Vous aimerez peut-être aussi

- Boston CreameryDocument11 pagesBoston CreameryJelline Gaza100% (3)

- Boston Creamery CaseDocument9 pagesBoston Creamery Caselion_heart3001100% (1)

- Boston Creamery, Inc.Document18 pagesBoston Creamery, Inc.inneke_pradipta0% (1)

- The Home Depot: QuestionsDocument13 pagesThe Home Depot: Questions凱爾思Pas encore d'évaluation

- Boston Creamery Case StudyDocument3 pagesBoston Creamery Case Studypathak2277Pas encore d'évaluation

- Kirin Case AnalysisDocument20 pagesKirin Case Analysisbhuramac0% (1)

- Vivekananda Suaro IIM KozhikodeDocument13 pagesVivekananda Suaro IIM KozhikodevivekPas encore d'évaluation

- Baldwin Case Analysis - Kanupriya ChaudharyDocument4 pagesBaldwin Case Analysis - Kanupriya ChaudharyKanupriya ChaudharyPas encore d'évaluation

- Group 7 - Excel - Destin BrassDocument9 pagesGroup 7 - Excel - Destin BrassSaumya SahaPas encore d'évaluation

- JHT Case ExcelDocument4 pagesJHT Case Excelanup akashePas encore d'évaluation

- Sun Brewing Case ExhibitsDocument26 pagesSun Brewing Case ExhibitsShshankPas encore d'évaluation

- MANAC-II Assignment: by Abhinav Prusty - B19001 Hari Sankar S - B19018 Soham Ghosh - B19052Document6 pagesMANAC-II Assignment: by Abhinav Prusty - B19001 Hari Sankar S - B19018 Soham Ghosh - B19052harisankar sureshPas encore d'évaluation

- Case ReichardDocument23 pagesCase ReichardDesiSelviaPas encore d'évaluation

- Management AccountingDocument1 pageManagement AccountingMohtasim Bin HabibPas encore d'évaluation

- Case Amara RajaDocument2 pagesCase Amara RajaAnand JohnPas encore d'évaluation

- Cafe Monte BiancoDocument21 pagesCafe Monte BiancoWilliam Torrez OrozcoPas encore d'évaluation

- Beta Management QuestionsDocument1 pageBeta Management QuestionsbjhhjPas encore d'évaluation

- Prestige Telephone Company Case Study Report UneditedDocument13 pagesPrestige Telephone Company Case Study Report UneditedAmor0% (1)

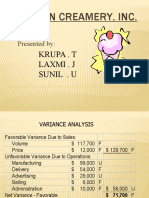

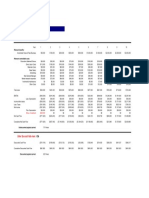

- Boston Creamery Case AnalysisDocument19 pagesBoston Creamery Case AnalysisTessa B. Dick100% (7)

- Mystic SportsDocument34 pagesMystic SportshelloPas encore d'évaluation

- ABC QuestionDocument4 pagesABC QuestionOnaderu Oluwagbenga EnochPas encore d'évaluation

- Alternative Choices and DecisionsDocument29 pagesAlternative Choices and DecisionsAman BansalPas encore d'évaluation

- MANAC II - Morrissey Forgings CaseDocument8 pagesMANAC II - Morrissey Forgings CaseKaran Oberoi100% (1)

- Otago MuseumDocument19 pagesOtago MuseumFoamdomePas encore d'évaluation

- AFM Model Test PaperDocument16 pagesAFM Model Test PaperNeelu AhluwaliaPas encore d'évaluation

- Creative Sports Solution-RevisedDocument4 pagesCreative Sports Solution-RevisedRohit KumarPas encore d'évaluation

- Otago's MuseumDocument5 pagesOtago's Museumyecika50% (2)

- Case Case:: Colorscope, Colorscope, Inc. IncDocument4 pagesCase Case:: Colorscope, Colorscope, Inc. IncBalvinder SinghPas encore d'évaluation

- Super ProjectDocument1 pageSuper ProjectVaibhav SaithPas encore d'évaluation

- Lilac Flour Mills FinalDocument7 pagesLilac Flour Mills FinalAbhishek KujurPas encore d'évaluation

- Baldwin Bicycle CompanyDocument19 pagesBaldwin Bicycle CompanyMannu83Pas encore d'évaluation

- Tata Motors ValuationDocument38 pagesTata Motors ValuationAkshat JainPas encore d'évaluation

- IIMASMPBL0419101-Marketing AssignmentDocument4 pagesIIMASMPBL0419101-Marketing Assignmentsantosh hariharan100% (2)

- Sneaker Excel Sheet For Risk AnalysisDocument11 pagesSneaker Excel Sheet For Risk AnalysisSuperGuyPas encore d'évaluation

- Mercury AthleticDocument9 pagesMercury AthleticfutyPas encore d'évaluation

- Colorscope IncDocument14 pagesColorscope IncShashi ShekharPas encore d'évaluation

- This Study Resource Was: Forner CarpetDocument4 pagesThis Study Resource Was: Forner CarpetLi CarinaPas encore d'évaluation

- Vyaderm-Case Analysis 2006Document4 pagesVyaderm-Case Analysis 2006Mridul SharmaPas encore d'évaluation

- Exhibit 10 (Reliance Baking Soda) : Manufacturer's Price Per CaseDocument2 pagesExhibit 10 (Reliance Baking Soda) : Manufacturer's Price Per Casehope 23Pas encore d'évaluation

- Boston Creamery Case AnalysisDocument19 pagesBoston Creamery Case AnalysisAkshay Agarwal50% (2)

- ABC QuestionsDocument14 pagesABC QuestionsLara Lewis Achilles0% (1)

- Baldwin Bicycle Company - Final Assignment - Group F - 20210728Document4 pagesBaldwin Bicycle Company - Final Assignment - Group F - 20210728ApoorvaPas encore d'évaluation

- Guna Fiber LTDDocument5 pagesGuna Fiber LTDKshitishPas encore d'évaluation

- Piedmont Trailer Manufacturing Comany SolutionsDocument26 pagesPiedmont Trailer Manufacturing Comany SolutionsEve Diekemper100% (1)

- AJAX OriginalDocument7 pagesAJAX Originalreva_radhakrish1834Pas encore d'évaluation

- Accounting in Action: Assignment Classification TableDocument50 pagesAccounting in Action: Assignment Classification TableChi IuvianamoPas encore d'évaluation

- ZomatoDocument56 pagesZomatopreethishPas encore d'évaluation

- ElasticityDocument5 pagesElasticityMike WooddellPas encore d'évaluation

- Frito Lay's PaperDocument9 pagesFrito Lay's Paperpunam89Pas encore d'évaluation

- Lube Study Report - MumbaiDocument11 pagesLube Study Report - Mumbaivinod kumarPas encore d'évaluation

- Boston CreameryDocument11 pagesBoston CreameryNadine OwonoPas encore d'évaluation

- Unit 6 Chapter 11Document5 pagesUnit 6 Chapter 11Kimberly A AlanizPas encore d'évaluation

- Spreadsheet ModellingDocument33 pagesSpreadsheet ModellingSecond FloorPas encore d'évaluation

- Task 7Document14 pagesTask 7Damaris MoralesPas encore d'évaluation

- AISAUCES2Document8 pagesAISAUCES2jlehartPas encore d'évaluation

- Livermore Valley Joint Unified School District: 45-Day Budget RevisionDocument2 pagesLivermore Valley Joint Unified School District: 45-Day Budget RevisionLivermoreParentsPas encore d'évaluation

- Financial Model Template: Company X 31-Mar NZ$Document6 pagesFinancial Model Template: Company X 31-Mar NZ$Bobby ChristiantoPas encore d'évaluation

- Budget PlanDocument10 pagesBudget PlanVasantha Reddy GundetiPas encore d'évaluation

- Group 6 - Boston CreameryDocument7 pagesGroup 6 - Boston CreameryYAKSH DODIAPas encore d'évaluation

- Jaxworks PaybackAnalysis1Document1 pageJaxworks PaybackAnalysis1Jo Ann RangelPas encore d'évaluation

- Portfolio Management - UnileverDocument50 pagesPortfolio Management - UnileverJames Jin-Hong Kim100% (1)

- Ultimate Binary Options e BookDocument45 pagesUltimate Binary Options e BookJayPas encore d'évaluation

- Capital Structure Decision: An Overview: Kennedy Prince ModuguDocument14 pagesCapital Structure Decision: An Overview: Kennedy Prince ModuguChaitanya PrasadPas encore d'évaluation

- The Launch of Ariel by The Procter and Gamble PakistanDocument2 pagesThe Launch of Ariel by The Procter and Gamble PakistanMaxhar Abbax100% (1)

- Parcor 4Document3 pagesParcor 4Joana Mae BalbinPas encore d'évaluation

- Camels Analysis of HDFC BankDocument31 pagesCamels Analysis of HDFC Bankasifbhaiyat33% (3)

- BUS FPX4060 - Assessment1 1Document17 pagesBUS FPX4060 - Assessment1 1AA TsolScholarPas encore d'évaluation

- Comparatie IFRS HGBDocument5 pagesComparatie IFRS HGBValentin BurcaPas encore d'évaluation

- TS Cash FlowDocument4 pagesTS Cash FlowVansh GoelPas encore d'évaluation

- Advertising PitchDocument8 pagesAdvertising PitchririPas encore d'évaluation

- Advance P13-14Document10 pagesAdvance P13-14nadaPas encore d'évaluation

- Frameworks - IIMADocument8 pagesFrameworks - IIMAParth SOODANPas encore d'évaluation

- Cashflow AnalysisDocument19 pagesCashflow Analysisgl101Pas encore d'évaluation

- Major Project - UnschoolDocument3 pagesMajor Project - UnschoolSAYANEE MITRA 21214098Pas encore d'évaluation

- Ma 1128Document21 pagesMa 1128jjim46686Pas encore d'évaluation

- MICFL - Annual Report 2020-21Document175 pagesMICFL - Annual Report 2020-21adittoantur100Pas encore d'évaluation

- UntitledDocument2 pagesUntitledRegir Adil100% (1)

- The Six Month Merchandise PlanDocument6 pagesThe Six Month Merchandise PlanJudy Ann CaubangPas encore d'évaluation

- Conceptual Framework ProcurementDocument218 pagesConceptual Framework ProcurementTerry Gunduza0% (1)

- Facebook Blueprint - Study GuideDocument47 pagesFacebook Blueprint - Study Guidefunguy29100% (4)

- Bsit Performance TaskDocument1 pageBsit Performance Taskaldwin.barba45Pas encore d'évaluation

- 11th - ACCOUNTANCY - PUBLIC EXAM MARCH-2023 ANSWER KEY (EM)Document17 pages11th - ACCOUNTANCY - PUBLIC EXAM MARCH-2023 ANSWER KEY (EM)nishvanprabhuPas encore d'évaluation

- MKT101 - Chapter 9 - TKR PDFDocument32 pagesMKT101 - Chapter 9 - TKR PDFAhnaf RaselPas encore d'évaluation

- College Presentation - Lipton Talent Hunt1Document15 pagesCollege Presentation - Lipton Talent Hunt1mannif1100% (1)

- Introduction To Economics Exercise Chapter TwoDocument5 pagesIntroduction To Economics Exercise Chapter TwoNebiyu NegaPas encore d'évaluation

- Solution Manual For Financial Statements Analysis Subramanyam Wild 11th EditionDocument48 pagesSolution Manual For Financial Statements Analysis Subramanyam Wild 11th EditionKatrinaYoungqtoki100% (83)

- Zakiyyah Logan Joins PrivatePlus MortgageDocument2 pagesZakiyyah Logan Joins PrivatePlus MortgagePR.comPas encore d'évaluation

- E-Retailing Vs Traditional RetailingDocument13 pagesE-Retailing Vs Traditional RetailingGagan Gupta100% (1)

- Introduction To Inventory ManagementDocument71 pagesIntroduction To Inventory ManagementJane LobPas encore d'évaluation

- Case 6Document24 pagesCase 6Bella TjendriawanPas encore d'évaluation