - Basic SHEAi NatangcopPas encore d'évaluation

- F - FINAL COMPREHENSIVE EXAM GELERA - Docx - 140790664Document16 pagesF - FINAL COMPREHENSIVE EXAM GELERA - Docx - 140790664Christian Jade Siccuan AglibutPas encore d'évaluation

- Valuation of Securities: Calculating Market ValuesDocument3 pagesValuation of Securities: Calculating Market ValuesAurelia RijiPas encore d'évaluation

- Article - Simplifying Earnings Per Share By: Dr. Ciaran Connolly, D. Phil, MBA, FCA. Examiner: Professional 2 - Advanced Corporate ReportingDocument13 pagesArticle - Simplifying Earnings Per Share By: Dr. Ciaran Connolly, D. Phil, MBA, FCA. Examiner: Professional 2 - Advanced Corporate ReportingsmlingwaPas encore d'évaluation

- Notes On Indian Business EnviornmentDocument43 pagesNotes On Indian Business Enviornmentsindhumegharaj100% (28)

- MSQ-10 - Cost of CapitalDocument11 pagesMSQ-10 - Cost of CapitalElin SaldañaPas encore d'évaluation

- Chap 010Document50 pagesChap 010mas azizPas encore d'évaluation

- Baliwag Polytechnic College: Financial Accounting and Reporting A. AlmineDocument3 pagesBaliwag Polytechnic College: Financial Accounting and Reporting A. AlmineCain Cyrus MonderoPas encore d'évaluation

- Accounting Textbook Solutions - 72Document19 pagesAccounting Textbook Solutions - 72acc-expertPas encore d'évaluation

- 8515825479604441Document4 pages8515825479604441Fransisco Karindra CarakaPas encore d'évaluation

- Supreme Court Rules on Redemption of Preferred SharesDocument6 pagesSupreme Court Rules on Redemption of Preferred SharesDanica Godornes100% (1)

- 09 How Low Can It GoDocument3 pages09 How Low Can It GoHéctor Eduardo Moreno Sandoval75% (4)

- Level 1 Quizmaster'sDocument9 pagesLevel 1 Quizmaster'ssarahbeePas encore d'évaluation

- MCQfrom QuizesDocument16 pagesMCQfrom QuizesFahad100% (1)

- Ratios TaskDocument3 pagesRatios Taskiceman2167Pas encore d'évaluation

- Chapter 16Document10 pagesChapter 16GONZALES, MICA ANGEL A.Pas encore d'évaluation

- AP-100 (Audit of Shareholders' Equity)Document8 pagesAP-100 (Audit of Shareholders' Equity)Gwyneth CartallaPas encore d'évaluation

- MFRD - LaliteshDocument35 pagesMFRD - LaliteshRajivVyasPas encore d'évaluation

- Capital of The CompanyDocument28 pagesCapital of The CompanyLusajo MwakibingaPas encore d'évaluation

- ICICI BANK AR 2019 Directors Report PDFDocument71 pagesICICI BANK AR 2019 Directors Report PDFSailendran MenattamaiPas encore d'évaluation

- Financial Statement AnalysisDocument50 pagesFinancial Statement AnalysisRishin Suresh S100% (1)

- Buy Back Offer (Company Update)Document60 pagesBuy Back Offer (Company Update)Shyam SunderPas encore d'évaluation

- CF 2Document114 pagesCF 2Vishnu VardhanPas encore d'évaluation

- Financial Statement Analysis: Charles H. GibsonDocument47 pagesFinancial Statement Analysis: Charles H. Gibsonmohamed100% (2)

- Pas 28Document3 pagesPas 28Jay JavierPas encore d'évaluation

- Important questions on company lawDocument21 pagesImportant questions on company lawshakthi jayanthPas encore d'évaluation

- Accounting for Share CapitalDocument8 pagesAccounting for Share CapitalMayank DuhalniPas encore d'évaluation

- Satyajit 2Document30 pagesSatyajit 2Raihan WorldwidePas encore d'évaluation

- Abdul Samad (01-112182-043)Document5 pagesAbdul Samad (01-112182-043)ABDUL SAMADPas encore d'évaluation