Vous aimerez peut-être aussi

- Risk Management and Basel II: Bank Alfalah LimitedDocument72 pagesRisk Management and Basel II: Bank Alfalah LimitedtanhaitanhaPas encore d'évaluation

- Analyzing Banking Risk (Fourth Edition): A Framework for Assessing Corporate Governance and Risk ManagementD'EverandAnalyzing Banking Risk (Fourth Edition): A Framework for Assessing Corporate Governance and Risk ManagementÉvaluation : 5 sur 5 étoiles5/5 (5)

- Teaching C.S. Lewis:: A Handbook For Professors, Church Leaders, and Lewis EnthusiastsDocument30 pagesTeaching C.S. Lewis:: A Handbook For Professors, Church Leaders, and Lewis EnthusiastsAyo Abe LighthousePas encore d'évaluation

- KPMG Software Testing Services - GenericDocument24 pagesKPMG Software Testing Services - GenericmaheshsamuelPas encore d'évaluation

- Tariff and Customs LawDocument15 pagesTariff and Customs LawJel LyPas encore d'évaluation

- Key Features of Basel IDocument16 pagesKey Features of Basel IAltaf Hasan KhanPas encore d'évaluation

- Basel II Capital Accord SlidesDocument25 pagesBasel II Capital Accord SlidesAamir RazaPas encore d'évaluation

- Special Issues in Indian Banking Sector ReportDocument78 pagesSpecial Issues in Indian Banking Sector ReportAli AttarwalaPas encore d'évaluation

- 1.RISK CompediumDocument95 pages1.RISK CompediumyogeshthakkerPas encore d'évaluation

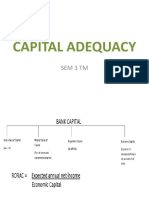

- Capital Adequacy: Sem 3 TMDocument45 pagesCapital Adequacy: Sem 3 TMahsan habibPas encore d'évaluation

- Basel 2 - DeloitteDocument29 pagesBasel 2 - DeloitteSENTHIL KUMARPas encore d'évaluation

- Risk Management and Basel II: Indian Institute of Banking and FinanceDocument31 pagesRisk Management and Basel II: Indian Institute of Banking and FinanceKaran AsraniPas encore d'évaluation

- Risk-Based Capital Management for BanksDocument39 pagesRisk-Based Capital Management for BanksUdita GopalkrishnaPas encore d'évaluation

- Basel I, II and III ExplainedDocument31 pagesBasel I, II and III ExplainedLalitha RamaswamyPas encore d'évaluation

- Basel II Compliance Solution Framework OverviewDocument12 pagesBasel II Compliance Solution Framework OverviewgirrajmeenaPas encore d'évaluation

- Basel II Compliance Solution FrameworkDocument12 pagesBasel II Compliance Solution Frameworkamol2982Pas encore d'évaluation

- Basel Ii at A GlanceDocument13 pagesBasel Ii at A GlanceNaushad AnsariPas encore d'évaluation

- The New Basel Capital Accord Oliver WymanDocument4 pagesThe New Basel Capital Accord Oliver Wymanrafa_a24Pas encore d'évaluation

- Presented By: Arpita Gupta Disha Sogani Priyamvada Romi SharmaDocument17 pagesPresented By: Arpita Gupta Disha Sogani Priyamvada Romi SharmaPriyamvada ShekhawatPas encore d'évaluation

- The Critical Challenge Facing Banks and Regulators Under Basel II: Improving Risk Management Through Implementation of Pillar 2Document16 pagesThe Critical Challenge Facing Banks and Regulators Under Basel II: Improving Risk Management Through Implementation of Pillar 2Hassan MphandePas encore d'évaluation

- Module D Capital Adequacy and Profit Planning: A Presentation byDocument50 pagesModule D Capital Adequacy and Profit Planning: A Presentation bySaravanan KaruppiahPas encore d'évaluation

- BaselDocument38 pagesBaselsourabhs90Pas encore d'évaluation

- Basel II PresentationDocument21 pagesBasel II PresentationMuhammad SaqibPas encore d'évaluation

- A Presentation On: A Presentation On Basel Committee Norms As Regards To Financial Sector Reforms in IndiaDocument23 pagesA Presentation On: A Presentation On Basel Committee Norms As Regards To Financial Sector Reforms in Indiavidha_s23Pas encore d'évaluation

- Moving Towards Basel Ii: Issues & ConcernsDocument36 pagesMoving Towards Basel Ii: Issues & Concernstejasdhanu786Pas encore d'évaluation

- Basel Ii Overview: February 2017Document35 pagesBasel Ii Overview: February 2017Venkatsubramanian R IyerPas encore d'évaluation

- 3c. - Pillars of CapitalDocument30 pages3c. - Pillars of Capitalonly.oranda.goldfishPas encore d'évaluation

- Capital Adequacy Mms 2011Document121 pagesCapital Adequacy Mms 2011Aishwary KhandelwalPas encore d'évaluation

- Introduction To Basel IIDocument16 pagesIntroduction To Basel IIsushma_namepalliPas encore d'évaluation

- Taking and Managing Risks EffectivelyDocument28 pagesTaking and Managing Risks EffectivelyVijayPas encore d'évaluation

- BaselDocument37 pagesBaselRohit BeheraPas encore d'évaluation

- FRR-ALM Ch4Document66 pagesFRR-ALM Ch4Marek KurzyńskiPas encore d'évaluation

- Basel NormsDocument42 pagesBasel NormsBluehacksPas encore d'évaluation

- Risk Management in The Banking SectorDocument47 pagesRisk Management in The Banking SectorGaurEeshPas encore d'évaluation

- Current Level of Basel II ImplementationDocument20 pagesCurrent Level of Basel II ImplementationSneha BhorawatPas encore d'évaluation

- Basel II and Risk MGMTDocument6 pagesBasel II and Risk MGMTSagar ShahPas encore d'évaluation

- Base 2Document20 pagesBase 2asifanisPas encore d'évaluation

- Challenges To Indian BankingDocument28 pagesChallenges To Indian Bankinga_mohapatra55552752100% (1)

- Credit Risk ModellingDocument40 pagesCredit Risk ModellingSwaraj Dhar100% (2)

- Risk Management OverviewDocument35 pagesRisk Management OverviewSrinivas AcharPas encore d'évaluation

- Risk Based Internal Audit TrainingDocument4 pagesRisk Based Internal Audit TrainingaPas encore d'évaluation

- International Risk RegulationDocument15 pagesInternational Risk RegulationArinaSofiyaPas encore d'évaluation

- Basel II Report on Norms and Growth ImplicationsDocument12 pagesBasel II Report on Norms and Growth ImplicationsUmesha H SiddaiahPas encore d'évaluation

- Capital Adequacy: Prof. B.B.BhattacharyyaDocument115 pagesCapital Adequacy: Prof. B.B.BhattacharyyaSheetal IyerPas encore d'évaluation

- Pillar 3 USB Disclosure 6-30-17Document33 pagesPillar 3 USB Disclosure 6-30-17Siva RenjithPas encore d'évaluation

- Capital Adequacy NormsDocument26 pagesCapital Adequacy Normspuneeta chughPas encore d'évaluation

- Building A Holistic Capital Management FrameworkDocument16 pagesBuilding A Holistic Capital Management FrameworkCognizantPas encore d'évaluation

- Basel Capital Accord & Risk Management - A Perspective: B. BanerjiDocument55 pagesBasel Capital Accord & Risk Management - A Perspective: B. BanerjiprateeekPas encore d'évaluation

- Key Bank Capital RegulationsDocument38 pagesKey Bank Capital RegulationsNANDINI GUPTAPas encore d'évaluation

- Risk ManagementDocument31 pagesRisk ManagementAnkit ChawlaPas encore d'évaluation

- IAASB ISA 315 Revised 2019Document16 pagesIAASB ISA 315 Revised 2019Bianca Marie PedrozoPas encore d'évaluation

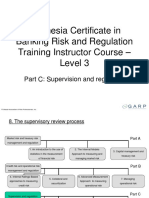

- Indonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3Document46 pagesIndonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3endro suendroPas encore d'évaluation

- Glossary: Capital Earnings Funds and Investment Asset Securitisation Nds-Om Web HomeDocument16 pagesGlossary: Capital Earnings Funds and Investment Asset Securitisation Nds-Om Web HomeSanjeet MohantyPas encore d'évaluation

- College ProjectDocument72 pagesCollege Projectcha7738713649Pas encore d'évaluation

- Risk Management & Basel Ii: By: Kajal Gupta Deepanshu Sapra Sanchit BhasinDocument11 pagesRisk Management & Basel Ii: By: Kajal Gupta Deepanshu Sapra Sanchit Bhasinsanchit bhasinPas encore d'évaluation

- Understanding Internal Capital Adequacy Assessment Process IcaapDocument2 pagesUnderstanding Internal Capital Adequacy Assessment Process IcaapArunjit SutradharPas encore d'évaluation

- Class Notes Financial Risk M: F PGDMDocument11 pagesClass Notes Financial Risk M: F PGDMprat05Pas encore d'évaluation

- Risk Management: Capital Management & Profit PlanningDocument25 pagesRisk Management: Capital Management & Profit Planningharry2learnPas encore d'évaluation

- On Capital AdequacyDocument46 pagesOn Capital Adequacymanishasain75% (8)

- Finance Basel Norms Revision SheetsDocument8 pagesFinance Basel Norms Revision SheetsMR SOUMIK GHOSHPas encore d'évaluation

- (Bank Policy) BASELDocument30 pages(Bank Policy) BASELprachiz1Pas encore d'évaluation

- Basel Norms I, II and IIIDocument30 pagesBasel Norms I, II and IIIYashwanth PrasadPas encore d'évaluation

- The Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiD'EverandThe Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiPas encore d'évaluation

- Galvanize Action donation instructionsDocument1 pageGalvanize Action donation instructionsRasaq LakajePas encore d'évaluation

- CRPC 1973 PDFDocument5 pagesCRPC 1973 PDFAditi SinghPas encore d'évaluation

- PMT Machines LTD Inspection and Test Plan For Bogie Frame FabricationDocument6 pagesPMT Machines LTD Inspection and Test Plan For Bogie Frame FabricationAMIT SHAHPas encore d'évaluation

- Solution Manual For Fundamentals of Modern Manufacturing 6Th Edition by Groover Isbn 1119128692 9781119128694 Full Chapter PDFDocument24 pagesSolution Manual For Fundamentals of Modern Manufacturing 6Th Edition by Groover Isbn 1119128692 9781119128694 Full Chapter PDFsusan.lemke155100% (11)

- PSEA Self Assessment Form - 2024 02 02 102327 - YjloDocument2 pagesPSEA Self Assessment Form - 2024 02 02 102327 - Yjlokenedy nuwaherezaPas encore d'évaluation

- Chapter 3-Hedging Strategies Using Futures-29.01.2014Document26 pagesChapter 3-Hedging Strategies Using Futures-29.01.2014abaig2011Pas encore d'évaluation

- Fta Checklist Group NV 7-6-09Document7 pagesFta Checklist Group NV 7-6-09initiative1972Pas encore d'évaluation

- SAS HB 06 Weapons ID ch1 PDFDocument20 pagesSAS HB 06 Weapons ID ch1 PDFChris EfstathiouPas encore d'évaluation

- Pilot Registration Process OverviewDocument48 pagesPilot Registration Process OverviewMohit DasPas encore d'évaluation

- HertzDocument2 pagesHertzChhavi AnandPas encore d'évaluation

- Cruise LetterDocument23 pagesCruise LetterSimon AlvarezPas encore d'évaluation

- Introduction To The Appian PlatformDocument13 pagesIntroduction To The Appian PlatformbolillapalidaPas encore d'évaluation

- BGAS-CSWIP 10 Year Re-Certification Form (Overseas) No LogbookDocument7 pagesBGAS-CSWIP 10 Year Re-Certification Form (Overseas) No LogbookMedel Cay De CastroPas encore d'évaluation

- Coiculescu PDFDocument2 pagesCoiculescu PDFprateek_301466650Pas encore d'évaluation

- PLAI 10 Point AgendaDocument24 pagesPLAI 10 Point Agendaapacedera689100% (2)

- Case 50Document4 pagesCase 50Phan Tuan AnhPas encore d'évaluation

- Introduction to Social Media AnalyticsDocument26 pagesIntroduction to Social Media AnalyticsDiksha TanejaPas encore d'évaluation

- CardingDocument9 pagesCardingSheena JindalPas encore d'évaluation

- AACCSA Journal of Trade and Business V.1 No. 1Document90 pagesAACCSA Journal of Trade and Business V.1 No. 1Peter MuigaiPas encore d'évaluation

- Types of Electronic CommerceDocument2 pagesTypes of Electronic CommerceVivek RajPas encore d'évaluation

- James M Stearns JR ResumeDocument2 pagesJames M Stearns JR Resumeapi-281469512Pas encore d'évaluation

- Employee Separation Types and ReasonsDocument39 pagesEmployee Separation Types and ReasonsHarsh GargPas encore d'évaluation

- Handout 2Document2 pagesHandout 2Manel AbdeljelilPas encore d'évaluation

- Sunmeet Logistic Company ProfileDocument5 pagesSunmeet Logistic Company ProfileKomal PatilPas encore d'évaluation

- Detailed Project Report Bread Making Unit Under Pmfme SchemeDocument26 pagesDetailed Project Report Bread Making Unit Under Pmfme SchemeMohammed hassenPas encore d'évaluation

- Service Culture Module 2Document2 pagesService Culture Module 2Cedrick SedaPas encore d'évaluation

- Gurdjieff & Fritz Peters, Part IDocument7 pagesGurdjieff & Fritz Peters, Part IThe Gurdjieff JournalPas encore d'évaluation