Vous aimerez peut-être aussi

- Islamic Sales Contracts StructureDocument54 pagesIslamic Sales Contracts StructureFaisal Mir100% (1)

- Deposit and Investment ProductsDocument35 pagesDeposit and Investment ProductsNurulhikmah RoslanPas encore d'évaluation

- Islamic Modes of FinanceDocument23 pagesIslamic Modes of FinanceKassahun EssaPas encore d'évaluation

- Islamic Modes of Finance: Theory and Key Shariah PrinciplesDocument5 pagesIslamic Modes of Finance: Theory and Key Shariah PrinciplesAmmar HashmiPas encore d'évaluation

- 8th Mode of FinancingDocument30 pages8th Mode of FinancingYaseen IqbalPas encore d'évaluation

- Islamic Modes of Finance: Theory and Key Shariah PrinciplesDocument40 pagesIslamic Modes of Finance: Theory and Key Shariah PrinciplesnuasyamPas encore d'évaluation

- Islamic Modes of Financing MurabahaDocument53 pagesIslamic Modes of Financing MurabahaMuhammad AzeemPas encore d'évaluation

- Murabaha Finanacing in PakistanDocument47 pagesMurabaha Finanacing in Pakistanaamir mumtazPas encore d'évaluation

- Presentation On Istisna Financing Risks & Mitigation: Risk ManagementDocument9 pagesPresentation On Istisna Financing Risks & Mitigation: Risk ManagementAhmed Shahir UsmaniPas encore d'évaluation

- Derivatives. ... Syet Derivatives..Document42 pagesDerivatives. ... Syet Derivatives..Francis Emmanuel TolentinoPas encore d'évaluation

- Islamic Financial Contracts MurabahaDocument20 pagesIslamic Financial Contracts MurabahaFBusinessPas encore d'évaluation

- Murabaha - Concept & AAOIFIDocument45 pagesMurabaha - Concept & AAOIFIhasan_siddiqui_15Pas encore d'évaluation

- Islamic Financial Products and Processes: Ameenullah SheikhDocument18 pagesIslamic Financial Products and Processes: Ameenullah SheikhhamzaPas encore d'évaluation

- T3 - Salient Features and ContractsDocument49 pagesT3 - Salient Features and Contractsmichael musillaPas encore d'évaluation

- Lec 06 - Trade Based Financing-MurabahahDocument42 pagesLec 06 - Trade Based Financing-MurabahahOmayr QureshiPas encore d'évaluation

- UIB2612 1630 LECTURE 6 MurabahahDocument32 pagesUIB2612 1630 LECTURE 6 MurabahahSyahirah ArifPas encore d'évaluation

- IslamicDerivatives & StructredProductDocument75 pagesIslamicDerivatives & StructredProductSaid BouarfaouiPas encore d'évaluation

- Green Retro Markets and Finance Presentation - 20240213 - 085823 - 0000Document44 pagesGreen Retro Markets and Finance Presentation - 20240213 - 085823 - 0000Riza Mae AzulPas encore d'évaluation

- Chap 08 - MurabahaDocument18 pagesChap 08 - MurabahaSofia SohailPas encore d'évaluation

- Islamic Finance (Self Made Notes)Document8 pagesIslamic Finance (Self Made Notes)Muhammad Hamza AyoubPas encore d'évaluation

- Session 5 IstisnaDocument16 pagesSession 5 IstisnaShaheena SanaPas encore d'évaluation

- Chap 3 Part 2Document42 pagesChap 3 Part 2Intan SawalPas encore d'évaluation

- Chapter 05 Introduction To Islamic Banking and Finance - FinalDocument53 pagesChapter 05 Introduction To Islamic Banking and Finance - FinalNashaad SardheeyePas encore d'évaluation

- ICM04-Islamic Structured ProductsDocument33 pagesICM04-Islamic Structured ProductsDila DypPas encore d'évaluation

- Slides - MurabahaDocument21 pagesSlides - Murabahanursya syaPas encore d'évaluation

- Aasignment On Hire Purchase Finance and Consumer CreditDocument14 pagesAasignment On Hire Purchase Finance and Consumer Creditchaudhary92100% (3)

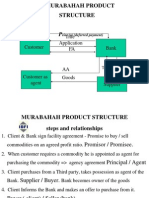

- Murabahah Product Structure: Title Application FADocument26 pagesMurabahah Product Structure: Title Application FAUmair UddinPas encore d'évaluation

- Murabaha FinanceDocument36 pagesMurabaha FinancesaadriazPas encore d'évaluation

- Islamic BK CH 3 PDFDocument27 pagesIslamic BK CH 3 PDFAA BB MMPas encore d'évaluation

- Derivatives - Cheat SheetDocument12 pagesDerivatives - Cheat SheetUchit MehtaPas encore d'évaluation

- ISBF NotesDocument13 pagesISBF Notesmuneebmateen01Pas encore d'évaluation

- Islamic Financial Accounting Standard-1 Murabaha: Interpretation and ImplementationDocument32 pagesIslamic Financial Accounting Standard-1 Murabaha: Interpretation and ImplementationMasoom ZahraPas encore d'évaluation

- Islamic Finance - Iqra UniversityDocument20 pagesIslamic Finance - Iqra UniversityalavihabibPas encore d'évaluation

- Rehmanwaheed 3180 17836 2 13. MurabahaDocument34 pagesRehmanwaheed 3180 17836 2 13. MurabahaSadia AbidPas encore d'évaluation

- Chapter 6 - Murabahah - Salam - Istisna 2Document42 pagesChapter 6 - Murabahah - Salam - Istisna 2d7gpxg55j9Pas encore d'évaluation

- Investment SideDocument52 pagesInvestment Sideayman FergeionPas encore d'évaluation

- Islamic Finance PrinciplesDocument31 pagesIslamic Finance Principlesbachtiar_aras6459Pas encore d'évaluation

- Diminishing Musharakah MBLDocument17 pagesDiminishing Musharakah MBLUbaid ArifPas encore d'évaluation

- Group OneDocument14 pagesGroup OneOmer WarsamehPas encore d'évaluation

- Al-Wadeah Principal and It's Feature Al-Wadeah Principal and It's FeatureDocument8 pagesAl-Wadeah Principal and It's Feature Al-Wadeah Principal and It's Featurevivekananda RoyPas encore d'évaluation

- Bai Istisna by Mufti MujeebDocument16 pagesBai Istisna by Mufti MujeebshagulhameedlPas encore d'évaluation

- Bank Credit - : Loans & AdvancesDocument75 pagesBank Credit - : Loans & AdvancesNikhilrajsingh ShekhawatPas encore d'évaluation

- Islamic Bonds SukukDocument18 pagesIslamic Bonds SukukJawad A SoomroPas encore d'évaluation

- Meezan Bank PresentationDocument17 pagesMeezan Bank PresentationHussnain RazaPas encore d'évaluation

- Updated LECTURE 2 - Risk Quantification (Basic Concepts)Document47 pagesUpdated LECTURE 2 - Risk Quantification (Basic Concepts)Ajid Ur Rehman100% (1)

- Islamic Financial Systems-2Document17 pagesIslamic Financial Systems-2محمد حسنین رضا قادریPas encore d'évaluation

- AFA 3e PPT Chap10Document79 pagesAFA 3e PPT Chap10Quỳnh NguyễnPas encore d'évaluation

- Diminishing Musharakah Presentation 02-06-08Document32 pagesDiminishing Musharakah Presentation 02-06-08AlHuda Centre of Islamic Banking & Economics (CIBE)Pas encore d'évaluation

- Futures and Options: Ibs Mumbai PGPM (2020-2022)Document12 pagesFutures and Options: Ibs Mumbai PGPM (2020-2022)Sayan GhoshPas encore d'évaluation

- Diminishing Musharakah - MBL - PpsDocument17 pagesDiminishing Musharakah - MBL - Ppsgul_e_sabaPas encore d'évaluation

- Diminishing Musharakah MBLDocument17 pagesDiminishing Musharakah MBLAATIF IMTIAZPas encore d'évaluation

- Islamic Banking PracticesDocument27 pagesIslamic Banking PracticesAadil HanifPas encore d'évaluation

- Chap 2 Part 2Document56 pagesChap 2 Part 2zakirah zalmiePas encore d'évaluation

- Introduction To Derivatives: 17th August, 2010Document47 pagesIntroduction To Derivatives: 17th August, 2010Amrita JhaPas encore d'évaluation

- Financial Engineering - Futures, Forwards and SwapsDocument114 pagesFinancial Engineering - Futures, Forwards and Swapsqari saibPas encore d'évaluation

- Accounting For InvestmentDocument29 pagesAccounting For InvestmentSyahrul AmirulPas encore d'évaluation

- Types of Channels: Value Chain Strategy: Channel Strategy SelectionDocument3 pagesTypes of Channels: Value Chain Strategy: Channel Strategy Selectionatiqa tanveerPas encore d'évaluation

- Submitted TO: SIR M.Yousaf "International Trade Barriers AND Their Solution"Document7 pagesSubmitted TO: SIR M.Yousaf "International Trade Barriers AND Their Solution"atiqa tanveerPas encore d'évaluation

- Carter 2011Document42 pagesCarter 2011atiqa tanveerPas encore d'évaluation

- Principles of Islamic Financial SystemDocument30 pagesPrinciples of Islamic Financial Systematiqa tanveerPas encore d'évaluation

- Risk Underlying Islamic Financial ModesDocument33 pagesRisk Underlying Islamic Financial Modesatiqa tanveerPas encore d'évaluation

- Socialism and Islamic Economic SystemDocument31 pagesSocialism and Islamic Economic Systematiqa tanveerPas encore d'évaluation

- Socialism and Islamic Economic SystemDocument31 pagesSocialism and Islamic Economic Systematiqa tanveerPas encore d'évaluation

- Islamic Modes of Financing: Ijarah (I)Document38 pagesIslamic Modes of Financing: Ijarah (I)atiqa tanveerPas encore d'évaluation

- Principles of Islamic Financial SystemDocument30 pagesPrinciples of Islamic Financial Systematiqa tanveerPas encore d'évaluation

- Capitalism and Islamic Economic SystemDocument30 pagesCapitalism and Islamic Economic Systematiqa tanveerPas encore d'évaluation

- Problems and Their Solution in MudarabahDocument43 pagesProblems and Their Solution in Mudarabahatiqa tanveerPas encore d'évaluation

- Islamic CairoDocument38 pagesIslamic Cairoapi-3747360Pas encore d'évaluation

- Guru NanakDocument104 pagesGuru NanakSabeeqa MalikPas encore d'évaluation

- BPUM - 3540 - Unit Pasir Pengaraian 1 SENTDocument45 pagesBPUM - 3540 - Unit Pasir Pengaraian 1 SENTRolaPas encore d'évaluation

- Dza Adminboundaries TabulardataDocument141 pagesDza Adminboundaries TabulardataMoussaouiPas encore d'évaluation

- 22 MoriscosDocument18 pages22 Moriscosapi-3860945Pas encore d'évaluation

- Dajjaal ReducedDocument128 pagesDajjaal ReducedJamaatu-l-FitrahPas encore d'évaluation

- How To Give Dawah To ShiasDocument32 pagesHow To Give Dawah To ShiasFaisal Umer100% (1)

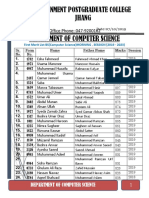

- Government Postgraduate College Jhang Department of Computer ScienceDocument10 pagesGovernment Postgraduate College Jhang Department of Computer ScienceMUHAMMAD SALEEM RAZAPas encore d'évaluation

- Employee Disciplinary MeasuresDocument16 pagesEmployee Disciplinary MeasuresSweet Miranda100% (2)

- Midterm Exam World Religions and Belief Systems Name: - Grade & SectionDocument2 pagesMidterm Exam World Religions and Belief Systems Name: - Grade & Sectionjovie100% (4)

- The Last Chapter of The Necronomicon, Edited by Allen MackeyDocument5 pagesThe Last Chapter of The Necronomicon, Edited by Allen MackeyALLEN MACKEYPas encore d'évaluation

- Cambridge O Level: Islamiyat 2058/22Document18 pagesCambridge O Level: Islamiyat 2058/22Muhammad YousafPas encore d'évaluation

- Faisal TownDocument18 pagesFaisal TownMuhammad Asif Hussain100% (1)

- Story of BrassTacks - An Epic Tale of Passion, Courage and RomanceDocument28 pagesStory of BrassTacks - An Epic Tale of Passion, Courage and RomanceBTghazwa88% (16)

- A Gift For The 27th Night DuaDocument7 pagesA Gift For The 27th Night Duaseemee23820Pas encore d'évaluation

- Imam Jafar Al Sadiq Book On Dream Interpretation English CompleteDocument66 pagesImam Jafar Al Sadiq Book On Dream Interpretation English CompletegoodhassanPas encore d'évaluation

- Darko Trifunović: Origins of Terrorism in BosniaDocument40 pagesDarko Trifunović: Origins of Terrorism in BosniaNeverGiveUp ForTheTruePas encore d'évaluation

- Partition of Bengal To Khilafat MovementDocument50 pagesPartition of Bengal To Khilafat MovementManzoor Marri100% (1)

- The Lost Two-Thirds Kuwaits TerritorialDocument20 pagesThe Lost Two-Thirds Kuwaits TerritorialAbo AliPas encore d'évaluation

- Islam in TamilnaduDocument116 pagesIslam in TamilnadurosgazPas encore d'évaluation

- Prime Bank Foundation: Finally Selected List For ESP Stipend 2017Document17 pagesPrime Bank Foundation: Finally Selected List For ESP Stipend 2017habibPas encore d'évaluation

- PENILAIANDocument15 pagesPENILAIANMuhammad AwaluddinPas encore d'évaluation

- Comparative Analysis of Judaism, Christianity, and IslamDocument15 pagesComparative Analysis of Judaism, Christianity, and IslamAlmirah100% (3)

- English Solution2 - Class 10 EnglishDocument34 pagesEnglish Solution2 - Class 10 EnglishTaqi ShahPas encore d'évaluation

- ScriptDocument3 pagesScriptREYNAN MEDINAPas encore d'évaluation

- Peran Wakaf Tunai Dalam Pengentasan Kemiskinan Di IndonesiaDocument12 pagesPeran Wakaf Tunai Dalam Pengentasan Kemiskinan Di Indonesiasyaidatul sadiahPas encore d'évaluation

- List of Candidates For Walk in Interview of Mos/Wmos On 29 MAY, 2021 District D.G. KhanDocument9 pagesList of Candidates For Walk in Interview of Mos/Wmos On 29 MAY, 2021 District D.G. KhanJALIL UR REHMANPas encore d'évaluation

- 184282eo PDFDocument891 pages184282eo PDFanil ariPas encore d'évaluation

- Islamiat Class 7Document9 pagesIslamiat Class 7humayunameer.7001Pas encore d'évaluation

- Rao Don DA P 29, 37Document109 pagesRao Don DA P 29, 37hoanglanhouPas encore d'évaluation