Vous aimerez peut-être aussi

- 2017 LATBSDC CRITERIA - Final - 06 08 17 PDFDocument72 pages2017 LATBSDC CRITERIA - Final - 06 08 17 PDFRannie IsonPas encore d'évaluation

- Caterpillar Cat 320D Excavator (Prefix KGF) Service Repair Manual (KGF00001 and Up)Document22 pagesCaterpillar Cat 320D Excavator (Prefix KGF) Service Repair Manual (KGF00001 and Up)kfmuseddk100% (1)

- Lit Erar y Devices: Types & DefinitionsDocument47 pagesLit Erar y Devices: Types & DefinitionsImran RafiqPas encore d'évaluation

- Process Costing and Hybrid Product-Costing Systems: Mcgraw-Hill/IrwinDocument44 pagesProcess Costing and Hybrid Product-Costing Systems: Mcgraw-Hill/Irwinsunanda mPas encore d'évaluation

- WPSDocument2 pagesWPSJuli Agus50% (2)

- QAP For Pipes For Hydrant and Sprinkler SystemDocument3 pagesQAP For Pipes For Hydrant and Sprinkler SystemCaspian DattaPas encore d'évaluation

- BMW R 1200 GS 2006 Desmontaje - Montaje CilindrosDocument26 pagesBMW R 1200 GS 2006 Desmontaje - Montaje CilindrosPablo Ezequiel GarciaPas encore d'évaluation

- Cost Management: A Case for Business Process Re-engineeringD'EverandCost Management: A Case for Business Process Re-engineeringPas encore d'évaluation

- Urban Transport Guidelines - Geometric Design of Urban Colloctor RoadsDocument26 pagesUrban Transport Guidelines - Geometric Design of Urban Colloctor RoadsCharl de Reuck100% (1)

- Chapter 7.process Costing - For Students - Part1Document13 pagesChapter 7.process Costing - For Students - Part1DAN NGUYEN THEPas encore d'évaluation

- Hilton 11e Chap004 PPT-STUDocument42 pagesHilton 11e Chap004 PPT-STULạnh LùngPas encore d'évaluation

- Chapter No.04 - Process Costing and Hybrid Product-Costing SystemsDocument39 pagesChapter No.04 - Process Costing and Hybrid Product-Costing SystemsWali NoorzadPas encore d'évaluation

- Chap004, Process CostingDocument17 pagesChap004, Process Costingrief1010Pas encore d'évaluation

- Akb Bab4Document37 pagesAkb Bab4MulyaniPas encore d'évaluation

- Chap4 (E)Document47 pagesChap4 (E)Kiên Lê TrungPas encore d'évaluation

- Chaitra B Chaitra C MDocument28 pagesChaitra B Chaitra C MChaitra MuralidharaPas encore d'évaluation

- Chap004 7e EditedDocument47 pagesChap004 7e EditedfarahPas encore d'évaluation

- Chapter 10 PPT Agm-1Document13 pagesChapter 10 PPT Agm-1Paulina DocenaPas encore d'évaluation

- CHPT 03 HODocument22 pagesCHPT 03 HOKerby Gail RulonaPas encore d'évaluation

- SPPTChap 004Document50 pagesSPPTChap 004QUANG NGUYỄN VINHPas encore d'évaluation

- Process Costing and Hybrid Product-Costing SystemsDocument38 pagesProcess Costing and Hybrid Product-Costing SystemsZia UddinPas encore d'évaluation

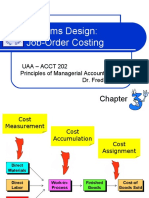

- Systems Design: Job-Order Costing: Uaa - Acct 202 Principles of Managerial Accounting Dr. Fred BarbeeDocument22 pagesSystems Design: Job-Order Costing: Uaa - Acct 202 Principles of Managerial Accounting Dr. Fred BarbeeOrnica BalesPas encore d'évaluation

- Process Costing - Chapter 4Document18 pagesProcess Costing - Chapter 4Asadullahil GalibPas encore d'évaluation

- Analisa Biaya 8 Process CostingDocument74 pagesAnalisa Biaya 8 Process CostingBrian HuangPas encore d'évaluation

- CH 4Document41 pagesCH 4nigoxiy168Pas encore d'évaluation

- Process Cost SystemsDocument48 pagesProcess Cost SystemssajdahwasPas encore d'évaluation

- Hilton Chapter 4 Prerecorded LectureDocument12 pagesHilton Chapter 4 Prerecorded Lecturesunq hccnPas encore d'évaluation

- Systems Design: Process Costing: Mcgraw Hill/IrwinDocument15 pagesSystems Design: Process Costing: Mcgraw Hill/IrwinMarc Jim GregorioPas encore d'évaluation

- Process Costing: Learning ObjectivesDocument23 pagesProcess Costing: Learning ObjectivesChau ToPas encore d'évaluation

- CMA I - Chapter 4, Process CostingDocument68 pagesCMA I - Chapter 4, Process CostingLakachew GetasewPas encore d'évaluation

- ACCY918 T3 2023 Wk3 Process Costing Lecture NoteDocument82 pagesACCY918 T3 2023 Wk3 Process Costing Lecture NoteNIRAJ SharmaPas encore d'évaluation

- Systems Design: Process Costing: Chapter FourDocument78 pagesSystems Design: Process Costing: Chapter FourAyesha FarooqPas encore d'évaluation

- Cost Accumulation System: Defines - Cost Object - Method of Assigning Costs To ProductionDocument4 pagesCost Accumulation System: Defines - Cost Object - Method of Assigning Costs To ProductionKaryl FailmaPas encore d'évaluation

- 2 - MCP1 Chapter 3Document27 pages2 - MCP1 Chapter 3nusratPas encore d'évaluation

- Systems Design: Process Costing: Chapter FourDocument53 pagesSystems Design: Process Costing: Chapter FourFahim RezaPas encore d'évaluation

- Agenda: AF3112 Management Accounting 2Document17 pagesAgenda: AF3112 Management Accounting 2RosePas encore d'évaluation

- AF3112 Management Accounting 2: Process CostingDocument66 pagesAF3112 Management Accounting 2: Process Costing行歌Pas encore d'évaluation

- Hilton Chapter 4 Live Adobe ConnectDocument15 pagesHilton Chapter 4 Live Adobe ConnectJaved ImranPas encore d'évaluation

- SCM L05 ProcessCostingDocument38 pagesSCM L05 ProcessCostinghorace000715Pas encore d'évaluation

- Cost Accounting SystemsDocument4 pagesCost Accounting SystemsEDELYN PoblacionPas encore d'évaluation

- Chapter 10 - Process CostingDocument83 pagesChapter 10 - Process CostingXyne FernandezPas encore d'évaluation

- Managerial Accounting Garrison Noreen Brewer Chapter 04Document76 pagesManagerial Accounting Garrison Noreen Brewer Chapter 041793 Taherul IslamPas encore d'évaluation

- 2 Process Costing w2Document17 pages2 Process Costing w2Angel YungPas encore d'évaluation

- Dokumen - Tips Managerial Accounting Garrison Noreen Brewer Chapter 04Document76 pagesDokumen - Tips Managerial Accounting Garrison Noreen Brewer Chapter 04Arghya BiswasPas encore d'évaluation

- Management Accounting Session 2 Cost Terms & Purposes: Indian Institute of Management RohtakDocument58 pagesManagement Accounting Session 2 Cost Terms & Purposes: Indian Institute of Management RohtakSiddharthPas encore d'évaluation

- Process CostingDocument76 pagesProcess CostingAnonymous Lz2qH7Pas encore d'évaluation

- Lesson 3Document168 pagesLesson 3kirawang098Pas encore d'évaluation

- Systems Design: Job-Order Costing: Managerial Accounting Dr. Fred BarbeeDocument19 pagesSystems Design: Job-Order Costing: Managerial Accounting Dr. Fred BarbeeAbdirazak MohamedPas encore d'évaluation

- Understanding Costs For Management Decisions: Uaa - Acct 650 Seminar in Executive Uses of Accounting Dr. Fred BarbeeDocument92 pagesUnderstanding Costs For Management Decisions: Uaa - Acct 650 Seminar in Executive Uses of Accounting Dr. Fred BarbeeAhmed RazaPas encore d'évaluation

- Hilton Chapter 3 Live Adobe ConnectDocument13 pagesHilton Chapter 3 Live Adobe ConnectaksPas encore d'évaluation

- A WK5 Chp4Document69 pagesA WK5 Chp4Jocelyn LimPas encore d'évaluation

- Job Order Costing: Cost Accounting: Foundations and Evolutions, 8eDocument34 pagesJob Order Costing: Cost Accounting: Foundations and Evolutions, 8eJohann Tetzel DoggzonePas encore d'évaluation

- 4 Process CostingDocument7 pages4 Process CostingKaryl FailmaPas encore d'évaluation

- Ronald Hilton Chapter 3Document25 pagesRonald Hilton Chapter 3Difen L HaradiniPas encore d'évaluation

- (Revised) Week 13 - ReviewDocument94 pages(Revised) Week 13 - ReviewCheuk Ling SoPas encore d'évaluation

- COST ACCOUNTING NOTES & REVIEWER (Finals 1st Sem)Document14 pagesCOST ACCOUNTING NOTES & REVIEWER (Finals 1st Sem)Princess Delos SantosPas encore d'évaluation

- Chap 004Document15 pagesChap 004Ahmad Restu FauziPas encore d'évaluation

- Notes 1Document3 pagesNotes 1Bercasio KelvinPas encore d'évaluation

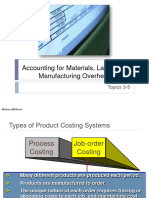

- Topics 3-5Document31 pagesTopics 3-5guloro2001Pas encore d'évaluation

- Process Costing and Hybrid Product-Costing SystemsDocument17 pagesProcess Costing and Hybrid Product-Costing SystemsWailPas encore d'évaluation

- Manac Knowledge Session - Mid TermDocument33 pagesManac Knowledge Session - Mid TermDebaloy DeyPas encore d'évaluation

- Acct Activity Based CostingDocument44 pagesAcct Activity Based CostingTolosa WorkuPas encore d'évaluation

- Cost Terms, Concepts, and Classifications: Uaa - Acct 202 Principles of Managerial Accounting Dr. Fred BarbeeDocument41 pagesCost Terms, Concepts, and Classifications: Uaa - Acct 202 Principles of Managerial Accounting Dr. Fred Barbeekindergarten tutorialPas encore d'évaluation

- Job-Order Costing and Modern Manufacturing PracticesDocument32 pagesJob-Order Costing and Modern Manufacturing PracticesPriyadarshi Saini100% (1)

- Summary Chapter 4Document3 pagesSummary Chapter 4ninarizkitaPas encore d'évaluation

- CH 21Document70 pagesCH 21Shakib Ahmed Emon 0389Pas encore d'évaluation

- Consumer Behavior Case StudyDocument15 pagesConsumer Behavior Case StudyImran Rafiq100% (1)

- Solution Assignment 3wDocument3 pagesSolution Assignment 3wImran RafiqPas encore d'évaluation

- Effect of Television Food Advertisement On Children's Food Purchasing RequestsDocument8 pagesEffect of Television Food Advertisement On Children's Food Purchasing RequestsImran RafiqPas encore d'évaluation

- Sae J3213-2023Document32 pagesSae J3213-20237620383tlPas encore d'évaluation

- TP 5990Document40 pagesTP 5990Roberto Sanchez Zapata100% (1)

- Orbinox Ex PDFDocument2 pagesOrbinox Ex PDFRio PurnamaPas encore d'évaluation

- Bonny 13 EspañolDocument284 pagesBonny 13 EspañolOscar CorderoPas encore d'évaluation

- STP CivilDocument25 pagesSTP CivilRK PROJECT CONSULTANTSPas encore d'évaluation

- Industrial Drive and Application PDFDocument90 pagesIndustrial Drive and Application PDFGOUTHAM A.R coorgPas encore d'évaluation

- 9701 w12 QP 23Document12 pages9701 w12 QP 23poliuytrewqPas encore d'évaluation

- Mvi56e MCMMCMXT Setup GuideDocument78 pagesMvi56e MCMMCMXT Setup GuidepaplusPas encore d'évaluation

- Design Based Comparative Study of Several Condensers Ijariie2142 PDFDocument7 pagesDesign Based Comparative Study of Several Condensers Ijariie2142 PDFFrancePas encore d'évaluation

- Generators Acapp 2nd1718 4Document19 pagesGenerators Acapp 2nd1718 4Anonymous uCjM4Q0% (2)

- Malate + NAD Oxaloacetate + NADH + HDocument14 pagesMalate + NAD Oxaloacetate + NADH + HRonaldPas encore d'évaluation

- Tenant Valve PlusDocument2 pagesTenant Valve Pluspaul coffeyPas encore d'évaluation

- Digital Time StampingDocument22 pagesDigital Time StampingSunil Vicky VohraPas encore d'évaluation

- ML3 USB Adapter 76-50214-02 Instructions: Container RefrigerationDocument24 pagesML3 USB Adapter 76-50214-02 Instructions: Container RefrigerationHussain ShahPas encore d'évaluation

- Bus Switching Scheme PDFDocument6 pagesBus Switching Scheme PDFJAYKUMAR SINGHPas encore d'évaluation

- Evaco 2 FDocument5 pagesEvaco 2 FjnmanivannanPas encore d'évaluation

- Design of Cold Formed Sections by Satish KumarDocument62 pagesDesign of Cold Formed Sections by Satish Kumarspawar1988Pas encore d'évaluation

- Buzzer WT1205Document1 pageBuzzer WT1205Tiago Alves Dos SantosPas encore d'évaluation

- Danfoss Install Operation and Manitenance IOM APP1.5-3.5Document70 pagesDanfoss Install Operation and Manitenance IOM APP1.5-3.5warshipvnPas encore d'évaluation

- Industrial Training ReportDocument19 pagesIndustrial Training ReportRam PandeyPas encore d'évaluation

- An Introduction To Project Logistics Management: ArticleDocument9 pagesAn Introduction To Project Logistics Management: ArticleCh Tushar BhatiPas encore d'évaluation

- Anmlab 67 5451074084 5451074092Document9 pagesAnmlab 67 5451074084 5451074092Quoc Vuong HoangPas encore d'évaluation

- Week 1: Directing and Managing Project ExecutionDocument10 pagesWeek 1: Directing and Managing Project ExecutionAnonymous 4eQB3WZPas encore d'évaluation

- Atmospheric Storage Tanks Venting Req API 2000 (6th ED 2009)Document15 pagesAtmospheric Storage Tanks Venting Req API 2000 (6th ED 2009)HyungTae JangPas encore d'évaluation