Vous aimerez peut-être aussi

- AS Economics - 11 - The Price System and The Micro Economy (Consumer & Producer Surplus)Document181 pagesAS Economics - 11 - The Price System and The Micro Economy (Consumer & Producer Surplus)Damion BrusselPas encore d'évaluation

- MacroEconomics - MultiplierDocument38 pagesMacroEconomics - MultiplierPranay KarthikPas encore d'évaluation

- Relevance of Keynesian Theory To The Current EconomicDocument15 pagesRelevance of Keynesian Theory To The Current EconomicSiva Krishna Reddy NallamilliPas encore d'évaluation

- Chapter 1Document6 pagesChapter 1zelalem wegayehuPas encore d'évaluation

- Welfare EconomicsDocument4 pagesWelfare EconomicsManish KumarPas encore d'évaluation

- Module 7 - Inflation & UnemploymentDocument51 pagesModule 7 - Inflation & UnemploymentPrashasti100% (1)

- Lecture 5 - Growth and ProductivityDocument54 pagesLecture 5 - Growth and ProductivityAli Ali100% (1)

- Micro & Macro EconomicsDocument8 pagesMicro & Macro Economicsadnantariq_2004100% (1)

- Chapter 2-Scarcity, Choice and Opportunity CostDocument32 pagesChapter 2-Scarcity, Choice and Opportunity CostNuriIzzatiPas encore d'évaluation

- Prepared by Iordanis Petsas To Accompany by Paul R. Krugman and Maurice ObstfeldDocument39 pagesPrepared by Iordanis Petsas To Accompany by Paul R. Krugman and Maurice ObstfeldNazish GulzarPas encore d'évaluation

- BBEK4203 Principles of Macroeconomics CDocument269 pagesBBEK4203 Principles of Macroeconomics CHaziq Zulkefly100% (1)

- T2 Public GoodsDocument101 pagesT2 Public GoodsEstella ManeaPas encore d'évaluation

- Chapter 3 Money and Monetary PolicyDocument35 pagesChapter 3 Money and Monetary PolicyZaid Harithah100% (1)

- Inflation: Definition, Causes, Measurement, Consequences and Corrective ActionsDocument47 pagesInflation: Definition, Causes, Measurement, Consequences and Corrective ActionsJagveer GandhiPas encore d'évaluation

- Income Elasticity of Demand: InterpretationDocument10 pagesIncome Elasticity of Demand: Interpretationabhijeet9981Pas encore d'évaluation

- CH 1 - Introduction MicroeconomicsDocument45 pagesCH 1 - Introduction MicroeconomicsAchmad TriantoPas encore d'évaluation

- Foreign Aid and Foreign InvestmentDocument16 pagesForeign Aid and Foreign InvestmentKumkum SultanaPas encore d'évaluation

- OLIGOPOLYDocument31 pagesOLIGOPOLYMark Lorence Dihayco100% (1)

- Chapter 3 Classic Theories of Economic Growth and DevelopmentDocument4 pagesChapter 3 Classic Theories of Economic Growth and DevelopmentStephany GrailPas encore d'évaluation

- DPB 1023 Microeconomics: Lecturer: Suzana Binti IthnainDocument23 pagesDPB 1023 Microeconomics: Lecturer: Suzana Binti Ithnainhxzyrxh hxzyqxh100% (1)

- SpecificFactorsModel LectureSlidesDocument66 pagesSpecificFactorsModel LectureSlidestohox86894Pas encore d'évaluation

- Elasticity and Its ApplicationDocument55 pagesElasticity and Its ApplicationMarcella Alifia Kuswana Putri100% (1)

- ECO 415 CH 1 IntroDocument22 pagesECO 415 CH 1 IntroMohd ZaidPas encore d'évaluation

- Chapter 6 - Cost of ProductionDocument29 pagesChapter 6 - Cost of ProductionArup SahaPas encore d'évaluation

- The Macro-Economic Performance of Bangladesh (2008-2013)Document14 pagesThe Macro-Economic Performance of Bangladesh (2008-2013)gunners888Pas encore d'évaluation

- 10 Principles of EconomicsDocument3 pages10 Principles of EconomicsArlette MovsesyanPas encore d'évaluation

- Economics Midterm ReviewerDocument9 pagesEconomics Midterm ReviewerAr-ar RealuyoPas encore d'évaluation

- Household Behavior Consumer ChoiceDocument40 pagesHousehold Behavior Consumer ChoiceRAYMUND JOHN ROSARIOPas encore d'évaluation

- Topic Two The Price System and The MicroeconomyDocument25 pagesTopic Two The Price System and The MicroeconomyRashid okeyoPas encore d'évaluation

- Monetary & Fiscal PolicyDocument10 pagesMonetary & Fiscal PolicyManavazhaganPas encore d'évaluation

- Costs of UnemploymentDocument15 pagesCosts of UnemploymentNandy Raghoo GopaulPas encore d'évaluation

- Chapter 1 Page 25Document25 pagesChapter 1 Page 25Sangheethaa SukumaranPas encore d'évaluation

- A Note On Welfare Propositions in EconomicsDocument13 pagesA Note On Welfare Propositions in EconomicsmkatsotisPas encore d'évaluation

- Modern Theory of RentDocument8 pagesModern Theory of RentKajal VermaPas encore d'évaluation

- Lesson 1&2 - Economics PDFDocument7 pagesLesson 1&2 - Economics PDFTrixie CabotagePas encore d'évaluation

- Economic Challenges Facing Global and Domestic Business: Learn Ing G OalsDocument15 pagesEconomic Challenges Facing Global and Domestic Business: Learn Ing G Oalsgarimasoni89497Pas encore d'évaluation

- Rural and Urban Development MeaningDocument13 pagesRural and Urban Development Meaningteddy jr AnfonePas encore d'évaluation

- Lecture 03 - Elasticity of Demand and SupplyDocument60 pagesLecture 03 - Elasticity of Demand and SupplyTanveer Khan100% (1)

- Theory of Consumer Choice - Lecture 3Document10 pagesTheory of Consumer Choice - Lecture 3Sharanya RajeshPas encore d'évaluation

- OligopolyDocument34 pagesOligopolySaya Augustin100% (1)

- Shift-Share AnalysisDocument24 pagesShift-Share AnalysisHesekiel Butar-butarPas encore d'évaluation

- Oligopoly (Kinked Demand Curve) 2007Document22 pagesOligopoly (Kinked Demand Curve) 2007PankajBhadana100% (1)

- Microeconomy (Paper) PDFDocument125 pagesMicroeconomy (Paper) PDFxavierjosephPas encore d'évaluation

- Individual & Market DemandDocument12 pagesIndividual & Market DemandAkshay ModakPas encore d'évaluation

- Conduct of Monetary Policy Goal and TargetsDocument12 pagesConduct of Monetary Policy Goal and TargetsSumra KhanPas encore d'évaluation

- Revision - Classical and KeynesianDocument29 pagesRevision - Classical and KeynesianMsKhan0078Pas encore d'évaluation

- Chapter 1 Ten Principles of EconomicsDocument29 pagesChapter 1 Ten Principles of EconomicsSharon YuPas encore d'évaluation

- Sem 3 - Intermediate-Macroeconomics - Part 1Document4 pagesSem 3 - Intermediate-Macroeconomics - Part 1Maverick SinghPas encore d'évaluation

- McEachern11e - Ch1-The Art and Science of Economic AnalysisDocument53 pagesMcEachern11e - Ch1-The Art and Science of Economic AnalysisLilith GhazaryanPas encore d'évaluation

- Chapter # 6: Multiple Regression Analysis: The Problem of EstimationDocument43 pagesChapter # 6: Multiple Regression Analysis: The Problem of EstimationRas DawitPas encore d'évaluation

- WEEK3 LESSON 4 Production FunctionDocument4 pagesWEEK3 LESSON 4 Production FunctionSixd WazninePas encore d'évaluation

- Marginal Benefit and Marginal CostDocument4 pagesMarginal Benefit and Marginal CostAmina Akther Mim 1821179649Pas encore d'évaluation

- Ricardian or Classical Theory of Income DistributionDocument15 pagesRicardian or Classical Theory of Income DistributionketanPas encore d'évaluation

- Economics Midterm ReviewDocument5 pagesEconomics Midterm ReviewAmyPas encore d'évaluation

- CIE Igcse E (0455) : ConomicsDocument15 pagesCIE Igcse E (0455) : ConomicsChutiaPas encore d'évaluation

- Economics: Measuring The Cost of LivingDocument21 pagesEconomics: Measuring The Cost of LivingHanPas encore d'évaluation

- Mixed EconomyDocument13 pagesMixed Economyjr_bergPas encore d'évaluation

- FMS Trade Theories PPT 1Document501 pagesFMS Trade Theories PPT 1Abhi Singh100% (1)

- Microeconomics: by Robert S. Pindyck Daniel Rubinfeld Ninth EditionDocument51 pagesMicroeconomics: by Robert S. Pindyck Daniel Rubinfeld Ninth EditionClaytonMitchellJr.Pas encore d'évaluation

- C06 Krugman 11e PDFDocument63 pagesC06 Krugman 11e PDFYUJIA HUPas encore d'évaluation

- Week 1 Lecture and Seminar SlidesDocument8 pagesWeek 1 Lecture and Seminar SlidesShahidUmarPas encore d'évaluation

- Database Recovery TechniquesDocument41 pagesDatabase Recovery TechniquesShahidUmarPas encore d'évaluation

- CW1 Assignment FY027 BriefDocument3 pagesCW1 Assignment FY027 BriefShahidUmar50% (2)

- Chapter 11Document19 pagesChapter 11ShahidUmarPas encore d'évaluation

- Human Resource Development Center Institute of Management Sciences Peshawar Paid Internship OpportunityDocument1 pageHuman Resource Development Center Institute of Management Sciences Peshawar Paid Internship OpportunityShahidUmarPas encore d'évaluation

- ElasticityDocument51 pagesElasticityShahidUmar100% (1)

- Short NotesDocument17 pagesShort NotesShahidUmarPas encore d'évaluation

- BCS TopicDocument66 pagesBCS TopicShahidUmarPas encore d'évaluation

- Assigement 1Document11 pagesAssigement 1ShahidUmarPas encore d'évaluation

- List of Countries in The World With Their CapitalsDocument3 pagesList of Countries in The World With Their CapitalsShahidUmar0% (1)

- National Education Policy 2009Document12 pagesNational Education Policy 2009ShahidUmarPas encore d'évaluation

- National Educational Policy 2009: Submitted To: Dr. Muhammad Amin Submitted By: Sahar Fatima M.phill ELPSDocument12 pagesNational Educational Policy 2009: Submitted To: Dr. Muhammad Amin Submitted By: Sahar Fatima M.phill ELPSShahidUmarPas encore d'évaluation

- An Overview of Policy Design Origins, Process and Design ItselfDocument41 pagesAn Overview of Policy Design Origins, Process and Design ItselfShahidUmar100% (1)

- Price Elasticity of GoldDocument18 pagesPrice Elasticity of Goldpaps3535_2955544267% (3)

- Bcoc 134 2022-23Document14 pagesBcoc 134 2022-23icaibosinterPas encore d'évaluation

- Sosial Sciences 2012 PDFDocument14 pagesSosial Sciences 2012 PDFNugiPas encore d'évaluation

- EC205 Mathematics For Economics and Business: The Straight Line and Applications IIDocument3 pagesEC205 Mathematics For Economics and Business: The Straight Line and Applications IIperePas encore d'évaluation

- Cover Page / Title / Your Name / Date Etc Etc.: DeletedDocument3 pagesCover Page / Title / Your Name / Date Etc Etc.: Deletedgauri kanodiaPas encore d'évaluation

- Applied EconomicsDocument39 pagesApplied EconomicsDwights Christian50% (2)

- Engineering Structures: Melina Bosco, Giovanna A.F. Ferrara, Aurelio Ghersi, Edoardo M. Marino, Pier Paolo RossiDocument15 pagesEngineering Structures: Melina Bosco, Giovanna A.F. Ferrara, Aurelio Ghersi, Edoardo M. Marino, Pier Paolo RossimohamedPas encore d'évaluation

- Microeconomics Exam 2Document10 pagesMicroeconomics Exam 2Robin SminesPas encore d'évaluation

- BBA Program Syllabus 2012Document65 pagesBBA Program Syllabus 2012Biju Kumar ThapaliaPas encore d'évaluation

- 3 Mundlak Cavallo y Domenech 1990Document25 pages3 Mundlak Cavallo y Domenech 1990Candela Vazquez FernándezPas encore d'évaluation

- The Impact of Fertilizer Subsidy On Paddy Cultivation in Sri LankaDocument24 pagesThe Impact of Fertilizer Subsidy On Paddy Cultivation in Sri LankaKenneth Alain GabitoPas encore d'évaluation

- 4.bachelor of Arts - EconomicsDocument46 pages4.bachelor of Arts - EconomicsGjPas encore d'évaluation

- In This Chapter We Ve Emphasized That The Elasticity of SupplyDocument1 pageIn This Chapter We Ve Emphasized That The Elasticity of Supplytrilocksp SinghPas encore d'évaluation

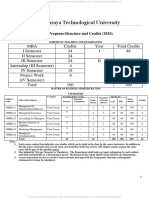

- VTU MBA Scheme and Syllabus WEF 2018-19Document141 pagesVTU MBA Scheme and Syllabus WEF 2018-19MANORANJAN M SPas encore d'évaluation

- Chapter 5 PowerPointDocument58 pagesChapter 5 PowerPointArturoPas encore d'évaluation

- Q HatDocument3 pagesQ Hatthanhpham0505Pas encore d'évaluation

- Arc ElasticityDocument5 pagesArc ElasticityAliNoorPas encore d'évaluation

- CHAPTER 5 - Basics of Demand and SupplyDocument73 pagesCHAPTER 5 - Basics of Demand and Supplyancaye1962Pas encore d'évaluation

- India's Petroleum Demand: Empirical Estimations and Projections For The FutureDocument30 pagesIndia's Petroleum Demand: Empirical Estimations and Projections For The FutureSantosh creationsPas encore d'évaluation

- S.4 - Chapter 9-10 - MC - Demand and SupplyDocument39 pagesS.4 - Chapter 9-10 - MC - Demand and SupplyLam GracePas encore d'évaluation

- Handouts and QuestionsDocument138 pagesHandouts and QuestionsJay Villegas ArmeroPas encore d'évaluation

- Unit 2 The Allocation of Resources: How The Market Works Market FailureDocument12 pagesUnit 2 The Allocation of Resources: How The Market Works Market FailureJada CameronPas encore d'évaluation

- ICFAI University Previous Years Question Paper 4Document24 pagesICFAI University Previous Years Question Paper 4Ashish GohilPas encore d'évaluation

- Caie Igcse Economics 0455 Theory v1Document16 pagesCaie Igcse Economics 0455 Theory v1Mehri MustafayevaPas encore d'évaluation

- MULTIPLE CHOICE QUESTIONS Mankiw 7th 1Document10 pagesMULTIPLE CHOICE QUESTIONS Mankiw 7th 1Mỹ HoàiPas encore d'évaluation

- BS Development Studies - Department of Economics-AWKUMDocument160 pagesBS Development Studies - Department of Economics-AWKUMShehzad RahmanPas encore d'évaluation

- Impact of Agriculture Subsidies On Productivity of Major Crops in Pakistan and India A Case Study of Fertilizer SubsidyDocument72 pagesImpact of Agriculture Subsidies On Productivity of Major Crops in Pakistan and India A Case Study of Fertilizer SubsidySamar RanaPas encore d'évaluation

- The Discounting PrincipleDocument2 pagesThe Discounting PrinciplesommelierPas encore d'évaluation

- Applied Economics For Students Only NewDocument51 pagesApplied Economics For Students Only NewAna Rose S. LlameraPas encore d'évaluation

- Consumer Choice and Elasticity: Full Length Text - Micro Only TextDocument35 pagesConsumer Choice and Elasticity: Full Length Text - Micro Only TextGvantsa MorchadzePas encore d'évaluation