Vous aimerez peut-être aussi

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- F4E-QA-102 Supplier Audit Implementation 296E7T v2 3Document18 pagesF4E-QA-102 Supplier Audit Implementation 296E7T v2 3Jai BhandariPas encore d'évaluation

- The Environmental Audit Report (External Audit)Document3 pagesThe Environmental Audit Report (External Audit)Sheyyan TanPas encore d'évaluation

- Midterms Se11 Answer KeyDocument5 pagesMidterms Se11 Answer KeyALYZA ANGELA ORNEDO100% (1)

- CFAS - Module 1 PDFDocument22 pagesCFAS - Module 1 PDFKashato BabyPas encore d'évaluation

- Air PollutionDocument1 pageAir PollutionJyle ManiagoPas encore d'évaluation

- Brief Description of The "My Tree Parenting Project"Document3 pagesBrief Description of The "My Tree Parenting Project"Jyle ManiagoPas encore d'évaluation

- Orca Share Media1582508437215Document6 pagesOrca Share Media1582508437215Jyle ManiagoPas encore d'évaluation

- RESPT2LITERATUREDocument14 pagesRESPT2LITERATUREJyle Maniago0% (1)

- Queen Esther - Bible StoryDocument13 pagesQueen Esther - Bible StoryJyle ManiagoPas encore d'évaluation

- CH1. FUNDAMENTALS OF AUDITING AND ASSURANCE SERVICES pt2 2Document17 pagesCH1. FUNDAMENTALS OF AUDITING AND ASSURANCE SERVICES pt2 2Jyle ManiagoPas encore d'évaluation

- Audit MCQ PDFDocument100 pagesAudit MCQ PDFFentorPas encore d'évaluation

- Introduction To Financial Accounting I: ACC203 Course GuideDocument171 pagesIntroduction To Financial Accounting I: ACC203 Course GuideAllsmart NgPas encore d'évaluation

- The Audit of Financial Statements SA 200ADocument2 pagesThe Audit of Financial Statements SA 200AAmit SaxenaPas encore d'évaluation

- Issai 1705Document6 pagesIssai 1705fhreankPas encore d'évaluation

- Isa 265Document9 pagesIsa 265baabasaamPas encore d'évaluation

- Auditing Expense CycleDocument1 pageAuditing Expense CycleMelvin Jan SujedePas encore d'évaluation

- Germany SpainDocument18 pagesGermany SpainsriramPas encore d'évaluation

- Stat Audit ChecklistDocument2 pagesStat Audit ChecklistMksreekanthMkPas encore d'évaluation

- Financial Crime Dissertation TopicsDocument4 pagesFinancial Crime Dissertation TopicsWriteMyPaperApaFormatCanada100% (1)

- MD Sajjad AnsariDocument2 pagesMD Sajjad AnsariMd sajjad afzalPas encore d'évaluation

- Formatted Brgy. FormsDocument21 pagesFormatted Brgy. FormsBarangay CambaroPas encore d'évaluation

- Sihs-Question Bank For A'levelDocument21 pagesSihs-Question Bank For A'levelDickson MukunziPas encore d'évaluation

- Topic 7 Introduction To Public Sector BudgetingDocument5 pagesTopic 7 Introduction To Public Sector BudgetingShumbusho Consultingtz100% (1)

- Critical Anlaysis of Clause 49 0F Listing AgreementDocument37 pagesCritical Anlaysis of Clause 49 0F Listing AgreementRohit DongrePas encore d'évaluation

- GHTF Sg3 n19 2012 Nonconformity Grading 121102Document16 pagesGHTF Sg3 n19 2012 Nonconformity Grading 121102chit catPas encore d'évaluation

- 201702fraud Responsibility MatrixDocument4 pages201702fraud Responsibility MatrixChinh Lê ĐìnhPas encore d'évaluation

- Basic Accounting - BokDocument6 pagesBasic Accounting - BokCastigador Batul PhoenixPas encore d'évaluation

- PADMALIFE-Annual Report - 2017Document74 pagesPADMALIFE-Annual Report - 2017Saram ShahPas encore d'évaluation

- Irector's First Task Is To Develop A Charter. Identify The Item That Should BeDocument105 pagesIrector's First Task Is To Develop A Charter. Identify The Item That Should BeNICELLE TAGLEPas encore d'évaluation

- Substantive Testing and DocumentationDocument3 pagesSubstantive Testing and DocumentationRose Medina BarondaPas encore d'évaluation

- Electricity Department, Government of Puducherry As-Is Study of The Electricity DepartmentDocument56 pagesElectricity Department, Government of Puducherry As-Is Study of The Electricity DepartmentIbraheem Adel SheerahPas encore d'évaluation

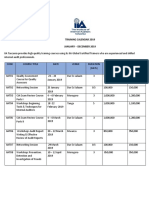

- IIA Calender 2019Document5 pagesIIA Calender 2019MtanaPas encore d'évaluation

- ISBP International Chamber of CommerceDocument66 pagesISBP International Chamber of CommercePrem Deep100% (1)

- Management Accounting: University of Sunderland Teg International CollegeDocument20 pagesManagement Accounting: University of Sunderland Teg International CollegeTrinh NguyễnPas encore d'évaluation

- Voluntary Winding Up and Removal of NamesDocument21 pagesVoluntary Winding Up and Removal of Namessreedevi sureshPas encore d'évaluation

- Cover LetterDocument2 pagesCover LetterBilal AslamPas encore d'évaluation