Vous aimerez peut-être aussi

- Purchase Money MortgageDocument6 pagesPurchase Money MortgageJames Bradley StoddartPas encore d'évaluation

- Final Exam-Law On Obligations and ContractsDocument6 pagesFinal Exam-Law On Obligations and ContractsKat Miranda75% (8)

- More Credit With Fewer Crises 2011Document84 pagesMore Credit With Fewer Crises 2011World Economic ForumPas encore d'évaluation

- Activity Based CostingDocument30 pagesActivity Based Costinghardik1302Pas encore d'évaluation

- HCCDocument272 pagesHCCAlok Singh RajawatPas encore d'évaluation

- Business Finance ManagementDocument14 pagesBusiness Finance ManagementMuhammad Sajid SaeedPas encore d'évaluation

- Valuation and Rates of Return: Powerpoint Presentation Prepared by Michel Paquet, SaitDocument41 pagesValuation and Rates of Return: Powerpoint Presentation Prepared by Michel Paquet, SaitArundhati SinhaPas encore d'évaluation

- Creating Value Through Required ReturnDocument74 pagesCreating Value Through Required Returnriz4winPas encore d'évaluation

- Ias-40 - Investment PropertyDocument16 pagesIas-40 - Investment PropertyPue Das100% (2)

- Chapter 4 DerivativesDocument38 pagesChapter 4 DerivativesTamrat KindePas encore d'évaluation

- Chapter 7 Choosing A Source of Credit The Costs of Credit AlternativesDocument40 pagesChapter 7 Choosing A Source of Credit The Costs of Credit Alternativesgyanprakashdeb302Pas encore d'évaluation

- CVP Analysis Final 1Document92 pagesCVP Analysis Final 1Utsav ChoudhuryPas encore d'évaluation

- Cancellation of Real Estate MortgageDocument2 pagesCancellation of Real Estate MortgageapbacaniPas encore d'évaluation

- Capital StructureDocument41 pagesCapital StructureRAJASHRI SPas encore d'évaluation

- Nature and Definition of AccountingDocument17 pagesNature and Definition of AccountingEdward Magat100% (1)

- Introduction To Corporate FinanceDocument29 pagesIntroduction To Corporate FinanceRifki AyyashPas encore d'évaluation

- Accounts Receivable (Chapter 4)Document31 pagesAccounts Receivable (Chapter 4)chingPas encore d'évaluation

- Taxarion PresentationDocument39 pagesTaxarion PresentationNeri DelfinPas encore d'évaluation

- MA2 T2 MD Cost of CapitalDocument57 pagesMA2 T2 MD Cost of CapitalMangoStarr Aibelle VegasPas encore d'évaluation

- Debt MarketDocument15 pagesDebt MarketChetal BholePas encore d'évaluation

- Financial Management - PPT - 2011Document183 pagesFinancial Management - PPT - 2011ashpika100% (1)

- Equity and Debt: First Some RevisionDocument44 pagesEquity and Debt: First Some RevisionHay JirenyaaPas encore d'évaluation

- Cost of CapitalDocument37 pagesCost of Capitalrajthakre81Pas encore d'évaluation

- Current Liabilities and Contingencies: HapterDocument58 pagesCurrent Liabilities and Contingencies: Haptergellie mare floresPas encore d'évaluation

- Risk and The Required Rate of ReturnDocument31 pagesRisk and The Required Rate of Returngellie villarinPas encore d'évaluation

- Swedish MatchDocument6 pagesSwedish MatchMechanical DepartmentPas encore d'évaluation

- MidTerm Lesson Part 1Document34 pagesMidTerm Lesson Part 1ARMAN WAYNE ANGELESPas encore d'évaluation

- Chap 009Document20 pagesChap 009Ela PelariPas encore d'évaluation

- Financial Management I - Chapter 8Document21 pagesFinancial Management I - Chapter 8Mardi UmarPas encore d'évaluation

- Chap 014Document79 pagesChap 014hanguyenhihiPas encore d'évaluation

- Cost of CapitalDocument18 pagesCost of CapitalJoshua CabinasPas encore d'évaluation

- Risk, Cost of Capital, and ValuationDocument34 pagesRisk, Cost of Capital, and ValuationNguyễn Cẩm HươngPas encore d'évaluation

- Organization and Functioning of Securities MarketsDocument36 pagesOrganization and Functioning of Securities MarketsabidanazirPas encore d'évaluation

- Chapter 2 - The Business Plan Road Map To SuccessDocument52 pagesChapter 2 - The Business Plan Road Map To SuccessFanie SaphiraPas encore d'évaluation

- Cost of Capital: Powerpoint Presentation Prepared by Michel Paquet, SaitDocument54 pagesCost of Capital: Powerpoint Presentation Prepared by Michel Paquet, SaitArundhati SinhaPas encore d'évaluation

- Substantive Test of CashDocument16 pagesSubstantive Test of CashmanuelaristotlePas encore d'évaluation

- Long Term Notes PayableDocument11 pagesLong Term Notes PayableMuhammad Zikri ErnansyaPas encore d'évaluation

- Cost of CapitalDocument53 pagesCost of CapitalJaodat Mand KhanPas encore d'évaluation

- AccountDocument37 pagesAccountGaurang MakwanaPas encore d'évaluation

- Company Accounting - Powerpoint PresentationDocument29 pagesCompany Accounting - Powerpoint Presentationtammy_yau3199100% (1)

- Cost of CapitalDocument21 pagesCost of Capitalshan07011984Pas encore d'évaluation

- The Capital Structure TheoriesDocument61 pagesThe Capital Structure TheoriesAayushPas encore d'évaluation

- Cost of Capital Capital BudgetingDocument19 pagesCost of Capital Capital BudgetingFahad AliPas encore d'évaluation

- Accounting For Long Term Construction ContractsDocument25 pagesAccounting For Long Term Construction Contractspearl100% (1)

- FM11 CH 09 Cost of CapitalDocument54 pagesFM11 CH 09 Cost of CapitalMadeOasePas encore d'évaluation

- Liablities Provision and Contingences Suger FactoryDocument49 pagesLiablities Provision and Contingences Suger FactorynatiPas encore d'évaluation

- Capital Structure Determination Capital Structure DeterminationDocument43 pagesCapital Structure Determination Capital Structure Determinationzohrah riazPas encore d'évaluation

- Current LiabilitiesDocument111 pagesCurrent LiabilitiesMikaela LacabaPas encore d'évaluation

- Chapter Three: Valuation of Financial Instruments & Cost of CapitalDocument68 pagesChapter Three: Valuation of Financial Instruments & Cost of CapitalAbrahamPas encore d'évaluation

- Intro. To Income Tax FTDocument52 pagesIntro. To Income Tax FTJOANA GRACE ALLORINPas encore d'évaluation

- Sources and Raising of LT FinanceDocument52 pagesSources and Raising of LT FinanceAshutoshPas encore d'évaluation

- CH 09 RevisedDocument36 pagesCH 09 RevisedNiharikaChouhanPas encore d'évaluation

- Relative Valuations FINALDocument44 pagesRelative Valuations FINALChinmay ShirsatPas encore d'évaluation

- Tax For CorpDocument28 pagesTax For CorpNiki DimaanoPas encore d'évaluation

- Cost of Capital: Foundations of Financial ManagementDocument41 pagesCost of Capital: Foundations of Financial ManagementBlack UnicornPas encore d'évaluation

- Corporate Income Taxation-Special CorporationDocument24 pagesCorporate Income Taxation-Special CorporationXyla Marie EstorPas encore d'évaluation

- Terminal Cash FlowDocument9 pagesTerminal Cash FlowKazzandraEngallaPaduaPas encore d'évaluation

- Accounting BasicsDocument68 pagesAccounting BasicsEd Caty100% (1)

- Corporate Finance Chapter6Document20 pagesCorporate Finance Chapter6Dan688Pas encore d'évaluation

- ch10 - LiabilitiesDocument89 pagesch10 - Liabilitiessherlyne100% (1)

- Chapter 4 PowerpointDocument25 pagesChapter 4 Powerpointapi-248607804Pas encore d'évaluation

- Lec7 - Account ReceivablesDocument33 pagesLec7 - Account ReceivablesDylan Rabin PereiraPas encore d'évaluation

- Investment in Debt SecuritiesDocument53 pagesInvestment in Debt SecuritiesLalaine De JesusPas encore d'évaluation

- Cap BudDocument29 pagesCap BudJorelyn Joy Balbaloza CandoyPas encore d'évaluation

- Chap 012Document15 pagesChap 012Ela PelariPas encore d'évaluation

- Cost of CapitalDocument68 pagesCost of CapitalJohn Ervin TalagaPas encore d'évaluation

- Report Chapter 10Document39 pagesReport Chapter 10Erma CaseñasPas encore d'évaluation

- Valuation of Accounts ReceivableDocument7 pagesValuation of Accounts ReceivableUwuuUPas encore d'évaluation

- 8 OptionsDocument37 pages8 Optionskrishnadasa108Pas encore d'évaluation

- Operations Management FoundationsDocument72 pagesOperations Management FoundationsKabariPas encore d'évaluation

- Working Capital Management: (Training Seminars)Document1 pageWorking Capital Management: (Training Seminars)VenoniPas encore d'évaluation

- 8 OptionsDocument37 pages8 Optionskrishnadasa108Pas encore d'évaluation

- Receivable ManagementDocument49 pagesReceivable Managementrekha123Pas encore d'évaluation

- 8 OptionsDocument37 pages8 Optionskrishnadasa108Pas encore d'évaluation

- Credit Risk Management Research PapersDocument6 pagesCredit Risk Management Research Papersscxofyplg100% (1)

- Topic 5c - Audit of Shareholders' Equity and Long Term LiabilityDocument14 pagesTopic 5c - Audit of Shareholders' Equity and Long Term LiabilityLANGITBIRUPas encore d'évaluation

- MB0041Document26 pagesMB0041Saurav KumarPas encore d'évaluation

- This Study Resource WasDocument2 pagesThis Study Resource WasNah HamzaPas encore d'évaluation

- 8 Mata v. Court of Appeals (April 7, 1992)Document8 pages8 Mata v. Court of Appeals (April 7, 1992)pkdg1995Pas encore d'évaluation

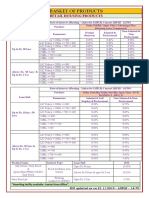

- BASKET OF PRODUCTS As On 21.11.19Document3 pagesBASKET OF PRODUCTS As On 21.11.19Virendra K VermaPas encore d'évaluation

- Resume of KarencoslinDocument3 pagesResume of Karencoslinapi-24131152Pas encore d'évaluation

- FMDFINA Valuation Online HandoutsDocument12 pagesFMDFINA Valuation Online HandoutsasiacrisostomoPas encore d'évaluation

- Overview of CreditDocument24 pagesOverview of CreditJanell AgananPas encore d'évaluation

- CFA Research Challenge Write-UpDocument15 pagesCFA Research Challenge Write-UpSebastian MorenoPas encore d'évaluation

- Compound InterestDocument29 pagesCompound InterestNicole Roxanne RubioPas encore d'évaluation

- Develop and Use A Savings Plan MaterialDocument9 pagesDevelop and Use A Savings Plan MaterialDo DothingsPas encore d'évaluation

- Alfred C. Morley-The Financial Services Industry - Banks, Thrifts, Insurance Companies, and Securities Firms-AIMR (CFA Institute) (1992) PDFDocument148 pagesAlfred C. Morley-The Financial Services Industry - Banks, Thrifts, Insurance Companies, and Securities Firms-AIMR (CFA Institute) (1992) PDFtariqul21Pas encore d'évaluation

- Muskan Valbani PGP/24/456Document6 pagesMuskan Valbani PGP/24/456Muskan ValbaniPas encore d'évaluation

- Accounting Principles AbDocument36 pagesAccounting Principles Absamson mutukuPas encore d'évaluation

- Tullett Prebon Perfect Storm. Energi Finance and The End of GrowDocument84 pagesTullett Prebon Perfect Storm. Energi Finance and The End of GrowasdgsdfgPas encore d'évaluation

- Retail Banking AdvancesDocument38 pagesRetail Banking AdvancesShruti SrivastavaPas encore d'évaluation

- Innovaglobal-003 040119Document37 pagesInnovaglobal-003 040119georgepPas encore d'évaluation

- MathDocument35 pagesMathbritaniaPas encore d'évaluation

- Chapter 07: Bond Markets: Page 1Document23 pagesChapter 07: Bond Markets: Page 1AS SAPas encore d'évaluation

- Project Report On Skill Development Under Tailoring Training by PeopleDocument8 pagesProject Report On Skill Development Under Tailoring Training by PeopleBiplab SwainPas encore d'évaluation

- Eng 329 Team1Document11 pagesEng 329 Team1b21fa1676Pas encore d'évaluation