Vous aimerez peut-être aussi

- Chapter 7 Brief ExercisesDocument6 pagesChapter 7 Brief ExercisesPatrick YazbeckPas encore d'évaluation

- The Accounting Cycle - Part1Document12 pagesThe Accounting Cycle - Part1RaaiinaPas encore d'évaluation

- Topic 3 Accounting ProcessDocument49 pagesTopic 3 Accounting ProcessNurul AfiqahPas encore d'évaluation

- ABM 1 - PPT - Chapter 3Document100 pagesABM 1 - PPT - Chapter 3Ofelia RagpaPas encore d'évaluation

- Lecture 1 - Revision - Accrual Accounting ConceptsDocument46 pagesLecture 1 - Revision - Accrual Accounting ConceptsMuzzamil YounusPas encore d'évaluation

- Gross Working CapitalDocument14 pagesGross Working Capitalfizza amjadPas encore d'évaluation

- Financial&managerial Accounting - 15e Williamshakabettner Chap 7Document18 pagesFinancial&managerial Accounting - 15e Williamshakabettner Chap 7mzqacePas encore d'évaluation

- Lecture 03Document108 pagesLecture 03Masood AliPas encore d'évaluation

- Business ModelDocument29 pagesBusiness ModelTirsolito SalvadorPas encore d'évaluation

- Accounting Equation and Transaction AnalysisDocument6 pagesAccounting Equation and Transaction AnalysisRR SarkarPas encore d'évaluation

- Power Point Slides - Week 2 (Canvas) - 2Document37 pagesPower Point Slides - Week 2 (Canvas) - 2damini.sharma1221Pas encore d'évaluation

- AccounBM1 - Recording Business TransactionsDocument41 pagesAccounBM1 - Recording Business TransactionsKathlyn LabetaPas encore d'évaluation

- Rules in Debit and CreditDocument17 pagesRules in Debit and CreditWenibet SilvanoPas encore d'évaluation

- Tugas Kelompok Ke-1 Week 3/ Sesi 4: EssayDocument5 pagesTugas Kelompok Ke-1 Week 3/ Sesi 4: Essayadelia zahraPas encore d'évaluation

- Fabm Group 4. Closing EntriesDocument11 pagesFabm Group 4. Closing Entriesjoel phillip GranadaPas encore d'évaluation

- BAB 2 Analisis TransaksiDocument84 pagesBAB 2 Analisis TransaksiScouter SejatiPas encore d'évaluation

- Ch07Part1 Online PDFDocument39 pagesCh07Part1 Online PDFBich VietPas encore d'évaluation

- Journalizing, Posting and Trial Balance: For Non-WiredDocument8 pagesJournalizing, Posting and Trial Balance: For Non-WiredCj ArquisolaPas encore d'évaluation

- Bookkeeping NCIII Lecture 3.1Document59 pagesBookkeeping NCIII Lecture 3.1jvtg994Pas encore d'évaluation

- Accountancy: Shaheen Falcons Pu CollegeDocument13 pagesAccountancy: Shaheen Falcons Pu CollegeMohammed RayyanPas encore d'évaluation

- Pembahasan Soal AC Part 1Document34 pagesPembahasan Soal AC Part 1suci monalia putriPas encore d'évaluation

- Checkbook RegisterDocument11 pagesCheckbook RegisterDewa WijaksanaPas encore d'évaluation

- T Ran Sak Sijo U RN Alp O Stin G T Rial B Alan Ce A D Ju Stin G E N Tries A D Ju Sted Trial B Alan Cef in An Cial Statem en TC Lo Sin GDocument5 pagesT Ran Sak Sijo U RN Alp O Stin G T Rial B Alan Ce A D Ju Stin G E N Tries A D Ju Sted Trial B Alan Cef in An Cial Statem en TC Lo Sin GAnggelia TiyantiPas encore d'évaluation

- Accounting Concepts and PrinciplesDocument30 pagesAccounting Concepts and PrinciplesKristine Lei Del MundoPas encore d'évaluation

- Accounting For Receivables: Learning ObjectivesDocument63 pagesAccounting For Receivables: Learning ObjectivesBayaderPas encore d'évaluation

- CH 9 - Intermediate AccountingDocument28 pagesCH 9 - Intermediate Accountinghana osmanPas encore d'évaluation

- CH 09Document30 pagesCH 09XS3 GamingPas encore d'évaluation

- Module 5 Answer KeysDocument5 pagesModule 5 Answer KeysJaspreetPas encore d'évaluation

- SOAL AkuntansiDocument13 pagesSOAL AkuntansiArum MashitoPas encore d'évaluation

- Fundamental Accounting Principles By: Wild Larson ChiappettaDocument25 pagesFundamental Accounting Principles By: Wild Larson ChiappettaMuseera IffatPas encore d'évaluation

- Analyzing and Recording TransactionsDocument43 pagesAnalyzing and Recording TransactionsAndrea ValdezPas encore d'évaluation

- 2nd Summative TestDocument2 pages2nd Summative Testje-ann montejoPas encore d'évaluation

- Principles of Accounting Second Year, Semester 1Document38 pagesPrinciples of Accounting Second Year, Semester 1Sara Abdelrahim MakkawiPas encore d'évaluation

- Chapter 7 SolutionsDocument8 pagesChapter 7 SolutionsAustin LeePas encore d'évaluation

- S06-07 - FA - Handout Before 1 - Cash Flow StatementDocument36 pagesS06-07 - FA - Handout Before 1 - Cash Flow Statementcharlesdegaulle594Pas encore d'évaluation

- Chapter 2 AccountingDocument12 pagesChapter 2 Accountingmoon loverPas encore d'évaluation

- Service Entity Module - Key To CorrectionDocument23 pagesService Entity Module - Key To CorrectionMiru YuPas encore d'évaluation

- The Recording Process: Weygandt - Kieso - KimmelDocument68 pagesThe Recording Process: Weygandt - Kieso - Kimmelatia fariaPas encore d'évaluation

- CH 6 Classpack With SolutionsDocument20 pagesCH 6 Classpack With SolutionsjimenaPas encore d'évaluation

- AP 01 - Cash To Accrual BasisDocument11 pagesAP 01 - Cash To Accrual BasisGabriel OrolfoPas encore d'évaluation

- Professional Accounting PackageDocument72 pagesProfessional Accounting PackageAnmol poudelPas encore d'évaluation

- CH 09Document67 pagesCH 09KHANH Du NgocPas encore d'évaluation

- Principles of Accounting Second Year, Semester 1: Transactions AnalysisDocument38 pagesPrinciples of Accounting Second Year, Semester 1: Transactions AnalysisSara Abdelrahim MakkawiPas encore d'évaluation

- Week 12 Homework - Financial AccountingDocument3 pagesWeek 12 Homework - Financial Accountinglamvolamvo0912Pas encore d'évaluation

- SM ch04Document53 pagesSM ch04Akash JainPas encore d'évaluation

- Accounting 471: Class 11Document66 pagesAccounting 471: Class 11CORES LYRICSPas encore d'évaluation

- CH 09Document69 pagesCH 09Jubaida Naznin Chowdhury JefrinPas encore d'évaluation

- Accounting Equations PaDocument24 pagesAccounting Equations PaAisyah Ayu SaputriPas encore d'évaluation

- Fundamentals of Accounting 2 Draft PDFDocument123 pagesFundamentals of Accounting 2 Draft PDFCzaeshel Edades100% (5)

- Acctg 115 - CH 7 SolutionsDocument9 pagesAcctg 115 - CH 7 SolutionsShehryaar MunirPas encore d'évaluation

- Chapter02 AccountingDocument36 pagesChapter02 Accountingkenshi ihsnekPas encore d'évaluation

- Docx. Journal SampleDocument21 pagesDocx. Journal SampleRHIAN B.Pas encore d'évaluation

- Financial Accounting & Analysis AssignmentDocument4 pagesFinancial Accounting & Analysis AssignmentDhanshree Thorat AmbavlePas encore d'évaluation

- Advanced Accounting Week 4Document3 pagesAdvanced Accounting Week 4rahmaPas encore d'évaluation

- Chapter 2 Recording ProcessDocument71 pagesChapter 2 Recording ProcessNaaPas encore d'évaluation

- Fundamentals of ABM1 - Q4 - LAS2 DRAFTDocument10 pagesFundamentals of ABM1 - Q4 - LAS2 DRAFTSitti Halima Amilbahar AdgesPas encore d'évaluation

- Accounting Lecture 1Document3 pagesAccounting Lecture 1Karl haddadPas encore d'évaluation

- Principles of Accounting Lecture 3Document30 pagesPrinciples of Accounting Lecture 3Masum HossainPas encore d'évaluation

- Summary of Richard A. Lambert's Financial Literacy for ManagersD'EverandSummary of Richard A. Lambert's Financial Literacy for ManagersPas encore d'évaluation

- UAE Government Behavorial Competency FrameworkDocument54 pagesUAE Government Behavorial Competency FrameworkRoger Eli PaulPas encore d'évaluation

- UAE Government Behavorial Competency FrameworkDocument54 pagesUAE Government Behavorial Competency FrameworkRoger Eli PaulPas encore d'évaluation

- UAE Government Behavorial Competency FrameworkDocument54 pagesUAE Government Behavorial Competency FrameworkRoger Eli PaulPas encore d'évaluation

- UAE Government Behavorial Competency FrameworkDocument54 pagesUAE Government Behavorial Competency FrameworkRoger Eli PaulPas encore d'évaluation

- Critical Incident Technique: Training WorkbookDocument13 pagesCritical Incident Technique: Training Workbookbishan123Pas encore d'évaluation

- Evaluation of Job Analysis Methods by Experienced Job AnalystsDocument12 pagesEvaluation of Job Analysis Methods by Experienced Job Analystsbishan123Pas encore d'évaluation

- Critical Incident Technique: Training WorkbookDocument13 pagesCritical Incident Technique: Training Workbookbishan123Pas encore d'évaluation

- C&B Webiner ScreenshotDocument4 pagesC&B Webiner Screenshotbishan123Pas encore d'évaluation

- Whitepaper Mofu Perform Compensation BenchmarkingDocument10 pagesWhitepaper Mofu Perform Compensation BenchmarkingbatterupPas encore d'évaluation

- Job EvaluationDocument221 pagesJob Evaluationhutsup100% (1)

- Saraswati Puja Paddhati by Cyber GrandpaDocument93 pagesSaraswati Puja Paddhati by Cyber GrandpaSankha BhattacharyaPas encore d'évaluation

- 2020-Compensation-Best-Practices-Report - Payscale PDFDocument58 pages2020-Compensation-Best-Practices-Report - Payscale PDFbishan123Pas encore d'évaluation

- Effective Interviewing TechniquesDocument17 pagesEffective Interviewing Techniquesbishan123Pas encore d'évaluation

- Effective Interviewing TechniquesDocument17 pagesEffective Interviewing Techniquesbishan123Pas encore d'évaluation

- Employee Satisfaction Survey-1 PDFDocument14 pagesEmployee Satisfaction Survey-1 PDFJohari Valiao AliPas encore d'évaluation

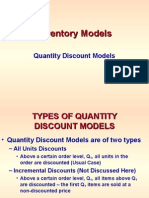

- INVENTORY - Quantity Discount ModelsDocument17 pagesINVENTORY - Quantity Discount ModelsSumit PareekPas encore d'évaluation

- ConclusionDocument2 pagesConclusionYuhanis YusofPas encore d'évaluation

- Midterm Ans GE1202Document3 pagesMidterm Ans GE1202Joshua MahPas encore d'évaluation

- Chap 4 - Bond MarketsDocument19 pagesChap 4 - Bond MarketsMariam JahanzebPas encore d'évaluation

- BCG MatrixDocument19 pagesBCG MatrixRahul Kumar Sahu100% (1)

- Service Marketing ProjectDocument8 pagesService Marketing ProjectRoyal WarjriPas encore d'évaluation

- Business English: Prof. Alis Elena MarinciaDocument10 pagesBusiness English: Prof. Alis Elena MarinciaAlis Elena BUCURPas encore d'évaluation

- Chapter 2 Demand, Supply and Market EquilibriumDocument31 pagesChapter 2 Demand, Supply and Market EquilibriumMuhamad NazrinPas encore d'évaluation

- Analysis & Interpretation: Prepared By: Sir Hamza Abdul HaqDocument10 pagesAnalysis & Interpretation: Prepared By: Sir Hamza Abdul HaqSrabon BaruaPas encore d'évaluation

- Perfect CompetitionDocument3 pagesPerfect CompetitionVarun ChandakPas encore d'évaluation

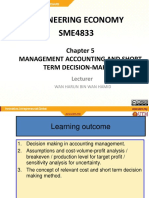

- Engineering Economy SME4833: Management Accounting and Short Term Decision-MakingDocument33 pagesEngineering Economy SME4833: Management Accounting and Short Term Decision-Makinghaza toriqiyPas encore d'évaluation

- Surf Excel & RexonaDocument17 pagesSurf Excel & Rexonaimran_maleque1987100% (3)

- Intro Indian EconomyDocument37 pagesIntro Indian EconomySathish KumarPas encore d'évaluation

- Free QFD Template From QFDPRODocument8 pagesFree QFD Template From QFDPROjimmy FloresPas encore d'évaluation

- Economics - Profit and RevenueDocument23 pagesEconomics - Profit and Revenuejinnah kayPas encore d'évaluation

- Nadia Binti Isnkandar - Digital Marketing Training Module ProposalDocument12 pagesNadia Binti Isnkandar - Digital Marketing Training Module ProposalnadiaPas encore d'évaluation

- Lesson 1Document35 pagesLesson 1Aprile Margareth Hidalgo100% (1)

- MGT602 Technical Article Theme 15Document9 pagesMGT602 Technical Article Theme 15Ishmal RizwanPas encore d'évaluation

- HPDocument23 pagesHPS M Hasan Sayeed100% (5)

- ENGG 405 - Module 6Document7 pagesENGG 405 - Module 6Desi Margaret ElauriaPas encore d'évaluation

- Corporate Other Laws MCQ 2 NewDocument7 pagesCorporate Other Laws MCQ 2 Newgvramani51233Pas encore d'évaluation

- 01 Trade With TrendlinesDocument3 pages01 Trade With TrendlinesWinson A. B.Pas encore d'évaluation

- LLP Act 2008 Handwritten NotesDocument24 pagesLLP Act 2008 Handwritten Notes카미 니KaminiPas encore d'évaluation

- 5 MarksDocument3 pages5 MarksDharma ProductionsPas encore d'évaluation

- Accounting Cycle Exercises IV PDFDocument47 pagesAccounting Cycle Exercises IV PDFAsimPas encore d'évaluation

- AFM - Answers of IMP QuestionsDocument6 pagesAFM - Answers of IMP QuestionsShiva JohriPas encore d'évaluation

- Books of Original Entry Part 3 (Petty Cash Book)Document10 pagesBooks of Original Entry Part 3 (Petty Cash Book)Paula-Kay Thompson100% (1)

- Comparing NPV and BCRDocument2 pagesComparing NPV and BCRKelvin LunguPas encore d'évaluation

- MODULE 5 - Applied EconomicsDocument5 pagesMODULE 5 - Applied EconomicsAstxilPas encore d'évaluation

- Vuegis AdidasDocument11 pagesVuegis Adidasconquesotortillas59Pas encore d'évaluation