Vous aimerez peut-être aussi

- Colorscope 1Document6 pagesColorscope 1Andrew NeuberPas encore d'évaluation

- Case1 Colorscope Solution PPTXDocument42 pagesCase1 Colorscope Solution PPTXAmit Dixit100% (1)

- Management 122 Course XXXXZAXReader - Rev J - SolutionsDocument43 pagesManagement 122 Course XXXXZAXReader - Rev J - SolutionsWOw WongPas encore d'évaluation

- Color ScopeDocument10 pagesColor Scopedharti_thakare100% (1)

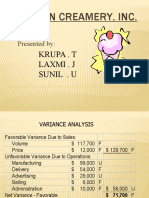

- Boston Creamery Variance Analysis Reveals $71K Profit GainDocument9 pagesBoston Creamery Variance Analysis Reveals $71K Profit GainwahyuPas encore d'évaluation

- Case Case:: Colorscope, Colorscope, Inc. IncDocument4 pagesCase Case:: Colorscope, Colorscope, Inc. IncBalvinder SinghPas encore d'évaluation

- Case Analysis of Colorscope, Inc.: Cost and Management AccountingDocument14 pagesCase Analysis of Colorscope, Inc.: Cost and Management AccountingRaghav SPas encore d'évaluation

- Wilkerson Company Break Even Analysis for Multi-product SituationDocument5 pagesWilkerson Company Break Even Analysis for Multi-product SituationYAKSH DODIAPas encore d'évaluation

- 05 Wilkerson Company Solution - StudentsDocument9 pages05 Wilkerson Company Solution - StudentsVinyabhooshan Bajpai PGP 2022-24 Batch100% (1)

- Analysis of PolysarDocument84 pagesAnalysis of PolysarParthMairPas encore d'évaluation

- This Study Resource Was: Forner CarpetDocument4 pagesThis Study Resource Was: Forner CarpetLi CarinaPas encore d'évaluation

- Vyaderm Caseanalysis PDFDocument6 pagesVyaderm Caseanalysis PDFSahil Azher RashidPas encore d'évaluation

- Case - 2 - Kalamazoo - Zoo SolutionDocument27 pagesCase - 2 - Kalamazoo - Zoo SolutionAnandPas encore d'évaluation

- Colorscope IncDocument14 pagesColorscope IncShashi ShekharPas encore d'évaluation

- LIFO vs FIFO Impact on Merrimack TractorsDocument3 pagesLIFO vs FIFO Impact on Merrimack TractorsstudvabzPas encore d'évaluation

- Software Asssociates11Document13 pagesSoftware Asssociates11Arslan ShaikhPas encore d'évaluation

- Case ReichardDocument23 pagesCase ReichardDesiSelviaPas encore d'évaluation

- Does IT Payoff Strategies of Two Banking GiantsDocument10 pagesDoes IT Payoff Strategies of Two Banking GiantsScyfer_16031991Pas encore d'évaluation

- Shimano 3Document14 pagesShimano 3Tigist AlemayehuPas encore d'évaluation

- PIA Breakeven Analysis and Financial Performance ReportDocument3 pagesPIA Breakeven Analysis and Financial Performance ReportsaadsahilPas encore d'évaluation

- Case Study Beta Management Company: Raman Dhiman Indian Institute of Management (Iim), ShillongDocument8 pagesCase Study Beta Management Company: Raman Dhiman Indian Institute of Management (Iim), ShillongFabián Fuentes100% (1)

- Johnson BeverageDocument6 pagesJohnson BeverageShouib Mehreyar100% (1)

- Cafe Monte BiancoDocument21 pagesCafe Monte BiancoWilliam Torrez OrozcoPas encore d'évaluation

- Seligram, IncDocument5 pagesSeligram, IncAto SumartoPas encore d'évaluation

- Sun Microsystems Financials and ValuationDocument6 pagesSun Microsystems Financials and ValuationJasdeep SinghPas encore d'évaluation

- 05 Lilac Flour MillsDocument6 pages05 Lilac Flour Millsspaw1108Pas encore d'évaluation

- Vyaderm CaseanalysisDocument6 pagesVyaderm CaseanalysisArvind Gupta100% (1)

- Boston Creamery CaseDocument9 pagesBoston Creamery Caselion_heart3001100% (1)

- Guideline ICE1 TextOnlyDocument4 pagesGuideline ICE1 TextOnlyRima AkidPas encore d'évaluation

- Economic Impact of Oakland Athletics Ballpark at Howard TerminalDocument13 pagesEconomic Impact of Oakland Athletics Ballpark at Howard TerminalZennie AbrahamPas encore d'évaluation

- Mystic SportsDocument34 pagesMystic SportshelloPas encore d'évaluation

- Sneaker Excel Sheet For Risk AnalysisDocument11 pagesSneaker Excel Sheet For Risk AnalysisSuperGuyPas encore d'évaluation

- Colorscope IncDocument1 pageColorscope IncsanPas encore d'évaluation

- Cell Name Original Value Final ValueDocument7 pagesCell Name Original Value Final ValuedebojyotiPas encore d'évaluation

- Costing Systems Reveal True Product MarginsDocument1 pageCosting Systems Reveal True Product Marginsfelipevwa100% (1)

- Sharing Sheet Hallstead JewelersDocument11 pagesSharing Sheet Hallstead JewelersHarpreet SinghPas encore d'évaluation

- Unitron CorporationDocument7 pagesUnitron CorporationERika PratiwiPas encore d'évaluation

- Case1 Nett Colorscope SaddamrobertobinuDocument10 pagesCase1 Nett Colorscope SaddamrobertobinucicishintyaPas encore d'évaluation

- MANAGEMENT ACCOUNTING - IIDocument5 pagesMANAGEMENT ACCOUNTING - IIshshank pandeyPas encore d'évaluation

- Davey Brothers Watch Co. and Classic Pen Company Case AnalysisDocument4 pagesDavey Brothers Watch Co. and Classic Pen Company Case Analysisabhishek pattanayakPas encore d'évaluation

- Cost Volume ProfitDocument15 pagesCost Volume Profitprashant0071988Pas encore d'évaluation

- DHL ExhibitsDocument7 pagesDHL ExhibitsAlan SamPas encore d'évaluation

- Hallstead Jewelers Breakeven AnalysisDocument7 pagesHallstead Jewelers Breakeven Analysisanon_839867152Pas encore d'évaluation

- VyaddermDocument25 pagesVyaddermJamie StevensPas encore d'évaluation

- SCM - Managing Uncertainty in DemandDocument27 pagesSCM - Managing Uncertainty in DemandHari Madhavan Krishna KumarPas encore d'évaluation

- Beta Management QuestionsDocument1 pageBeta Management QuestionsbjhhjPas encore d'évaluation

- 4 - Terminus Hotel - ADocument5 pages4 - Terminus Hotel - AAnonymous 2EdAmT96Hh0% (5)

- Kamoki Poultry FeedsDocument2 pagesKamoki Poultry Feedssidra imtiazPas encore d'évaluation

- Miles High Cycles Katherine Roland and John ConnorsDocument4 pagesMiles High Cycles Katherine Roland and John ConnorsvivekPas encore d'évaluation

- Titanium Dioxide and Super Project Prof. Joshy JacobDocument3 pagesTitanium Dioxide and Super Project Prof. Joshy JacobSIDDHARTH SINGHPas encore d'évaluation

- Hospital SupplyDocument3 pagesHospital SupplyKate BurgosPas encore d'évaluation

- Sun Brewing Case ExhibitsDocument26 pagesSun Brewing Case ExhibitsShshankPas encore d'évaluation

- ZomatoDocument56 pagesZomatopreethishPas encore d'évaluation

- Bridgeton Industries Case Study Analysis of Overhead AllocationDocument3 pagesBridgeton Industries Case Study Analysis of Overhead Allocationzxcv3214100% (1)

- Report 2Document4 pagesReport 2Trang PhamPas encore d'évaluation

- Color ScopeDocument12 pagesColor Scopeprincemech2004100% (1)

- Analyze manufacturing costs and variances for Marston, IncDocument11 pagesAnalyze manufacturing costs and variances for Marston, IncCharles GohPas encore d'évaluation

- 1) How Could Colposcope INC Improve Its Operations?Document2 pages1) How Could Colposcope INC Improve Its Operations?Nitu Pathak100% (1)

- Ca Inter Cost Management Accounting Test 2 Unscheduled Solution 598020012022Document14 pagesCa Inter Cost Management Accounting Test 2 Unscheduled Solution 598020012022Deppanshu KhandelwalPas encore d'évaluation

- Download slides, ebook, solutions and test bankDocument2 pagesDownload slides, ebook, solutions and test bankdindaPas encore d'évaluation

- Nivea Final PPT Group 2Document14 pagesNivea Final PPT Group 2Rajneesh100% (1)

- Group2 BloomexDocument9 pagesGroup2 BloomexRajneesh100% (1)

- Bloomex.ca Logistics Optimization Case SolutionDocument7 pagesBloomex.ca Logistics Optimization Case SolutionRajneesh100% (1)

- Colorscope, IncDocument16 pagesColorscope, IncRajneeshPas encore d'évaluation

- Hidesign Marketing - FinalDocument10 pagesHidesign Marketing - FinalRajneeshPas encore d'évaluation

- Course Lecture Notes For Cumulative Final Exam (Combined Weeks 1-10)Document178 pagesCourse Lecture Notes For Cumulative Final Exam (Combined Weeks 1-10)James CrombezPas encore d'évaluation

- SAP MM OverviewDocument113 pagesSAP MM OverviewPatil MGPas encore d'évaluation

- RevenueDocument5 pagesRevenueTanya AroraPas encore d'évaluation

- AcknowledgementDocument21 pagesAcknowledgementifrah17100% (1)

- B G ShirkeDocument15 pagesB G ShirkeAbu AbuPas encore d'évaluation

- Analyzing Uber's Profitability with Porter's Five ForcesDocument2 pagesAnalyzing Uber's Profitability with Porter's Five ForcesMikey ChuaPas encore d'évaluation

- 2018 July 20 CME Advanced Gap TechniquesDocument19 pages2018 July 20 CME Advanced Gap TechniquesVinicius FreitasPas encore d'évaluation

- BIR Ruling 98-97Document1 pageBIR Ruling 98-97Kenneth BuriPas encore d'évaluation

- 1Document8 pages1Hung DaoPas encore d'évaluation

- Cuadernillo IV Parcial Quinto Grado 2022Document1 pageCuadernillo IV Parcial Quinto Grado 2022tumbalacasamami5365Pas encore d'évaluation

- Vendor Instructions for Equipment PricingDocument26 pagesVendor Instructions for Equipment PricingFERNANDO FERRUSCAPas encore d'évaluation

- Quiz 3 SolutionsDocument6 pagesQuiz 3 SolutionsNgsPas encore d'évaluation

- Cable Industry in Indonesia PDFDocument85 pagesCable Industry in Indonesia PDFlinggaraninditaPas encore d'évaluation

- Biotech Sunglasses Break-Even AnalysisDocument8 pagesBiotech Sunglasses Break-Even AnalysisKuralay TilegenPas encore d'évaluation

- Marketing Rakura TeaDocument19 pagesMarketing Rakura TeaAnonymous G5ScwB50% (2)

- Oil Refineries (USA, Canada, Mexico)Document10 pagesOil Refineries (USA, Canada, Mexico)Margaret Carney100% (1)

- Chap 011Document5 pagesChap 011dt830280% (5)

- AaaaaDocument70 pagesAaaaaRamona Ana100% (1)

- Trial Balance December 2016Document1 pageTrial Balance December 2016Faie RifaiPas encore d'évaluation

- Activity Based ManagementDocument75 pagesActivity Based ManagementDonna KeePas encore d'évaluation

- Cost Sheet: Dr. Shubhendu VimalDocument9 pagesCost Sheet: Dr. Shubhendu VimalSnehil KrPas encore d'évaluation

- SIBM Bangalore Retail ManagementDocument4 pagesSIBM Bangalore Retail ManagementPrateek AryaPas encore d'évaluation

- Tutor 2 (Cost, Volume, Profit Analysis)Document2 pagesTutor 2 (Cost, Volume, Profit Analysis)aulia100% (1)

- EconomicsDocument107 pagesEconomicsWala LangPas encore d'évaluation

- Bunyan Lumber Harvest AnalysisDocument8 pagesBunyan Lumber Harvest AnalysisDinh JamiePas encore d'évaluation

- Economics of Strategy 6Th Edition PDF Full ChapterDocument41 pagesEconomics of Strategy 6Th Edition PDF Full Chapterrosa.green630100% (27)

- CGB Sample TestDocument4 pagesCGB Sample TestMuhammad Zubair SharifPas encore d'évaluation

- Phiếu Giao Bài Tập Số 3Document3 pagesPhiếu Giao Bài Tập Số 3Phạm Thị Thúy HằngPas encore d'évaluation

- ACTG22a Midterm B 1Document5 pagesACTG22a Midterm B 1Kimberly RojasPas encore d'évaluation

- CLSAU Mining0615Document40 pagesCLSAU Mining0615pokygangPas encore d'évaluation