Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Name of Investors (Bidders) Interest Rate (%) Auction Volume (Billion Dong)Document2 pagesName of Investors (Bidders) Interest Rate (%) Auction Volume (Billion Dong)Trần Phương AnhPas encore d'évaluation

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- A Comparative Study of Home Loan Schemes of Private Sector Banks Public Sector BanksDocument12 pagesA Comparative Study of Home Loan Schemes of Private Sector Banks Public Sector BanksKapil KumarPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Ecuador Bondholder Groups Release Revised Terms - July 13, 2020Document5 pagesEcuador Bondholder Groups Release Revised Terms - July 13, 2020Daniel BasesPas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Business 2257 Tutorial #1Document12 pagesBusiness 2257 Tutorial #1westernbebePas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Valuation With Market Multiples Avoid Pitfalls in The Use of Relative ValuationDocument15 pagesValuation With Market Multiples Avoid Pitfalls in The Use of Relative ValuationAlexCooks100% (1)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Model Question For Account409792809472943360Document8 pagesModel Question For Account409792809472943360yugeshPas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Sanjay Bakshi: Dear StudentsDocument2 pagesSanjay Bakshi: Dear StudentsBharat SahniPas encore d'évaluation

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- International Corporate Finance 11 Edition: by Jeff MaduraDocument34 pagesInternational Corporate Finance 11 Edition: by Jeff MaduraMahmoud SamyPas encore d'évaluation

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- JAVA MicroprojectDocument31 pagesJAVA Microprojectᴠɪɢʜɴᴇꜱʜ ɴᴀʀᴀᴡᴀᴅᴇ.Pas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- AIA Philam Life Policy Fund Withdrawal FormDocument2 pagesAIA Philam Life Policy Fund Withdrawal Formippon_osotoPas encore d'évaluation

- Starbucks Corporation - FinancialsDocument3 pagesStarbucks Corporation - FinancialsAtish GoolaupPas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

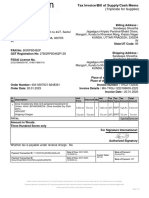

- Invoice DocumentDocument1 pageInvoice DocumentrameshPas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Sign. Primary Acc. Holder Sign Acc. Holder Sign Acc. HolderDocument1 pageSign. Primary Acc. Holder Sign Acc. Holder Sign Acc. HolderBrijesh EnterprisesPas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Tax SssssssDocument3 pagesTax SssssssJames Francis VillanuevaPas encore d'évaluation

- Tally Accounting Book by Ca MD ImranDocument6 pagesTally Accounting Book by Ca MD ImranMd ImranPas encore d'évaluation

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- 6th NLIU Trilegal Summit 2021 BrochureDocument11 pages6th NLIU Trilegal Summit 2021 Brochuremihir khannaPas encore d'évaluation

- Takeover and AcquisitionsDocument42 pagesTakeover and Acquisitionsparasjain100% (1)

- 2016 SMIC Annual ReportDocument120 pages2016 SMIC Annual ReportPatricia ReyesPas encore d'évaluation

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Cost of CapitalDocument37 pagesCost of Capitalwasiq999Pas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Fee Receipt - Lucknow UniversityDocument3 pagesFee Receipt - Lucknow UniversityNirbhay NirajPas encore d'évaluation

- ATA Contract Virtual OfficeDocument6 pagesATA Contract Virtual OfficeGuo YanmingPas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Workshop 3Document30 pagesWorkshop 3Jeevika BasnetPas encore d'évaluation

- Pradhan Mantri Fasal Bima Yojna (Pmfby) : Bajaj Allianz General Insurance Company LimitedDocument2 pagesPradhan Mantri Fasal Bima Yojna (Pmfby) : Bajaj Allianz General Insurance Company LimitedRahulSinghPas encore d'évaluation

- Bar Review Material No. 3 PDFDocument2 pagesBar Review Material No. 3 PDFScri Bid100% (1)

- Merger of JSW Steel Limited & Ispat Industries LimitedDocument2 pagesMerger of JSW Steel Limited & Ispat Industries Limitedpriteshvadera12345Pas encore d'évaluation

- Symfonie Angel Ventures AML 20130715Document13 pagesSymfonie Angel Ventures AML 20130715Symfonie CapitalPas encore d'évaluation

- Hull OFOD10e MultipleChoice Questions and Answers Ch17Document7 pagesHull OFOD10e MultipleChoice Questions and Answers Ch17Kevin Molly KamrathPas encore d'évaluation

- 10 Pages Directors' Summary - by CA Harsh GuptaDocument10 pages10 Pages Directors' Summary - by CA Harsh Guptagovarthan1976Pas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Chinmay Kadam Roll No. 21 Black BookDocument55 pagesChinmay Kadam Roll No. 21 Black BookShubh shahPas encore d'évaluation

- Invoice2024 01 06Document1 pageInvoice2024 01 06hugocasdevPas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)