Vous aimerez peut-être aussi

- Assignment #1 - 5064Document15 pagesAssignment #1 - 5064ShubhAm UpadhyayPas encore d'évaluation

- Case Study of Costs ConceptDocument21 pagesCase Study of Costs ConceptHosanna AleyePas encore d'évaluation

- Assignment 01Document2 pagesAssignment 01Iftekhar Chowdhury Prince0% (1)

- REXTAR User and Service GuideDocument58 pagesREXTAR User and Service GuidewellsuPas encore d'évaluation

- Nanyang Technological University SEMESTER 2 QUIZ 2019-2020 Ee6508 - Power QualityDocument2 pagesNanyang Technological University SEMESTER 2 QUIZ 2019-2020 Ee6508 - Power QualityYaraPas encore d'évaluation

- Sample Business Report FormatDocument1 pageSample Business Report FormatmironkoprevPas encore d'évaluation

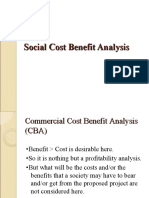

- Social Cost Benefit Analysis Overview About Two Approaches of SCBADocument79 pagesSocial Cost Benefit Analysis Overview About Two Approaches of SCBASunny NischalPas encore d'évaluation

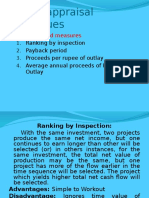

- Project Appraisal SCBADocument15 pagesProject Appraisal SCBAapi-3757629100% (1)

- Discuss The UNIDO Approach of Social-Cost Benefit AnalysisDocument3 pagesDiscuss The UNIDO Approach of Social-Cost Benefit AnalysisAmi Tandon100% (1)

- Unit 5 - Social Cost Benefit AnalysisDocument24 pagesUnit 5 - Social Cost Benefit Analysislamao123Pas encore d'évaluation

- Social Cost Benefit AnalysisDocument67 pagesSocial Cost Benefit Analysisitsmeha100% (1)

- Chapter IVDocument88 pagesChapter IVNesri Yaya100% (1)

- Unit 5Document15 pagesUnit 5Ramesh Thangavel TPas encore d'évaluation

- Agricultural Project Chapter 4Document73 pagesAgricultural Project Chapter 4Milkessa SeyoumPas encore d'évaluation

- Project Appraisal MethodsDocument15 pagesProject Appraisal MethodsAndrew GomezPas encore d'évaluation

- Process CostingDocument20 pagesProcess Costingአረጋዊ ሐይለማርያምPas encore d'évaluation

- International Economics Homework 1 Due On Dec. 16 in Electronic VersionDocument9 pagesInternational Economics Homework 1 Due On Dec. 16 in Electronic VersionAsmita HossainPas encore d'évaluation

- LT 1. Change ManagementDocument71 pagesLT 1. Change Managementፀፀፀፀፀ ከፀፀዘከPas encore d'évaluation

- Econometrics HandoutDocument24 pagesEconometrics Handoutimran khanPas encore d'évaluation

- Agri. Project Planning and Analysis: (Agec522)Document16 pagesAgri. Project Planning and Analysis: (Agec522)wondater Muluneh100% (1)

- The Heckscher-Ohlin Model + Leontief Paradox SummaryDocument2 pagesThe Heckscher-Ohlin Model + Leontief Paradox SummaryAnaPaperina0% (1)

- Financial Anaysis of ProjectDocument48 pagesFinancial Anaysis of ProjectalemayehuPas encore d'évaluation

- ELPDocument44 pagesELPRaghupathi Venkata SujathaPas encore d'évaluation

- Unit - 4 PPMDocument34 pagesUnit - 4 PPMdemeketeme2013Pas encore d'évaluation

- Numericals On National IncomeDocument16 pagesNumericals On National Incomesakchamsinha100% (1)

- 1 Logit Probit and Tobit ModelDocument51 pages1 Logit Probit and Tobit ModelPrabin Ghimire100% (2)

- Fnce 220: Business Finance: Lecture 6: Capital Investment DecisionsDocument39 pagesFnce 220: Business Finance: Lecture 6: Capital Investment DecisionsVincent KamemiaPas encore d'évaluation

- Approaches To Economic Analysis of ProjectsDocument25 pagesApproaches To Economic Analysis of ProjectsRodrick WilbroadPas encore d'évaluation

- Chapter 5Document26 pagesChapter 5Hoàng Phương ThảoPas encore d'évaluation

- Commercial PolicyDocument13 pagesCommercial Policynishantsaini0750% (2)

- Chap1 EconometricsDocument36 pagesChap1 EconometricsLidiya wodajenehPas encore d'évaluation

- Lecture 4Document43 pagesLecture 4decentdawoodPas encore d'évaluation

- Worksheet - 2 Demand & SupplyDocument2 pagesWorksheet - 2 Demand & SupplyPrince SingalPas encore d'évaluation

- U II: T K T D N I: NIT HE Eynesian Heory of Etermination of Ational NcomeDocument56 pagesU II: T K T D N I: NIT HE Eynesian Heory of Etermination of Ational NcomePrateek GoyalPas encore d'évaluation

- Gruber4e ch04Document43 pagesGruber4e ch04Voip KredisiPas encore d'évaluation

- Project Analysis Chapter SixDocument6 pagesProject Analysis Chapter Sixzewdie100% (1)

- Makerere University College of Business and Management Studies Master of Business AdministrationDocument15 pagesMakerere University College of Business and Management Studies Master of Business AdministrationDamulira DavidPas encore d'évaluation

- Qutitative Assignmente 3 AnsewreDocument8 pagesQutitative Assignmente 3 Ansewreabebe amare100% (2)

- EconomicsDocument22 pagesEconomicsVi Pin SinghPas encore d'évaluation

- Net Present Value. Lepton Industries Has A Project With The Following Projected CashDocument1 pageNet Present Value. Lepton Industries Has A Project With The Following Projected CashSharulatha S100% (1)

- Tme 601Document14 pagesTme 601dearsaswatPas encore d'évaluation

- Lecture - 3 - 4 - Determination of Economic ActivityDocument61 pagesLecture - 3 - 4 - Determination of Economic ActivityAnil KingPas encore d'évaluation

- Ridge LinesDocument42 pagesRidge LinesManik Kamboj100% (1)

- Econometrics 1: Dummy Dependent Variables ModelsDocument12 pagesEconometrics 1: Dummy Dependent Variables ModelsHay Jirenyaa0% (1)

- Social Cost Benefit Analysis - PPT 2009Document47 pagesSocial Cost Benefit Analysis - PPT 2009Rahul Jain100% (2)

- Chapter 2 Human CapitalDocument8 pagesChapter 2 Human CapitalkasuPas encore d'évaluation

- Econ Base Vs Input-Output ModelsDocument19 pagesEcon Base Vs Input-Output ModelsNiraj KumarPas encore d'évaluation

- Lecture 10 On Pollution ControlDocument22 pagesLecture 10 On Pollution Controlii muPas encore d'évaluation

- Theory of Comparative AdvantageDocument37 pagesTheory of Comparative AdvantageRohit Kumar100% (1)

- International Product Policy-SlidesDocument12 pagesInternational Product Policy-SlidesRAVINDRA Pr. SHUKLAPas encore d'évaluation

- SpecificFactorsModel LectureSlidesDocument66 pagesSpecificFactorsModel LectureSlidestohox86894Pas encore d'évaluation

- Econ Assignment AnswersDocument4 pagesEcon Assignment AnswersKazımPas encore d'évaluation

- The Theory of Trade and Investment: True/False QuestionsDocument25 pagesThe Theory of Trade and Investment: True/False QuestionsAshok SubramaniamPas encore d'évaluation

- Cost Function NotesDocument7 pagesCost Function Noteschandanpalai91100% (1)

- Aditional Problems MCQ SupplydemandDocument19 pagesAditional Problems MCQ SupplydemandHussein DarwishPas encore d'évaluation

- Tutorial Questions - Solutions: Question OneDocument8 pagesTutorial Questions - Solutions: Question Onephillip quimenPas encore d'évaluation

- Lesson - 04Document24 pagesLesson - 04vineeth.vininandanam.kPas encore d'évaluation

- Questions: Temesgen - Worku@aau - Edu.etDocument3 pagesQuestions: Temesgen - Worku@aau - Edu.etHoney HoneyPas encore d'évaluation

- Change of Origin and ScaleDocument11 pagesChange of Origin and ScaleSanjana PrabhuPas encore d'évaluation

- Techniques of Project Appraisal: An Presentation ONDocument20 pagesTechniques of Project Appraisal: An Presentation ONChandan Lawrence100% (1)

- Classification of CostsDocument28 pagesClassification of CostsDhanya DasPas encore d'évaluation

- Social Cost Benefit Analysis: Prof. Asiya ChaudharyDocument50 pagesSocial Cost Benefit Analysis: Prof. Asiya ChaudharyAgalya GaneshPas encore d'évaluation

- Social Cost Benefit AnalysisDocument44 pagesSocial Cost Benefit AnalysisAnshul ShuklaPas encore d'évaluation

- BSP M-2022-024 s2022 - Rural Bank Strengthening Program) PDFDocument5 pagesBSP M-2022-024 s2022 - Rural Bank Strengthening Program) PDFVictor GalangPas encore d'évaluation

- 09 Quotation For CC Kerb PDFDocument2 pages09 Quotation For CC Kerb PDFD V BHASKARPas encore d'évaluation

- (P1) Modul DC Motor Speed Control SystemDocument13 pages(P1) Modul DC Motor Speed Control SystemTito Bambang Priambodo - 6726Pas encore d'évaluation

- 5 1 5 PDFDocument376 pages5 1 5 PDFSaransh KejriwalPas encore d'évaluation

- Performance of Coffee Farmers Marketing Cooperatives in Yiragcheffe and Wonago Woredas, SNNPRS, Ethiopia PDFDocument166 pagesPerformance of Coffee Farmers Marketing Cooperatives in Yiragcheffe and Wonago Woredas, SNNPRS, Ethiopia PDFesulawyer2001Pas encore d'évaluation

- Blinx01's Ultimate DVD Subbing GuideDocument12 pagesBlinx01's Ultimate DVD Subbing GuideloscanPas encore d'évaluation

- Jcss Probabilistic Modelcode Part 3: Resistance ModelsDocument4 pagesJcss Probabilistic Modelcode Part 3: Resistance Modelsdimitrios25Pas encore d'évaluation

- Schiavi Enc Met Page023Document1 pageSchiavi Enc Met Page023Adel AdelPas encore d'évaluation

- Audit Quality and Audit Firm ReputationDocument10 pagesAudit Quality and Audit Firm ReputationEdosa Joshua AronmwanPas encore d'évaluation

- Louis Vuitton Out Let On Lines LVDocument24 pagesLouis Vuitton Out Let On Lines LVLiu DehuaPas encore d'évaluation

- FIN350 Quiz 2 Monday First Name - Last Name - Version BDocument6 pagesFIN350 Quiz 2 Monday First Name - Last Name - Version BHella Mae RambunayPas encore d'évaluation

- Module 2 - Govt GrantDocument4 pagesModule 2 - Govt GrantLui100% (1)

- What Makes An Event A Mega Event DefinitDocument18 pagesWhat Makes An Event A Mega Event DefinitMoosaPas encore d'évaluation

- Pumper March 2011 IssueDocument108 pagesPumper March 2011 IssuePumper MagazinePas encore d'évaluation

- G11 W8 The Consequences of My ActionsDocument3 pagesG11 W8 The Consequences of My Actionslyka garciaPas encore d'évaluation

- Følstad & Brandtzaeg (2020)Document14 pagesFølstad & Brandtzaeg (2020)Ijlal Shidqi Al KindiPas encore d'évaluation

- Q8-Auto-JK - en PDSDocument1 pageQ8-Auto-JK - en PDSagnovPas encore d'évaluation

- SLC Motor Oil Series 1Document8 pagesSLC Motor Oil Series 1Anonymous QE8o0gjPas encore d'évaluation

- Maximum Equivalent Stress Safety ToolDocument2 pagesMaximum Equivalent Stress Safety ToolDonfack BertrandPas encore d'évaluation

- Ministry of PowerDocument4 pagesMinistry of PowerVivek KumarPas encore d'évaluation

- Huawei CX311 Switch Module V100R001C00 White Paper 09Document41 pagesHuawei CX311 Switch Module V100R001C00 White Paper 09zain_zedanPas encore d'évaluation

- A Himalayan Challenge PDFDocument39 pagesA Himalayan Challenge PDFAdheesh TelangPas encore d'évaluation

- CH03-The Relational ModelDocument54 pagesCH03-The Relational Modelمحمود سمورPas encore d'évaluation

- Dfsan AbilistDocument64 pagesDfsan AbilistTorPas encore d'évaluation

- Carrigan ResumeDocument2 pagesCarrigan ResumeeacarriPas encore d'évaluation

- Production of Phenol Via Chlorobenzene and Caustic ProcessDocument1 pageProduction of Phenol Via Chlorobenzene and Caustic ProcessPatricia MirandaPas encore d'évaluation

- DE2 115 User Manual PDFDocument118 pagesDE2 115 User Manual PDFUFABCRAFAPas encore d'évaluation