Vous aimerez peut-être aussi

- Thomson Arthur - Crafting and Executing Strategy - Concepts and CasesDocument569 pagesThomson Arthur - Crafting and Executing Strategy - Concepts and CasesAlex Leț83% (24)

- Financial Statement Analysis, 10e by K. R. Subramanyam & John J. Wild Chapter03Document40 pagesFinancial Statement Analysis, 10e by K. R. Subramanyam & John J. Wild Chapter03RidhoVerianPas encore d'évaluation

- Pak Mulyadi Balanced ScorecardDocument113 pagesPak Mulyadi Balanced ScorecardRidhoVerian100% (2)

- Case PMDocument17 pagesCase PMKowshik SPas encore d'évaluation

- Honey QuestionnaireDocument8 pagesHoney QuestionnaireBerihu GirmayPas encore d'évaluation

- Why The Study of Business Is So ImportantDocument3 pagesWhy The Study of Business Is So ImportantAnita KhanPas encore d'évaluation

- Critical Review of The Globalization of MarketsDocument6 pagesCritical Review of The Globalization of Marketsabrahamsamuel100% (4)

- Environmental Scanning (Chapter2)Document28 pagesEnvironmental Scanning (Chapter2)Maria GanotPas encore d'évaluation

- Enron Corporation and Andersen, LLP CaseDocument13 pagesEnron Corporation and Andersen, LLP CaseCorneliusPas encore d'évaluation

- Note Receivable Part 2Document7 pagesNote Receivable Part 2Carlo VillanPas encore d'évaluation

- Internship Project Report" OnDocument60 pagesInternship Project Report" OnDiksha Sawhney80% (5)

- CHAPTER 7 Bonds and Their ValuationDocument43 pagesCHAPTER 7 Bonds and Their ValuationAhsan100% (2)

- Multi-Generational GapDocument2 pagesMulti-Generational GapPooja NagPas encore d'évaluation

- Stocks and Their Valuation Lecture 2015Document58 pagesStocks and Their Valuation Lecture 2015AJ100% (1)

- Learning-Organization-And-Knowledge-Management-In-The-Public-Sector-Case-Study - Content File PDFDocument17 pagesLearning-Organization-And-Knowledge-Management-In-The-Public-Sector-Case-Study - Content File PDFMuhammad Anwarul Izzat100% (1)

- AD The Globalization of Markets by Theodore Levitt ExplainsDocument3 pagesAD The Globalization of Markets by Theodore Levitt ExplainsKamana Thp Mgr100% (1)

- Human Resource Management Practice in Microsoft CorporationDocument6 pagesHuman Resource Management Practice in Microsoft CorporationMahak SharmaPas encore d'évaluation

- Stocks and Their ValuationDocument48 pagesStocks and Their ValuationHafiz Abdullah Indhar100% (1)

- Learning OrgDocument18 pagesLearning OrgSayali DiwatePas encore d'évaluation

- Risk and Return Concepts PDFDocument3 pagesRisk and Return Concepts PDFyvonneberdosPas encore d'évaluation

- AdffeegghgreggDocument463 pagesAdffeegghgreggSharmaine SurPas encore d'évaluation

- International Marketing Proposal of Bangladeshi HandicraftsDocument11 pagesInternational Marketing Proposal of Bangladeshi Handicraftsacidreign100% (4)

- Trends in Consulting IndustryDocument5 pagesTrends in Consulting IndustryArpit KothariPas encore d'évaluation

- A MultiGenerational WorkforceDocument6 pagesA MultiGenerational WorkforceMiguel GarcíaPas encore d'évaluation

- Relationships Sample QuestionnaireDocument7 pagesRelationships Sample QuestionnaireUsman AhmedPas encore d'évaluation

- RRLDocument3 pagesRRLirohnman hugoPas encore d'évaluation

- Chapter 6Document5 pagesChapter 6Silvia ReginaPas encore d'évaluation

- Begun and Held in Metro Manila, On Monday, The Twenty-Seventh Day of July, Two Thousand FifteenDocument2 pagesBegun and Held in Metro Manila, On Monday, The Twenty-Seventh Day of July, Two Thousand FifteenJay SuarezPas encore d'évaluation

- Regression-Timeseries ForecastingDocument4 pagesRegression-Timeseries ForecastingAkshat TiwariPas encore d'évaluation

- Ch02ppsolutions PDFDocument8 pagesCh02ppsolutions PDFVarsha BhootraPas encore d'évaluation

- Stocks and Their ValuationDocument20 pagesStocks and Their ValuationRajiv LamichhanePas encore d'évaluation

- Employee TurnoverDocument13 pagesEmployee TurnoverDurga TejaPas encore d'évaluation

- Impact of Non Financial Rewards On Employee Attitude Performance in The Workplace A Case Study of Business Institutes of KarachiDocument6 pagesImpact of Non Financial Rewards On Employee Attitude Performance in The Workplace A Case Study of Business Institutes of KarachiFahad BataviaPas encore d'évaluation

- 4) Sameer Vs CabilesDocument3 pages4) Sameer Vs CabilesCatherineBragaisPantiPas encore d'évaluation

- 14 .Labor Et Al Vs NLRC and Gold City Commercial Complex, Inc., GR 110388, Sept 14, 1995Document10 pages14 .Labor Et Al Vs NLRC and Gold City Commercial Complex, Inc., GR 110388, Sept 14, 1995Perry YapPas encore d'évaluation

- Does Intrinsic Rewards and Extrinsic Reward System Matter For Employee Performance? Evidence Form IT Sector of PakistanDocument4 pagesDoes Intrinsic Rewards and Extrinsic Reward System Matter For Employee Performance? Evidence Form IT Sector of PakistanWARSE JournalsPas encore d'évaluation

- Nature of IHRMDocument18 pagesNature of IHRMmishuhappyguyPas encore d'évaluation

- Time Value of MoneyDocument38 pagesTime Value of Moneytomikovan110% (1)

- Stocks and Their ValuationDocument38 pagesStocks and Their ValuationJansen Uy100% (1)

- Learning Organisation MbaDocument9 pagesLearning Organisation MbaMamilla Babu100% (1)

- 4 Competencies of A Learning OrganisationDocument3 pages4 Competencies of A Learning Organisationsrimant kumar100% (1)

- Ethical Issue in BusinessDocument6 pagesEthical Issue in BusinessJudil BanastaoPas encore d'évaluation

- Ford SWOT Analysis 2013Document3 pagesFord SWOT Analysis 2013Vilgia DelarhozaPas encore d'évaluation

- 6 CorporateDocument16 pages6 CorporateMoriko Mayhon100% (2)

- Learning Organization PDFDocument10 pagesLearning Organization PDFBrandon GomezPas encore d'évaluation

- The Globalization of Markets PPT FinalDocument9 pagesThe Globalization of Markets PPT FinalamauryvcPas encore d'évaluation

- The End of The Bretton Woods SystemDocument2 pagesThe End of The Bretton Woods SystemSteffie CarvalhoPas encore d'évaluation

- Public Sector EthicsDocument15 pagesPublic Sector EthicsJones Lyndon Crumb DamoPas encore d'évaluation

- Behavioral Biases-IIDocument49 pagesBehavioral Biases-IIrajeshchintamaneniPas encore d'évaluation

- Employee Turnover in Hospitality IndustryDocument31 pagesEmployee Turnover in Hospitality IndustryJuna BeqiriPas encore d'évaluation

- Letter of SubmissionDocument18 pagesLetter of Submissionshafiat0101Pas encore d'évaluation

- Performance Appraisal & Reward SystemDocument23 pagesPerformance Appraisal & Reward SystemSiddhu VemuriPas encore d'évaluation

- Ba250 Management Science Example ProblemsDocument8 pagesBa250 Management Science Example ProblemsAvlean Rica TorralbaPas encore d'évaluation

- The Learning Organisation OBDocument58 pagesThe Learning Organisation OBKaylen Kim JafthaPas encore d'évaluation

- Recruitment and SelectionDocument30 pagesRecruitment and SelectionSmriti KhannaPas encore d'évaluation

- Research Paper - Low Salary and ContractualizationDocument16 pagesResearch Paper - Low Salary and ContractualizationTrisha Marie PillenaPas encore d'évaluation

- Determinants of Employee Retention in Telecom Sector of Pakistan (Madiha Shoaib)Document18 pagesDeterminants of Employee Retention in Telecom Sector of Pakistan (Madiha Shoaib)Gaurav Sharma100% (1)

- Work Environment SurveyDocument3 pagesWork Environment SurveyScribdTranslations100% (1)

- Unit 1 International Human Resource Management (Human Resource Management)Document53 pagesUnit 1 International Human Resource Management (Human Resource Management)rameshPas encore d'évaluation

- Regression ModelsDocument26 pagesRegression Modelssbc100% (2)

- A Report On Religious Discrimination in The Workplace 3Document3 pagesA Report On Religious Discrimination in The Workplace 3owaxy23Pas encore d'évaluation

- Review This Article PDFDocument27 pagesReview This Article PDFHaliza SaniPas encore d'évaluation

- Thesis Accounts PayableDocument2 pagesThesis Accounts PayableMarife Arellano AlcobendasPas encore d'évaluation

- Stevenson6ce PPT Ch01Document36 pagesStevenson6ce PPT Ch01manpreetPas encore d'évaluation

- CH 9 Bond and Their ValuationDocument40 pagesCH 9 Bond and Their ValuationNeneng WulandariPas encore d'évaluation

- Bonds and Their ValuationDocument50 pagesBonds and Their ValuationhumaidjafriPas encore d'évaluation

- Atpk LK AuditedDocument64 pagesAtpk LK AuditedRidhoVerianPas encore d'évaluation

- Duska Ethics TheoryDocument10 pagesDuska Ethics TheoryRidhoVerianPas encore d'évaluation

- CH 12 Cash Flow Estimatision and Risk AnalysisDocument39 pagesCH 12 Cash Flow Estimatision and Risk AnalysisRidhoVerianPas encore d'évaluation

- Corporate Finance: Derivatives and Hedging RiskDocument55 pagesCorporate Finance: Derivatives and Hedging RiskRidhoVerian100% (1)

- Pak Taufikur CH 11 Financial Management BrighamDocument69 pagesPak Taufikur CH 11 Financial Management BrighamRidhoVerianPas encore d'évaluation

- AM PPA Customer ProfitabilityDocument36 pagesAM PPA Customer ProfitabilityRidhoVerianPas encore d'évaluation

- Pak Mulyadi Cascading Company ScorecardDocument102 pagesPak Mulyadi Cascading Company ScorecardRidhoVerian100% (1)

- Pak Ahmad Zaki Incentive Control AMDocument17 pagesPak Ahmad Zaki Incentive Control AMRidhoVerianPas encore d'évaluation

- Akt Man Environmental AccountingDocument44 pagesAkt Man Environmental AccountingRidhoVerianPas encore d'évaluation

- Bab 14 15 Paparan Managment Project IADocument19 pagesBab 14 15 Paparan Managment Project IARidhoVerianPas encore d'évaluation

- Bab 14 15 Paparan Managment Project IADocument19 pagesBab 14 15 Paparan Managment Project IARidhoVerianPas encore d'évaluation

- Case Study Whole Foods Market in 2008Document20 pagesCase Study Whole Foods Market in 2008RidhoVerianPas encore d'évaluation

- Schedule IagoDocument8 pagesSchedule IagoIago MartinsPas encore d'évaluation

- Art.1231-1232 - Bulatao V EstonactocDocument4 pagesArt.1231-1232 - Bulatao V EstonactocApol Pasok GimenezPas encore d'évaluation

- Lebanese Association of Certified Public Accountants - IFRS July Exam 2018Document8 pagesLebanese Association of Certified Public Accountants - IFRS July Exam 2018jad NasserPas encore d'évaluation

- Isc Report1c 1314Document33 pagesIsc Report1c 1314Rajanna JadiPas encore d'évaluation

- Rosalina Ong Go Roberto Street, Estacio Village Butuan City, Agusan Del Norte 8600Document1 pageRosalina Ong Go Roberto Street, Estacio Village Butuan City, Agusan Del Norte 8600rosaliecarpizoPas encore d'évaluation

- M/s Rishabh Creations Sikka Knitting FabDocument1 pageM/s Rishabh Creations Sikka Knitting FabVarun AgarwalPas encore d'évaluation

- Answers To TestsDocument19 pagesAnswers To TestsАнтон ВасильевPas encore d'évaluation

- BAFB3013 Financial ManagementDocument9 pagesBAFB3013 Financial ManagementSarah ShiphrahPas encore d'évaluation

- Function's of Insurance . by Aftab MullaDocument12 pagesFunction's of Insurance . by Aftab MullaImran Khan SharPas encore d'évaluation

- 2011 Audit of CashDocument2 pages2011 Audit of CashPopeye AlexPas encore d'évaluation

- Mutual Funds in India A Comparative Study of Select Public Sector and Private Sector CompaniesDocument13 pagesMutual Funds in India A Comparative Study of Select Public Sector and Private Sector Companiesarcherselevators0% (1)

- National Pension System (NPS) : SR - No ParticularDocument8 pagesNational Pension System (NPS) : SR - No ParticularLalita PhegadePas encore d'évaluation

- Basic Banking ConceptsDocument17 pagesBasic Banking ConceptsVishnuvardhan VishnuPas encore d'évaluation

- Micro Finance and Rural BankingDocument7 pagesMicro Finance and Rural Bankingfarhadcse30Pas encore d'évaluation

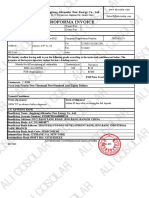

- Alicosolar Proforma Invoice For AS450WDocument1 pageAlicosolar Proforma Invoice For AS450WAngie GuerreroPas encore d'évaluation

- GlTrialBalance - General Ledger Trial Balance ReportDocument4 pagesGlTrialBalance - General Ledger Trial Balance ReportKv kPas encore d'évaluation

- Marine Insurance Claims ProcedureDocument6 pagesMarine Insurance Claims ProcedureNabil MohamedPas encore d'évaluation

- Advanced Accounting-2 Company: HoldingDocument20 pagesAdvanced Accounting-2 Company: HoldingTB AhmedPas encore d'évaluation

- Intermediate AccountingDocument4 pagesIntermediate AccountingMary Ellen LuceñaPas encore d'évaluation

- Financial Statements With Adjustments: Submitted To:-Ms. Palak Bajaj Submitted By:-Chirag VermaDocument15 pagesFinancial Statements With Adjustments: Submitted To:-Ms. Palak Bajaj Submitted By:-Chirag VermaChiragPas encore d'évaluation

- Jawaban Soal No. 1 Jurnal Koreksi A) Sebelum Penutupan BukuDocument13 pagesJawaban Soal No. 1 Jurnal Koreksi A) Sebelum Penutupan BukuAbdurahman YafiePas encore d'évaluation

- Department of Labor: 96 19484Document5 pagesDepartment of Labor: 96 19484USA_DepartmentOfLaborPas encore d'évaluation

- What Does REHABILITATION MeanDocument23 pagesWhat Does REHABILITATION MeanMaLizaCainapPas encore d'évaluation

- SBRIAS40 TutorSlidesDocument10 pagesSBRIAS40 TutorSlidesDipesh MagratiPas encore d'évaluation

- Tan v. Court of Appeals, G.R. No. 108555, December 20, 1994Document11 pagesTan v. Court of Appeals, G.R. No. 108555, December 20, 1994Krister VallentePas encore d'évaluation

- You Paid For It Examines St. Louis Economic Development Partnership's Six-Figure Salaries, High-Priced OfficesDocument8 pagesYou Paid For It Examines St. Louis Economic Development Partnership's Six-Figure Salaries, High-Priced OfficesKevinSeanHeldPas encore d'évaluation

- Merged Banks IFSC and MICRDocument479 pagesMerged Banks IFSC and MICRRahul OjhaPas encore d'évaluation

- Non Performing LoansDocument11 pagesNon Performing LoansRogers256Pas encore d'évaluation