Vous aimerez peut-être aussi

- Appraisal Ce Exam 5 Review PDFDocument30 pagesAppraisal Ce Exam 5 Review PDFAmeerPas encore d'évaluation

- RedbookDocument76 pagesRedbookodigmailPas encore d'évaluation

- California Department of Motor Vehicles: Betty T. YeeDocument20 pagesCalifornia Department of Motor Vehicles: Betty T. YeePov TsheejPas encore d'évaluation

- Request Sample Ltr2CFO - Trustee For OIDs 11 - 2017Document2 pagesRequest Sample Ltr2CFO - Trustee For OIDs 11 - 2017ricetech92% (13)

- Forensic Loan Audit Report - Sample Report 4-2009Document47 pagesForensic Loan Audit Report - Sample Report 4-2009boufninaPas encore d'évaluation

- Membership Form of CDPDocument1 pageMembership Form of CDPCentrist Democratic Party of the PhilippinesPas encore d'évaluation

- Bank Appraisal PDFDocument61 pagesBank Appraisal PDFScott BowermanPas encore d'évaluation

- National Real Estate Salesperson License Exam Prep: The Ultimate Guide To Becoming a Real Estate Agent| The Complete Exam Prep with Practice Tests and Insider Tips & Tricks | Achieve a 98% Pass Rate on Your First Attempt!D'EverandNational Real Estate Salesperson License Exam Prep: The Ultimate Guide To Becoming a Real Estate Agent| The Complete Exam Prep with Practice Tests and Insider Tips & Tricks | Achieve a 98% Pass Rate on Your First Attempt!Pas encore d'évaluation

- Managing Local Government Financial ResourcesDocument38 pagesManaging Local Government Financial Resourcesarnetan711100% (2)

- NBP Chapter 8 AnalysisDocument7 pagesNBP Chapter 8 AnalysisMaliha HassanPas encore d'évaluation

- Bill of Lading DetailsDocument3 pagesBill of Lading DetailsThamaa Nagh' GhemblezzPas encore d'évaluation

- Risk Management Policy and GuidelinesDocument22 pagesRisk Management Policy and Guidelineskenoly123Pas encore d'évaluation

- 5 Credit InvestigationDocument4 pages5 Credit InvestigationLansing0% (1)

- Bank GuaranteeDocument30 pagesBank GuaranteeKaruna ThatsitPas encore d'évaluation

- General Ledger Chart of AccountsDocument5 pagesGeneral Ledger Chart of AccountsBala RanganathPas encore d'évaluation

- Internal Control Manual SummaryDocument14 pagesInternal Control Manual SummaryMarina OleynichenkoPas encore d'évaluation

- Solutions Manual: 1st EditionDocument23 pagesSolutions Manual: 1st EditionJunior Waqairasari67% (3)

- Fals TCBDocument58 pagesFals TCBDennis JudsonPas encore d'évaluation

- Ag IG ReportDocument37 pagesAg IG ReportLachlan MarkayPas encore d'évaluation

- Greenwich Central School District: Claims AuditingDocument12 pagesGreenwich Central School District: Claims AuditingBethany BumpPas encore d'évaluation

- GeneralAndSupplementaryValuationsFAQs Cape TownDocument12 pagesGeneralAndSupplementaryValuationsFAQs Cape TownWikusPas encore d'évaluation

- Mattituck Park District: Credit Cards and Segregation of DutiesDocument19 pagesMattituck Park District: Credit Cards and Segregation of DutiesSuffolk TimesPas encore d'évaluation

- Liberty Community Authority (LCA) - 2017 Financial Information - ER1087218-ER850925-ER1251592Document3 pagesLiberty Community Authority (LCA) - 2017 Financial Information - ER1087218-ER850925-ER1251592Dan MonkPas encore d'évaluation

- Mount Kisco Audit, Parking Ticket CollectionsDocument12 pagesMount Kisco Audit, Parking Ticket CollectionsCara MatthewsPas encore d'évaluation

- OCC Feb 2010 Home Mortgage Disclosure HandbookDocument30 pagesOCC Feb 2010 Home Mortgage Disclosure Handbook83jjmackPas encore d'évaluation

- State Comptrollers Office Audit of Mount Vernon City School DistrictDocument33 pagesState Comptrollers Office Audit of Mount Vernon City School DistrictAJROKPas encore d'évaluation

- New York Comptroller Thomas DiNapoli On Mount Vernon's Revenue CollectionDocument34 pagesNew York Comptroller Thomas DiNapoli On Mount Vernon's Revenue CollectionErnie GarciaPas encore d'évaluation

- Hud CommissionerDocument5 pagesHud CommissionerdesignzzzzPas encore d'évaluation

- Subrecipient Risk Assessment QuestionnaireDocument6 pagesSubrecipient Risk Assessment QuestionnaireGbadeyanka O WuraolaPas encore d'évaluation

- Liu Audit Rent BreaksDocument16 pagesLiu Audit Rent BreaksCeleste KatzPas encore d'évaluation

- State Board of Elections: Audit ReportDocument37 pagesState Board of Elections: Audit ReportMark NewgentPas encore d'évaluation

- Dallas Central Appraisal District Frequently Asked Questions Establishing ValueDocument3 pagesDallas Central Appraisal District Frequently Asked Questions Establishing ValueLSPas encore d'évaluation

- Town of Woodstock: Financial Activities and Information TechnologyDocument26 pagesTown of Woodstock: Financial Activities and Information TechnologyTony AdamisPas encore d'évaluation

- Ulster County Resource Recovery Agency: Selected Financial OperationsDocument31 pagesUlster County Resource Recovery Agency: Selected Financial OperationsElliott AuerbachPas encore d'évaluation

- Eastchester Audit, Parking Ticket CollectionsDocument14 pagesEastchester Audit, Parking Ticket CollectionsCara MatthewsPas encore d'évaluation

- Measure J WordingDocument7 pagesMeasure J WordingLivermoreParentsPas encore d'évaluation

- 2021 Assessment-ManualDocument20 pages2021 Assessment-ManualjmarkgPas encore d'évaluation

- Investment Manangement ProgramDocument14 pagesInvestment Manangement ProgramRolando VasquezPas encore d'évaluation

- AB 1484 SummaryDocument6 pagesAB 1484 SummaryJbrownie HeimesPas encore d'évaluation

- Saratoga Springs Housing Authority AuditDocument43 pagesSaratoga Springs Housing Authority AuditDavid LombardoPas encore d'évaluation

- Eastchester Fire District: Internal Controls Over Financial OperationsDocument27 pagesEastchester Fire District: Internal Controls Over Financial OperationsCara MatthewsPas encore d'évaluation

- DOI Final Evaluation NPS Cell TowersDocument27 pagesDOI Final Evaluation NPS Cell TowersAlyssa RobertsPas encore d'évaluation

- Obsoguidelines - PENTINGDocument30 pagesObsoguidelines - PENTINGHarryPas encore d'évaluation

- FS38 Treatment of Property in The Means-Test For Permanent Care Home Provision FcsDocument28 pagesFS38 Treatment of Property in The Means-Test For Permanent Care Home Provision FcsIp CamPas encore d'évaluation

- Town of Hurley AuditDocument30 pagesTown of Hurley AuditTony AdamisPas encore d'évaluation

- Performance Audit Division of Building & Codes: Revenues and ExpensesDocument15 pagesPerformance Audit Division of Building & Codes: Revenues and ExpensestulocalpoliticsPas encore d'évaluation

- Athens Volunteer Firemen's Relief Association Audit Report Jan. 2022Document17 pagesAthens Volunteer Firemen's Relief Association Audit Report Jan. 2022Carl AldingerPas encore d'évaluation

- Limited Purpose Bank: Public DisclosureDocument12 pagesLimited Purpose Bank: Public DisclosureanshPas encore d'évaluation

- Local Govt Administration: Finances of Local Authorities in MalaysiaDocument30 pagesLocal Govt Administration: Finances of Local Authorities in MalaysiaArimanthea LeePas encore d'évaluation

- CCAO - County Budgets - 49 PgsDocument49 pagesCCAO - County Budgets - 49 PgsJHPas encore d'évaluation

- Alabama Department of Examiners of Public Accounts Report of Indian Ford Fire DistrictDocument23 pagesAlabama Department of Examiners of Public Accounts Report of Indian Ford Fire DistrictABC 33/40Pas encore d'évaluation

- Handouts FM LGU FinalDocument6 pagesHandouts FM LGU FinalCathy Pascual NonatoPas encore d'évaluation

- Internal Controls Over Credit Cards and Travel and Fuel ExpendituresDocument23 pagesInternal Controls Over Credit Cards and Travel and Fuel ExpendituresArica HarrisPas encore d'évaluation

- What Is A Metropolitan DistrictDocument4 pagesWhat Is A Metropolitan DistrictEaglebendmetroPas encore d'évaluation

- Department of The Lottery S A A P A F - U: Elected Dministrative Ctivities and Rior Udit Ollow PDocument11 pagesDepartment of The Lottery S A A P A F - U: Elected Dministrative Ctivities and Rior Udit Ollow PChris JosephPas encore d'évaluation

- BMHA AuditDocument26 pagesBMHA AuditWGRZ-TVPas encore d'évaluation

- Analisysis of Factor That Affect The Opinion of The BPK Regional Financial Gavernment Report in IndonesiaDocument17 pagesAnalisysis of Factor That Affect The Opinion of The BPK Regional Financial Gavernment Report in IndonesiaLucfia AnissatulPas encore d'évaluation

- Comptroller Audit Albany County Sheriff'sDocument22 pagesComptroller Audit Albany County Sheriff'sBrendan LyonsPas encore d'évaluation

- SAI-LGAS MDLSGDDocument6 pagesSAI-LGAS MDLSGDlovellev.ev3Pas encore d'évaluation

- Lec 26Document35 pagesLec 26Sanskruti WaghmarePas encore d'évaluation

- 2014-2018 Jackson County Capital Improvement ProgramDocument59 pages2014-2018 Jackson County Capital Improvement ProgramLivewire Printing CompanyPas encore d'évaluation

- Louisville Code Enforcement ReportDocument15 pagesLouisville Code Enforcement ReportBailey LoosemorePas encore d'évaluation

- Responses To Council Questions On Homelessness InvestmentDocument26 pagesResponses To Council Questions On Homelessness InvestmentUSA TODAY NetworkPas encore d'évaluation

- September - Malita Notes (Part 1)Document27 pagesSeptember - Malita Notes (Part 1)YeimePas encore d'évaluation

- JP OIG Audit-Rickey Jackson Community Hope CenterDocument112 pagesJP OIG Audit-Rickey Jackson Community Hope CenterWWLTVWebteamPas encore d'évaluation

- Selection of Location For A ProjectDocument35 pagesSelection of Location For A ProjectTushar PatilPas encore d'évaluation

- Federal Accounting Handbook: Policies, Standards, Procedures, PracticesD'EverandFederal Accounting Handbook: Policies, Standards, Procedures, PracticesPas encore d'évaluation

- Right To Farm Act BasicsDocument3 pagesRight To Farm Act BasicsDennis JudsonPas encore d'évaluation

- MCL Act 93 of 1981Document4 pagesMCL Act 93 of 1981Dennis JudsonPas encore d'évaluation

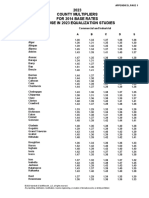

- 2023 County Multipliers Commercial and IndustrialDocument2 pages2023 County Multipliers Commercial and IndustrialDennis JudsonPas encore d'évaluation

- 2023 County Multipliers Residential FarmDocument1 page2023 County Multipliers Residential FarmDennis JudsonPas encore d'évaluation

- Suppliment - Four Against The KrampusDocument11 pagesSuppliment - Four Against The KrampusDennis JudsonPas encore d'évaluation

- A. Inflation Rate Used in The 2022 Capped Value FormulaDocument9 pagesA. Inflation Rate Used in The 2022 Capped Value FormulaDennis JudsonPas encore d'évaluation

- Who Can Grant WhatDocument3 pagesWho Can Grant WhatDennis JudsonPas encore d'évaluation

- Amar 2.0Document46 pagesAmar 2.0Dennis JudsonPas encore d'évaluation

- AMAR AfternoonDocument102 pagesAMAR AfternoonDennis JudsonPas encore d'évaluation

- AMAR Class MorningDocument8 pagesAMAR Class MorningDennis JudsonPas encore d'évaluation

- International Standard On Auditing 510 Initial Audit Engagements-Opening BalancesDocument13 pagesInternational Standard On Auditing 510 Initial Audit Engagements-Opening BalancesFalah Ud Din SheryarPas encore d'évaluation

- DanielSMahantyCISACIACISSP (30 0)Document6 pagesDanielSMahantyCISACIACISSP (30 0)Manasmitha RaguramPas encore d'évaluation

- CSIM Batch FormateDocument45 pagesCSIM Batch FormateAnand sharmaPas encore d'évaluation

- Commission On Audit: Ridzanna M. Abdulgafur Alayka A. Anuddin Stephany A. PolinarDocument35 pagesCommission On Audit: Ridzanna M. Abdulgafur Alayka A. Anuddin Stephany A. PolinarStephany PolinarPas encore d'évaluation

- Savings Account Scheme ChangesDocument10 pagesSavings Account Scheme ChangesbhanupalavarapuPas encore d'évaluation

- Comparative Liquidity Analysis of NepalDocument57 pagesComparative Liquidity Analysis of NepalMd ReyajuddinPas encore d'évaluation

- Zain Traders Assignment 2Document2 pagesZain Traders Assignment 2Bilal Ahmed100% (1)

- Usage Guide - Rewards Plus PDFDocument8 pagesUsage Guide - Rewards Plus PDFHemant JainPas encore d'évaluation

- MFL Scope of Work - Role Requirements - Project Management Consultancy ServicesDocument6 pagesMFL Scope of Work - Role Requirements - Project Management Consultancy ServicesAdreaPas encore d'évaluation

- History of The First Building and Loan Association in PhiladelphiaDocument1 pageHistory of The First Building and Loan Association in PhiladelphiaRichard CastorPas encore d'évaluation

- Ar 2020 21Document72 pagesAr 2020 21Joey KamPas encore d'évaluation

- Sme BookDocument397 pagesSme BookVivek Godgift J0% (1)

- Kyc-Aml-Cft - Policy KMBT - 215 - 04431Document11 pagesKyc-Aml-Cft - Policy KMBT - 215 - 04431Santosh JayasavalPas encore d'évaluation

- LIQUIDITY RISK AND LIQUIDITY MANAGEMENT IN ISLAMIC BANKS (DR Salman)Document29 pagesLIQUIDITY RISK AND LIQUIDITY MANAGEMENT IN ISLAMIC BANKS (DR Salman)lahem88100% (4)

- Value Line Pro Brochures CompleteDocument15 pagesValue Line Pro Brochures CompleteSilviu TrebuianPas encore d'évaluation

- Thailand SMART Member Bank CodeDocument1 pageThailand SMART Member Bank CodenatascoeurPas encore d'évaluation

- Money in The Modern Economy An Introduction PDFDocument10 pagesMoney in The Modern Economy An Introduction PDFTharindu DissanayakePas encore d'évaluation

- G.R. No. 174269 - Pantaleon Vs AmEx (2009)Document3 pagesG.R. No. 174269 - Pantaleon Vs AmEx (2009)Sarah Jade LayugPas encore d'évaluation

- Harshad MehtaDocument5 pagesHarshad MehtaSanil MeledathPas encore d'évaluation

- SSIs - PROBLEMSDocument25 pagesSSIs - PROBLEMSKaran KumarPas encore d'évaluation

- MOU For Sunrise Bank LimitedDocument4 pagesMOU For Sunrise Bank Limitedshobha swarPas encore d'évaluation

- Guidance Note On Audit of Banks by IcaiDocument955 pagesGuidance Note On Audit of Banks by IcaiTekumani Naveen Kumar100% (1)