Vous aimerez peut-être aussi

- TWBIN19Document3 pagesTWBIN191NessaPas encore d'évaluation

- NATS Test MaterialsDocument25 pagesNATS Test Materials1NessaPas encore d'évaluation

- WEB PORTALS - PPT Stephen SeniorDocument9 pagesWEB PORTALS - PPT Stephen Senior1NessaPas encore d'évaluation

- Report of The DLF Electronic Resource Management Initiative Appendix D: Entity Relationship Diagram For Electronic Resource ManagementDocument12 pagesReport of The DLF Electronic Resource Management Initiative Appendix D: Entity Relationship Diagram For Electronic Resource Management1NessaPas encore d'évaluation

- Report of The DLF Electronic Resource Management Initiative Appendix D: Entity Relationship Diagram For Electronic Resource ManagementDocument12 pagesReport of The DLF Electronic Resource Management Initiative Appendix D: Entity Relationship Diagram For Electronic Resource Management1NessaPas encore d'évaluation

- CAPE NOTES Unit 2 Module 1 Database Management-1Document15 pagesCAPE NOTES Unit 2 Module 1 Database Management-11NessaPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (120)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- 1 Liquidity RiskDocument8 pages1 Liquidity RiskShreyanko GhosalPas encore d'évaluation

- Forex 1Document53 pagesForex 1Irwan HeriyantoPas encore d'évaluation

- The Consumer Buying Behavior in The Digital AgeDocument10 pagesThe Consumer Buying Behavior in The Digital AgeAleksandar MihajlovićPas encore d'évaluation

- CHP 4 McqsDocument8 pagesCHP 4 McqsNasar IqbalPas encore d'évaluation

- LGFV Outreach Deck - April 2022 FinalDocument26 pagesLGFV Outreach Deck - April 2022 FinalJason ZhuPas encore d'évaluation

- Hull OFOD10e MultipleChoice Questions Only Ch08Document4 pagesHull OFOD10e MultipleChoice Questions Only Ch08Kevin Molly KamrathPas encore d'évaluation

- ItrDocument33 pagesItrzeno samaPas encore d'évaluation

- CH 14Document28 pagesCH 14Nazir Ahmed ZihadPas encore d'évaluation

- The Wall Street Crash of 1929Document11 pagesThe Wall Street Crash of 1929Ramona AlinaPas encore d'évaluation

- Global Securities OperationsDocument264 pagesGlobal Securities Operationsnishant hawelia100% (1)

- Gujarat Technological UniversityDocument2 pagesGujarat Technological UniversityShyamsunder SinghPas encore d'évaluation

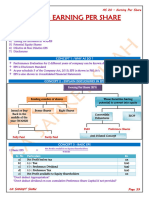

- As 20 - Earning Per Share CH-4Document5 pagesAs 20 - Earning Per Share CH-4lucifersdevil68Pas encore d'évaluation

- JPM Bitcoin ReportDocument86 pagesJPM Bitcoin ReportknwongabPas encore d'évaluation

- An Alternative View of Risk and Return: The Apt: Mcgraw-Hill/Irwin Corporate Finance, 7/EDocument27 pagesAn Alternative View of Risk and Return: The Apt: Mcgraw-Hill/Irwin Corporate Finance, 7/ERazzARazaPas encore d'évaluation

- 69 Aditya Pandey DMBA Case Study 1Document8 pages69 Aditya Pandey DMBA Case Study 1aditya pandey100% (1)

- Chapter 1 - Introduction To Financial MarketsDocument8 pagesChapter 1 - Introduction To Financial MarketsReianne Keith Zamora YanesPas encore d'évaluation

- SDL NSDLDocument2 pagesSDL NSDLNeha KrishnaniPas encore d'évaluation

- Problem No. 1: QuestionsDocument2 pagesProblem No. 1: QuestionsRen Ey100% (1)

- PR - Order in The Matter of Lee Capital Services Private LimitedDocument2 pagesPR - Order in The Matter of Lee Capital Services Private LimitedShyam SunderPas encore d'évaluation

- Kohler DCFDocument1 pageKohler DCFJennifer Langton100% (1)

- International Finance CaseDocument7 pagesInternational Finance CaseAl-Imran Bin KhodadadPas encore d'évaluation

- Types and Costs of Financial Capital: True-False QuestionsDocument8 pagesTypes and Costs of Financial Capital: True-False Questionsbia070386Pas encore d'évaluation

- Chapter 7 - Portfolio Theory and The Capital Asset Model Pricing (Compatibility Mode)Document21 pagesChapter 7 - Portfolio Theory and The Capital Asset Model Pricing (Compatibility Mode)Hanh TranPas encore d'évaluation

- ICICI Mutual Fund: Belgaum Institute of Management Studies MBADocument68 pagesICICI Mutual Fund: Belgaum Institute of Management Studies MBAPrasad KumbharPas encore d'évaluation

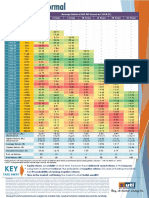

- Sensex Rolling ReturnsDocument1 pageSensex Rolling Returnsmaheshtech76Pas encore d'évaluation

- Sri Lanka Mutual Fund Market Opportunity Outlook 2022Document7 pagesSri Lanka Mutual Fund Market Opportunity Outlook 2022Neeraj ChawlaPas encore d'évaluation

- Cyclic Arbitrage in Decentralized Exchange MarketsDocument29 pagesCyclic Arbitrage in Decentralized Exchange Marketscat220minecraftPas encore d'évaluation

- University of Luzon College of AccountancyDocument3 pagesUniversity of Luzon College of AccountancyJonalyn May De VeraPas encore d'évaluation

- Index of ContentsDocument1 pageIndex of ContentskrutibhattPas encore d'évaluation

- Analysis of Financial Statements: Chapter No.07Document56 pagesAnalysis of Financial Statements: Chapter No.07Blue StonePas encore d'évaluation