Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Bill DiscountingDocument69 pagesBill DiscountingDhanesh BabarPas encore d'évaluation

- Horary and Sublord in RetroDocument1 pageHorary and Sublord in RetroProfessorAsim Kumar MishraPas encore d'évaluation

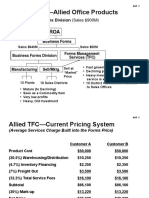

- ABC Costing Allied Office ProductsDocument13 pagesABC Costing Allied Office ProductsProfessorAsim Kumar Mishra100% (1)

- Announcement Effects of Bonus Issues On Equity Prices: The Indian ExperienceDocument15 pagesAnnouncement Effects of Bonus Issues On Equity Prices: The Indian ExperienceProfessorAsim Kumar MishraPas encore d'évaluation

- "Simple Rules of 4 Step Theory": Rule 1Document5 pages"Simple Rules of 4 Step Theory": Rule 1SaptarishisAstrology100% (2)

- TMP For AstroDocument4 pagesTMP For AstroProfessorAsim Kumar MishraPas encore d'évaluation

- 12 Signs of The ZodiacDocument9 pages12 Signs of The ZodiacProfessorAsim Kumar MishraPas encore d'évaluation

- Journal For Advancement of Stellar AstrologyDocument95 pagesJournal For Advancement of Stellar Astrologyandrew_dutta67% (3)

- Nov-Dec 2011 Issue of JASADocument0 pageNov-Dec 2011 Issue of JASAProfessorAsim Kumar MishraPas encore d'évaluation

- 8th House in MarriageDocument3 pages8th House in MarriageProfessorAsim Kumar MishraPas encore d'évaluation

- JASA Mar Apr 2012 IssueDocument104 pagesJASA Mar Apr 2012 IssueandrewduttaPas encore d'évaluation

- JASA Oct-Dec 2013 IssueDocument116 pagesJASA Oct-Dec 2013 Issuekumarkumar123Pas encore d'évaluation

- JASA May-Jun 2012 IssueDocument106 pagesJASA May-Jun 2012 IssueandrewduttaPas encore d'évaluation

- Astrology of Karma PDFDocument210 pagesAstrology of Karma PDFProfessorAsim Kumar Mishra100% (1)

- How K.P Pinpoint Events-Prasna PDFDocument59 pagesHow K.P Pinpoint Events-Prasna PDFdhritimohan100% (2)

- 8th House in MarriageDocument3 pages8th House in MarriageProfessorAsim Kumar MishraPas encore d'évaluation

- Astrovision EmagazineDocument65 pagesAstrovision EmagazineD.k. Pathak100% (1)

- KP BookDocument41 pagesKP Bookanand_kpm100% (4)

- IAS PROFESSION KP Analysis PDFDocument5 pagesIAS PROFESSION KP Analysis PDFProfessorAsim Kumar Mishra100% (2)

- Role of Nodes in KPDocument16 pagesRole of Nodes in KPRaj Yadav100% (3)

- Longevity Analysis PDFDocument53 pagesLongevity Analysis PDFProfessorAsim Kumar Mishra100% (3)

- Romance Astrology PDFDocument311 pagesRomance Astrology PDFProfessorAsim Kumar Mishra89% (9)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1091)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Report BSM at Indon - Thai 17 19 3 2015 (Final)Document50 pagesReport BSM at Indon - Thai 17 19 3 2015 (Final)J.T Haloho100% (1)

- ISQ Infrastructures ServicesDocument14 pagesISQ Infrastructures ServicesAnabela BentoPas encore d'évaluation

- Uzbekistan THE NATIONAL - GREEN - ECONOMY TAXONOMYDocument15 pagesUzbekistan THE NATIONAL - GREEN - ECONOMY TAXONOMYIgor PancevskiPas encore d'évaluation

- Unit-Ii: (10 Hours) : Socio-Economic AspectsDocument5 pagesUnit-Ii: (10 Hours) : Socio-Economic AspectsNivashini BaskaranPas encore d'évaluation

- محاضرة رقم 14Document22 pagesمحاضرة رقم 14Zainab A. AbdulstaarPas encore d'évaluation

- Government Infrastructure Projects: Construction of Burgos-Lidlidda Road, Burgos, Ilocos SurDocument4 pagesGovernment Infrastructure Projects: Construction of Burgos-Lidlidda Road, Burgos, Ilocos SurArnold Apostol Jr.Pas encore d'évaluation

- Final Report The Purse Project PDFDocument115 pagesFinal Report The Purse Project PDFTata RaminathaPas encore d'évaluation

- Environmental Protection Laws and Sustainable Development Niger Delta AFRICANA Vol4 No1Document33 pagesEnvironmental Protection Laws and Sustainable Development Niger Delta AFRICANA Vol4 No1SallyPas encore d'évaluation

- Soil Data at MyanmarDocument82 pagesSoil Data at MyanmarSuu ChatePas encore d'évaluation

- TOT Model Toll Operate Transfer ModelDocument5 pagesTOT Model Toll Operate Transfer Modelyash panchalPas encore d'évaluation

- CycleTracksPresentation 2.17.10Document81 pagesCycleTracksPresentation 2.17.10Anil Kumsr T BPas encore d'évaluation

- Pap II Regional Water Meeting Report FinalDocument45 pagesPap II Regional Water Meeting Report FinalCheikh SENEPas encore d'évaluation

- Chap 4 - Shallow Ult PDFDocument58 pagesChap 4 - Shallow Ult PDFChiến Lê100% (2)

- ABM 11 - ORGANIZATION AND MANAGEMENT - Q1 - W4 - Mod4Document13 pagesABM 11 - ORGANIZATION AND MANAGEMENT - Q1 - W4 - Mod4Anne MoralesPas encore d'évaluation

- LPG Reticulation Systems For Householdoctober 2023Document42 pagesLPG Reticulation Systems For Householdoctober 2023Iddi OmarPas encore d'évaluation

- Boao Review No. 13 201507 EnglishDocument112 pagesBoao Review No. 13 201507 EnglishChanPas encore d'évaluation

- Federal Preparedness Circular: Federal Emergency Management Agency Washington, D.C. 20472 FPC 65Document10 pagesFederal Preparedness Circular: Federal Emergency Management Agency Washington, D.C. 20472 FPC 65Alpha AppsPas encore d'évaluation

- Objectives of Foreign Direct InvestmentDocument6 pagesObjectives of Foreign Direct InvestmentSwati KatariaPas encore d'évaluation

- Leo Marshell - ProfileDocument4 pagesLeo Marshell - ProfilePriya LMAPas encore d'évaluation

- PDRIDocument7 pagesPDRImario5681Pas encore d'évaluation

- ADB - Masato MiyachiDocument40 pagesADB - Masato MiyachiAsian Development BankPas encore d'évaluation

- Philippines Digital Economy Report 2020 A Better Normal Under COVID 19 Digitalizing The Philippine Economy NowDocument134 pagesPhilippines Digital Economy Report 2020 A Better Normal Under COVID 19 Digitalizing The Philippine Economy NowJose Ramon G AlbertPas encore d'évaluation

- SAP For TelecommunicationsDocument12 pagesSAP For TelecommunicationsRino MinerviniPas encore d'évaluation

- Water Resources Development Report - Arizona 2011Document58 pagesWater Resources Development Report - Arizona 2011AlanInAZPas encore d'évaluation

- Immersed Tube Tunnels: Ahmet GursoyDocument2 pagesImmersed Tube Tunnels: Ahmet GursoyNando LtoruanPas encore d'évaluation

- Interlocking Plans & Locking Concepts PDFDocument96 pagesInterlocking Plans & Locking Concepts PDFvaranasilko100% (2)

- ICSE Solutions For Class 8 Geography Voyage - Urbanization - A Plus TopperDocument13 pagesICSE Solutions For Class 8 Geography Voyage - Urbanization - A Plus TopperBinu Kumar S0% (2)

- Dezvoltarea Agriculturii RuraleDocument526 pagesDezvoltarea Agriculturii RuraleVidrascu Anisoara100% (1)

- Blacktown City Council Annual ReportDocument344 pagesBlacktown City Council Annual ReportGeoff HeathPas encore d'évaluation