Vous aimerez peut-être aussi

- Forklift Truck Risk AssessmentDocument2 pagesForklift Truck Risk AssessmentAshis Das100% (1)

- Mitchella Partridge Berry Materia Medica HerbsDocument3 pagesMitchella Partridge Berry Materia Medica HerbsAlejandra GuerreroPas encore d'évaluation

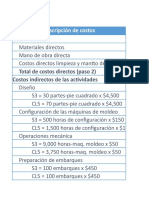

- OPTIMIZED ABC COSTING ANALYSIS TITLEDocument5 pagesOPTIMIZED ABC COSTING ANALYSIS TITLElykaPas encore d'évaluation

- Surgical InstrumentsDocument4 pagesSurgical InstrumentsWafa L. AbdulrahmanPas encore d'évaluation

- PC Assembly PlantDocument19 pagesPC Assembly Plantmuyenzo100% (1)

- G 26 Building Using ETABS 1673077361Document68 pagesG 26 Building Using ETABS 1673077361md hussainPas encore d'évaluation

- An Introduction To Cost Terms and PurposesDocument13 pagesAn Introduction To Cost Terms and PurposesHendriMaulanaPas encore d'évaluation

- BUS 5110 - Written Assignment - Unit 5 - MADocument5 pagesBUS 5110 - Written Assignment - Unit 5 - MAAliyazahra Kamila100% (1)

- P3 Past Papers Model AnswersDocument211 pagesP3 Past Papers Model AnswersEyad UsamaPas encore d'évaluation

- Symbols For Signalling Circuit DiagramsDocument27 pagesSymbols For Signalling Circuit DiagramsrobievPas encore d'évaluation

- Lab Costeo ABCDocument40 pagesLab Costeo ABCJuan Jose Rodriguez CasalloPas encore d'évaluation

- Induction Hardening - Interpretation of Drawing & Testing PDFDocument4 pagesInduction Hardening - Interpretation of Drawing & Testing PDFrajesh DESHMUKHPas encore d'évaluation

- Montego Bay Community College Variance Analysis WorksheetDocument8 pagesMontego Bay Community College Variance Analysis WorksheetLeigh018Pas encore d'évaluation

- Standard Costing & Variance Analysis - Sample Problems With SolutionsDocument8 pagesStandard Costing & Variance Analysis - Sample Problems With SolutionsMarjorie NepomucenoPas encore d'évaluation

- Celiac DiseaseDocument14 pagesCeliac Diseaseapi-355698448100% (1)

- ADDC Construction QuestionairesDocument19 pagesADDC Construction QuestionairesUsman Arif100% (1)

- Case Study Unit 5Document4 pagesCase Study Unit 5Hilkiah MusPas encore d'évaluation

- AOAC 2012.11 Vitamin DDocument3 pagesAOAC 2012.11 Vitamin DPankaj BudhlakotiPas encore d'évaluation

- Wilson Manufacturing Inc Has Implemented Lean Manufacturing IDocument1 pageWilson Manufacturing Inc Has Implemented Lean Manufacturing IAmit PandeyPas encore d'évaluation

- EXAMINATION: MANAGERIAL ACCOUNTINGDocument9 pagesEXAMINATION: MANAGERIAL ACCOUNTINGHồng Đức TrầnPas encore d'évaluation

- Papaya Partners Variance AnalysisDocument5 pagesPapaya Partners Variance Analysisकुनाल सिंहPas encore d'évaluation

- Section A challengesDocument18 pagesSection A challengesAyesha IqbalPas encore d'évaluation

- Cost Allocation Joint Products and ByproductsDocument8 pagesCost Allocation Joint Products and ByproductsHendriMaulanaPas encore d'évaluation

- 11 Standard CostingDocument30 pages11 Standard CostingLalan JaiswalPas encore d'évaluation

- Prof Rishi ChourasiaDocument18 pagesProf Rishi ChourasiaRishi ChourasiaPas encore d'évaluation

- Chapter 7 PPT Version 2Document61 pagesChapter 7 PPT Version 2islamasifPas encore d'évaluation

- Activity Based CostingDocument21 pagesActivity Based CostingSaket ParasrampuriaPas encore d'évaluation

- Managerial Accounting Final ExamDocument14 pagesManagerial Accounting Final ExamatifPas encore d'évaluation

- 4524 Robby Wangsa Saputra 1601226743 AkuntansiDocument3 pages4524 Robby Wangsa Saputra 1601226743 AkuntansiGatau JdodksjsjPas encore d'évaluation

- Tahmina Ahmed Instructor Cost AccountingDocument19 pagesTahmina Ahmed Instructor Cost Accountingfaraazxbox1Pas encore d'évaluation

- Module 3 - ABC Lecture S23Document26 pagesModule 3 - ABC Lecture S23Prachi YadavPas encore d'évaluation

- Mas Problem ABCDocument3 pagesMas Problem ABCPaul Vincent ConcepcionPas encore d'évaluation

- Cost Behavior Analysis & Variable Costing FormulasDocument7 pagesCost Behavior Analysis & Variable Costing FormulasNaba ZehraPas encore d'évaluation

- Analysing and Managing CostsDocument30 pagesAnalysing and Managing CostsSANG HOANG THANHPas encore d'évaluation

- Assignment CVPDocument4 pagesAssignment CVPKwason TaylorPas encore d'évaluation

- Ch.3 - Test BankDocument10 pagesCh.3 - Test Bankahmedgalalabdalbaath2003Pas encore d'évaluation

- Assignment No.2 206Document5 pagesAssignment No.2 206Halimah SheikhPas encore d'évaluation

- Review Sheet Exam 2Document17 pagesReview Sheet Exam 2photo312100% (1)

- Practice Questions On Direct and Indirect Cost VariancesDocument8 pagesPractice Questions On Direct and Indirect Cost VariancesAishwarya RaoPas encore d'évaluation

- Ma 123Document21 pagesMa 123Dean CraigPas encore d'évaluation

- Assignment2revised1Document5 pagesAssignment2revised1Pankaj KhannaPas encore d'évaluation

- UAS-ACCT6130-cost Accounting-Latihan persiapan-PJJDocument4 pagesUAS-ACCT6130-cost Accounting-Latihan persiapan-PJJOlim BariziPas encore d'évaluation

- Question - Mid Term Parallel Quiz 2324Document4 pagesQuestion - Mid Term Parallel Quiz 2324haikal.abiyu.w41Pas encore d'évaluation

- ADM3346 Assignment 2 Fall 2019 Revised With Typos CorrectdDocument3 pagesADM3346 Assignment 2 Fall 2019 Revised With Typos CorrectdSam FishPas encore d'évaluation

- Tutorial 9 Mock Exam Questions - 2022Document32 pagesTutorial 9 Mock Exam Questions - 2022Nina Selin OZSEKERCIPas encore d'évaluation

- Cima Standard Costing and Variance Analysis Session 1 QuestionsDocument13 pagesCima Standard Costing and Variance Analysis Session 1 QuestionsKiri chrisPas encore d'évaluation

- Management Accounting Information in The New Business EnvironmentDocument31 pagesManagement Accounting Information in The New Business EnvironmentGaluh Boga KuswaraPas encore d'évaluation

- ABC Costing Autumn 19Document15 pagesABC Costing Autumn 19Tory IslamPas encore d'évaluation

- Variable Costing SeatworkDocument5 pagesVariable Costing SeatworkPortgas D. AcePas encore d'évaluation

- Factory Overhead Plantwide and Departmental Rates With ExplanationsDocument2 pagesFactory Overhead Plantwide and Departmental Rates With ExplanationsDane LiongsonPas encore d'évaluation

- AkbiDocument37 pagesAkbiCenxi TVPas encore d'évaluation

- Item To Classify Standard Actual Type of VarianceDocument7 pagesItem To Classify Standard Actual Type of Variancedavid johnsonPas encore d'évaluation

- MGT 636 Chapter 01 ProblemsDocument2 pagesMGT 636 Chapter 01 ProblemsOng Kevin0% (1)

- Week 8 (Unit 7) - Tutorial Solutions: Review QuestionDocument10 pagesWeek 8 (Unit 7) - Tutorial Solutions: Review QuestionSheenam SinghPas encore d'évaluation

- Chapter 10 5eDocument4 pagesChapter 10 5eym5c2324Pas encore d'évaluation

- Final for PDFDocument8 pagesFinal for PDFWaizin KyawPas encore d'évaluation

- Problem-1 (Materials, Labor and Variable Overhead Variances)Document3 pagesProblem-1 (Materials, Labor and Variable Overhead Variances)Khim RamosPas encore d'évaluation

- B01 AbcDocument21 pagesB01 AbcAcca BooksPas encore d'évaluation

- Dela Pena-Act102-K7 Ass4Document12 pagesDela Pena-Act102-K7 Ass4Danielle Nicole Crisostomo BrocoyPas encore d'évaluation

- UntitledDocument2 pagesUntitledADEKE MERCYPas encore d'évaluation

- I. Background Information: A. Packaging The ProductsDocument3 pagesI. Background Information: A. Packaging The ProductsVALERIE Y. DIZONPas encore d'évaluation

- Individual assignment (Fall 2023)2Document11 pagesIndividual assignment (Fall 2023)2RealGenius (Carl)Pas encore d'évaluation

- CHAPTER 3 - Limiting Factor AnalysisDocument16 pagesCHAPTER 3 - Limiting Factor AnalysisNURUL SYAMIMIPas encore d'évaluation

- Managerial Accounting - Invidual Task 4Document7 pagesManagerial Accounting - Invidual Task 4Alexander CordovaPas encore d'évaluation

- Managerial Accounting JONGAY (AutoRecovered)Document24 pagesManagerial Accounting JONGAY (AutoRecovered)Jhoy AmoscoPas encore d'évaluation

- Module 9 Demonstration ProblemsDocument15 pagesModule 9 Demonstration ProblemsKatherine JoiePas encore d'évaluation

- Short AnswerDocument4 pagesShort AnswerMichiko Kyung-soonPas encore d'évaluation

- Ma Mba07083 Mhatre Bhushan GhanshyamDocument11 pagesMa Mba07083 Mhatre Bhushan GhanshyamsidPas encore d'évaluation

- Papaya Partners Budget Variance AnalysisDocument9 pagesPapaya Partners Budget Variance AnalysisSaka IbrahimPas encore d'évaluation

- Assignment 5Document3 pagesAssignment 5Hilkiah MusPas encore d'évaluation

- Physics SyllabusDocument85 pagesPhysics Syllabusalex demskoyPas encore d'évaluation

- Cars Ger Eu PCDocument157 pagesCars Ger Eu PCsergeyPas encore d'évaluation

- Pentecostal Ecclesiology: Simon K.H. Chan - 978-90-04-39714-9 Via Free AccessDocument156 pagesPentecostal Ecclesiology: Simon K.H. Chan - 978-90-04-39714-9 Via Free AccessStanley JohnsonPas encore d'évaluation

- Fairs in Punjab 2021-22Document9 pagesFairs in Punjab 2021-22Suchintan SinghPas encore d'évaluation

- 19 - Speed, Velocity and Acceleration (Answers)Document4 pages19 - Speed, Velocity and Acceleration (Answers)keyur.gala100% (1)

- Procedure for safely changing LWCV assembly with torques over 30,000 ft-lbsDocument2 pagesProcedure for safely changing LWCV assembly with torques over 30,000 ft-lbsnjava1978Pas encore d'évaluation

- Module 37 Nur 145Document38 pagesModule 37 Nur 145Marga WreathePas encore d'évaluation

- Crimson Holdings Fact Sheet As of April 14Document3 pagesCrimson Holdings Fact Sheet As of April 14WDIV/ClickOnDetroitPas encore d'évaluation

- Art-App-Module-12 Soulmaking, Improvisation, Installation, & TranscreationDocument4 pagesArt-App-Module-12 Soulmaking, Improvisation, Installation, & TranscreationJohn Mark D. RoaPas encore d'évaluation

- Standardization Parameters For Production of Tofu Using WSD-Y-1 MachineDocument6 pagesStandardization Parameters For Production of Tofu Using WSD-Y-1 MachineAdjengIkaWulandariPas encore d'évaluation

- EiaDocument14 pagesEiaRamir FamorcanPas encore d'évaluation

- Takara 2012Document57 pagesTakara 2012Deepak Ranjan SahooPas encore d'évaluation

- L C R Circuit Series and Parallel1Document6 pagesL C R Circuit Series and Parallel1krishcvrPas encore d'évaluation

- 60 GHZDocument9 pages60 GHZjackofmanytradesPas encore d'évaluation

- Is Revalida ExamDocument11 pagesIs Revalida ExamRodriguez, Jhe-ann M.Pas encore d'évaluation

- Navmesh Plus: How ToDocument7 pagesNavmesh Plus: How TobladimirPas encore d'évaluation

- Philip Rance EAH Philo of ByzantiumDocument3 pagesPhilip Rance EAH Philo of ByzantiumstoliPas encore d'évaluation

- 2 - Alaska - WorksheetsDocument7 pages2 - Alaska - WorksheetsTamni MajmuniPas encore d'évaluation