Vous aimerez peut-être aussi

- Music Mart SolutionDocument6 pagesMusic Mart SolutionStranger Sinha50% (2)

- Problem 2-2: J.L. Gregory CompanyDocument5 pagesProblem 2-2: J.L. Gregory CompanyKAPIL MBA 2021-23 (Delhi)Pas encore d'évaluation

- Case 2-2 Music Mart Balance Sheet 1 OctDocument5 pagesCase 2-2 Music Mart Balance Sheet 1 OctAnubhav Jha100% (3)

- 01 Ribbons N' Bows - SolutionDocument4 pages01 Ribbons N' Bows - SolutionShivam Kanojia100% (2)

- Lone Pine Cafe-CaseDocument28 pagesLone Pine Cafe-CaseNadya Rizkita100% (2)

- Case 3.1Document2 pagesCase 3.1Sandeep Agrawal100% (6)

- Case Forest City Tennis ClubDocument9 pagesCase Forest City Tennis ClubAhmedNiaz100% (1)

- Dispensers of CaliforniaDocument4 pagesDispensers of CaliforniaShweta GautamPas encore d'évaluation

- Maynard Company (A & B)Document9 pagesMaynard Company (A & B)akashnathgarg0% (1)

- Maynard CompanyDocument5 pagesMaynard CompanyNikitha Andrea SaldanhaPas encore d'évaluation

- 2-1 Maynard Company (A)Document1 page2-1 Maynard Company (A)Tarry Berry75% (4)

- Lone Pine CafeDocument4 pagesLone Pine CafeRahul TiwariPas encore d'évaluation

- Chapter 3 SolutionsDocument8 pagesChapter 3 SolutionsViren DeshpandePas encore d'évaluation

- Maruti Manesar Lockout: The Flip Side of People Management: Case Study by Group 9Document7 pagesMaruti Manesar Lockout: The Flip Side of People Management: Case Study by Group 9manik singh100% (1)

- Lone Pine Cafe SolutionDocument5 pagesLone Pine Cafe SolutionRitu ChhipaPas encore d'évaluation

- Solman 12 Second EdDocument23 pagesSolman 12 Second Edferozesheriff50% (2)

- Assumptions - : Cash Flow From Operations $ 0Document4 pagesAssumptions - : Cash Flow From Operations $ 0Krish HegdePas encore d'évaluation

- Campus PizzeriaDocument12 pagesCampus PizzeriaSHIVAM SRIVASTAVAPas encore d'évaluation

- Problem 3-1Document2 pagesProblem 3-1Omar CirunayPas encore d'évaluation

- A Bipartisan Agenda For Change: Case ProblemDocument6 pagesA Bipartisan Agenda For Change: Case ProblemunitybPas encore d'évaluation

- Lori Crump Accounting Case StudyDocument1 pageLori Crump Accounting Case StudyHarsh Anchalia100% (1)

- Case Study 4 - 3 Copies ExpressDocument8 pagesCase Study 4 - 3 Copies ExpressJZ0% (1)

- ACCOUNTING STERN CORPORATION (A) AnswerDocument4 pagesACCOUNTING STERN CORPORATION (A) AnswerPradina RachmadiniPas encore d'évaluation

- AHM13e - Chapter 01 - Key To EOC Problems and CasesDocument14 pagesAHM13e - Chapter 01 - Key To EOC Problems and CasesArunesh SN100% (1)

- Maynard Company (A) : EXHIBIT 1 Account BalancesDocument2 pagesMaynard Company (A) : EXHIBIT 1 Account Balancesriya lakhotiaPas encore d'évaluation

- Solution For Lone Pine Cafe CaseDocument5 pagesSolution For Lone Pine Cafe CaseShammika Krishna75% (4)

- Dispensers of California Case AnalysisDocument10 pagesDispensers of California Case AnalysisAvinash Singh100% (1)

- Ramji Bai VasavaDocument9 pagesRamji Bai Vasavaajatc6048100% (1)

- Revenue Recognition at HBPDocument2 pagesRevenue Recognition at HBPtechna8Pas encore d'évaluation

- Making A Tough Personnel Decision at Nova Waterfront HotelDocument11 pagesMaking A Tough Personnel Decision at Nova Waterfront HotelSiddharthPas encore d'évaluation

- Maria Hernandez and AssociatesDocument9 pagesMaria Hernandez and AssociatesMalik Fahad YounasPas encore d'évaluation

- Sombrero - Proposed Fruit Juice Outlet PDFDocument19 pagesSombrero - Proposed Fruit Juice Outlet PDFAngeli Aurelia100% (1)

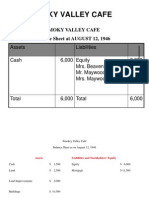

- Smoky Valley CafeDocument3 pagesSmoky Valley Cafemohit_namanPas encore d'évaluation

- Lone Pine CafeDocument13 pagesLone Pine CafeCynthia Anggi Maulina100% (1)

- The Garden Spot 1Document25 pagesThe Garden Spot 1Saad Arain0% (1)

- QED Electronics - Problem 3.7Document1 pageQED Electronics - Problem 3.7ivanyongforexPas encore d'évaluation

- Mansa Building CaseDocument14 pagesMansa Building CaseRikki DasPas encore d'évaluation

- Lewis Corporation Case 6-2 - Group 5Document8 pagesLewis Corporation Case 6-2 - Group 5Om Prakash100% (1)

- Case Report - Grenell FarmDocument5 pagesCase Report - Grenell Farmajsibal100% (1)

- Harsh Electricals Analyzing Cost in Search of Profit-Case StudyDocument8 pagesHarsh Electricals Analyzing Cost in Search of Profit-Case StudyAl- Noor0% (1)

- CPL Case Analysis SolutionDocument5 pagesCPL Case Analysis SolutionInder Singh100% (2)

- Problems & Solutions - RNSDocument28 pagesProblems & Solutions - RNSAyushi0% (1)

- Problem 4-4 Dindorf CompanyDocument5 pagesProblem 4-4 Dindorf Companymelati50% (4)

- Industrial Relations at Asian Paints - ePGPX03 - Group - 9Document13 pagesIndustrial Relations at Asian Paints - ePGPX03 - Group - 9manik singh0% (2)

- Solution Canonical Decision Problem PDFDocument24 pagesSolution Canonical Decision Problem PDFSaadat Ullah KhanPas encore d'évaluation

- Cash Flow CH 11Document2 pagesCash Flow CH 11ayush sharma75% (4)

- Multi Tech Case AnalysisDocument1 pageMulti Tech Case AnalysisRit8Pas encore d'évaluation

- Maria Hernandez Chemalite and Thumbs Up Case Study FinancialsDocument7 pagesMaria Hernandez Chemalite and Thumbs Up Case Study FinancialsTara AkintewePas encore d'évaluation

- Case Baron CoburgDocument8 pagesCase Baron CoburgDarwin Dionisio Clemente100% (2)

- Smokey Valley CafeDocument3 pagesSmokey Valley CafeSreenath SukumaranPas encore d'évaluation

- Lava Case Study Decision Paper KaushalDocument4 pagesLava Case Study Decision Paper Kaushalkaushal dhaparePas encore d'évaluation

- Octane Service StationDocument8 pagesOctane Service StationKalyan Kumar83% (6)

- Hamilton - Case A - 5 PDFDocument2 pagesHamilton - Case A - 5 PDFJayash Kaushal0% (1)

- Cash Flow StatementDocument4 pagesCash Flow StatementRavina Singh100% (1)

- Ch2 Solutions To The ExercisesDocument5 pagesCh2 Solutions To The ExercisesNishant Sharma0% (1)

- Case 4 2Document5 pagesCase 4 2Marjorie Morada67% (3)

- C1 MobonikDocument1 pageC1 MobonikKANIKA GORAYAPas encore d'évaluation

- Case-Final Music MartDocument17 pagesCase-Final Music MartDarwin Dionisio ClementePas encore d'évaluation

- Drill Corporate LiquidationDocument3 pagesDrill Corporate LiquidationElizabeth DumawalPas encore d'évaluation

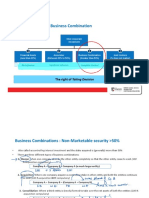

- Complete Control: Business Combination: The Right of Taking DecisionDocument17 pagesComplete Control: Business Combination: The Right of Taking DecisionSaurabh AwatiPas encore d'évaluation

- Garbage CollectionDocument1 pageGarbage CollectionDarwin Dionisio ClementePas encore d'évaluation

- DPWH For Ped LaneDocument2 pagesDPWH For Ped LaneDarwin Dionisio ClementePas encore d'évaluation

- Foundation Day MassDocument1 pageFoundation Day MassDarwin Dionisio ClementePas encore d'évaluation

- Maciprisa Winners For 2009Document1 pageMaciprisa Winners For 2009Darwin Dionisio ClementePas encore d'évaluation

- Epis Le: 1 School NewsDocument31 pagesEpis Le: 1 School NewsDarwin Dionisio ClementePas encore d'évaluation

- Management-The Broken Window TheoryDocument2 pagesManagement-The Broken Window TheoryDarwin Dionisio Clemente100% (1)

- Management-Just in Time TheoryDocument14 pagesManagement-Just in Time TheoryDarwin Dionisio ClementePas encore d'évaluation

- Life-Time For GodDocument61 pagesLife-Time For GodDarwin Dionisio ClementePas encore d'évaluation

- Life-Walk With MeDocument3 pagesLife-Walk With MeDarwin Dionisio ClementePas encore d'évaluation

- Life-What Makes Life 100Document2 pagesLife-What Makes Life 100Darwin Dionisio ClementePas encore d'évaluation

- Life-The Parable of The CrossDocument1 pageLife-The Parable of The CrossDarwin Dionisio Clemente100% (1)

- Life-There Is A Story About Two Friends WalkingDocument2 pagesLife-There Is A Story About Two Friends WalkingDarwin Dionisio ClementePas encore d'évaluation

- Governmental and Nonprofit Accounting 10th Edition Smith Test BankDocument13 pagesGovernmental and Nonprofit Accounting 10th Edition Smith Test Bankjessica100% (20)

- Executives Zero in On PriceDocument4 pagesExecutives Zero in On PriceRachelPas encore d'évaluation

- IGCSE Economics NotesDocument83 pagesIGCSE Economics NoteshiramchurnPas encore d'évaluation

- Chapter 3 - Shopping MallDocument19 pagesChapter 3 - Shopping MallNur Illahi'Pas encore d'évaluation

- Saurabh Surve - Updated ResumeDocument4 pagesSaurabh Surve - Updated ResumeSaurabh SurvePas encore d'évaluation

- Presentation of Merchant BankerDocument20 pagesPresentation of Merchant BankerJatin KambliPas encore d'évaluation

- Changes in Online Purchasing Human BehaviorDocument10 pagesChanges in Online Purchasing Human BehaviorSabrina Tasnim Esha 1721098Pas encore d'évaluation

- Gojek (Gofood Grab (Food) Ovo, Dana, Gopay Lembaga Keuangan - SuplierDocument1 pageGojek (Gofood Grab (Food) Ovo, Dana, Gopay Lembaga Keuangan - SuplierCurve CirclePas encore d'évaluation

- Institute of Management Studies, Davv University Indore: Mba (E-Commerce) 7 SemesterDocument30 pagesInstitute of Management Studies, Davv University Indore: Mba (E-Commerce) 7 SemesterPratiksha BairwaPas encore d'évaluation

- Landing Your Dream JobDocument24 pagesLanding Your Dream Jobnorshafikah0176Pas encore d'évaluation

- 1 Digital EntreprenuershipDocument32 pages1 Digital EntreprenuershipJit MukherheePas encore d'évaluation

- Richport Company Manufactures Products That Often Require SpecifDocument1 pageRichport Company Manufactures Products That Often Require SpecifAmit PandeyPas encore d'évaluation

- Compare and Contrast The Industrial Organisation Approach To The ResourceDocument3 pagesCompare and Contrast The Industrial Organisation Approach To The ResourceMarvin AlleynePas encore d'évaluation

- Financial Management CIA - 1 HERMES DIVYAM 2323626Document14 pagesFinancial Management CIA - 1 HERMES DIVYAM 2323626Divyam AgarwalPas encore d'évaluation

- Môn QU Ản Trị Chiến Lược (Strategic Management) L ớp học phần: Th ời lượng: 75 phútDocument2 pagesMôn QU Ản Trị Chiến Lược (Strategic Management) L ớp học phần: Th ời lượng: 75 phútThanh Hiếu Trần ThịPas encore d'évaluation

- May 2015 1492438683 38Document3 pagesMay 2015 1492438683 38Hồng ThắmPas encore d'évaluation

- Process Strategies: Three Types of Processes 1. Process FocusDocument4 pagesProcess Strategies: Three Types of Processes 1. Process Focusalpha fivePas encore d'évaluation

- Chapter 21 Test BankDocument78 pagesChapter 21 Test BankBrandon LeePas encore d'évaluation

- Selling: The Days of Amateur Selling Are OverDocument4 pagesSelling: The Days of Amateur Selling Are Overazeneth santosPas encore d'évaluation

- Miniso Retail ManagementDocument20 pagesMiniso Retail ManagementAditya100% (1)

- Apple Inc.: Case Study: A Deep Dive Into Apple Inc.'s Cutting Edge Supply Chain StrategiesDocument22 pagesApple Inc.: Case Study: A Deep Dive Into Apple Inc.'s Cutting Edge Supply Chain StrategiessoumikdasPas encore d'évaluation

- Assignment FINM7406Document4 pagesAssignment FINM7406TaufikTaoPas encore d'évaluation

- OlaDocument2 pagesOlaanderspeh.realestatePas encore d'évaluation

- Chapter 4 - Accounting For Merchandising (Slide Notes)Document27 pagesChapter 4 - Accounting For Merchandising (Slide Notes)NUR BALQIS BINTI MOHD TAJUDDIN BGPas encore d'évaluation

- Here Is What I Say To Start A Melaleuca Presentation When Meeting With Someone PDFDocument4 pagesHere Is What I Say To Start A Melaleuca Presentation When Meeting With Someone PDFPat NewtonPas encore d'évaluation

- Test Bank-Auditing Theory Chapter 9Document6 pagesTest Bank-Auditing Theory Chapter 9Michael CarlayPas encore d'évaluation

- P.G.Apte International Financial Management 1Document67 pagesP.G.Apte International Financial Management 1NeenaBediPas encore d'évaluation

- Beneish N Nichols.2005Document60 pagesBeneish N Nichols.2005Shanti PertiwiPas encore d'évaluation

- RP Theisis Group 5 Final (1) - 2Document39 pagesRP Theisis Group 5 Final (1) - 2Muhammad Ahsan SiddiquiPas encore d'évaluation

- Marketing ChannelDocument16 pagesMarketing Channelsakshi tomarPas encore d'évaluation