Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

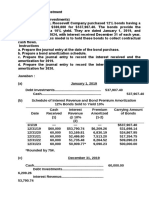

- Chapter 14 Book ValueDocument7 pagesChapter 14 Book ValueThalia Rhine AbertePas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Book Value Per ShareDocument2 pagesBook Value Per ShareShe Rae PalmaPas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Videocon Industries ProjectDocument84 pagesVideocon Industries ProjectPallavi MaliPas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Basic Concepts Capital Budgeting Defined Agency Problem in Capital BudgetingDocument107 pagesBasic Concepts Capital Budgeting Defined Agency Problem in Capital BudgetingKang JoonPas encore d'évaluation

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Chapter-4d Capital GainsDocument15 pagesChapter-4d Capital GainsBrinda RPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Dossier The Finance Club 2020-21 PDFDocument63 pagesDossier The Finance Club 2020-21 PDFKeya HalderPas encore d'évaluation

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Final Examination in Business Combi 2021Document7 pagesFinal Examination in Business Combi 2021Michael BongalontaPas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Case Nike - Cost of Capital Fix 1Document9 pagesCase Nike - Cost of Capital Fix 1Yousania RatuPas encore d'évaluation

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Compustat Users Guide-2003Document735 pagesCompustat Users Guide-2003Gain GainPas encore d'évaluation

- Barth, Beaver & Landsman, 2001Document41 pagesBarth, Beaver & Landsman, 2001Syiera Fella'sPas encore d'évaluation

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Jay Tesla: ExplanationDocument9 pagesJay Tesla: ExplanationJonathan Cheung100% (1)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- On January 1 2016 Aspen Company Acquired 80 Percent ofDocument1 pageOn January 1 2016 Aspen Company Acquired 80 Percent ofAmit PandeyPas encore d'évaluation

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Exemplu Test Examen - BFoctober11qpDocument8 pagesExemplu Test Examen - BFoctober11qpSima RoxanaPas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- PhpobiilxDocument19 pagesPhpobiilxShivansh JaiswalPas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- What Is The Meaning of Book Value Per Share?Document6 pagesWhat Is The Meaning of Book Value Per Share?Emely Grace YanongPas encore d'évaluation

- Admin Service - Asset Management - Furniture and Equipment - Disposal and Write-OffDocument16 pagesAdmin Service - Asset Management - Furniture and Equipment - Disposal and Write-OffBima Perdana PutraPas encore d'évaluation

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Bank Stress Testing A Stochastic Simulation FramewDocument51 pagesBank Stress Testing A Stochastic Simulation FramewmehPas encore d'évaluation

- Cambridge International AS & A Level: ACCOUNTING 9706/23Document20 pagesCambridge International AS & A Level: ACCOUNTING 9706/23Danish MasoodPas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Chapter 3 Review PDFDocument5 pagesChapter 3 Review PDFAisha KhanPas encore d'évaluation

- MODULE 3-Short ProblemsDocument5 pagesMODULE 3-Short ProblemsJaimell LimPas encore d'évaluation

- CASE 2 Suburban Electronics Company Session17Document7 pagesCASE 2 Suburban Electronics Company Session17Hilmi DaffaPas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- On January 1 2017 Procise Corporation Acquired 100 Percent ofDocument1 pageOn January 1 2017 Procise Corporation Acquired 100 Percent ofAmit PandeyPas encore d'évaluation

- Soal Debt InvestmentDocument5 pagesSoal Debt InvestmentKyle Kuro0% (1)

- Expenditure of Last Five YearsDocument7 pagesExpenditure of Last Five YearsPrawin Kumar PrabhakarPas encore d'évaluation

- Corporate Financial Accounting AssignmentsDocument7 pagesCorporate Financial Accounting AssignmentsPooja MauryaPas encore d'évaluation

- ACC121 SEM3 ExamplesDocument12 pagesACC121 SEM3 ExamplesTia1977Pas encore d'évaluation

- Translation of Foreign Currency Financial Statements: Multiple Choice QuestionsDocument154 pagesTranslation of Foreign Currency Financial Statements: Multiple Choice QuestionsMarwa HassanPas encore d'évaluation

- Happyland Market AnalysisDocument31 pagesHappyland Market AnalysisMwaura NdutaPas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Ca Inter Advanced Accounts Imp Questions BookletDocument112 pagesCa Inter Advanced Accounts Imp Questions BookletUdaykiran BheemaganiPas encore d'évaluation

- CHAPTER 8 Caselette - Audit of LiabilitiesDocument27 pagesCHAPTER 8 Caselette - Audit of LiabilitiesNovie Marie Balbin Anit100% (1)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)