Vous aimerez peut-être aussi

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

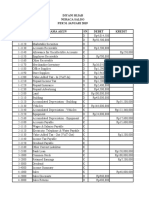

- ICICI Bank LimitedDocument1 pageICICI Bank LimitedNitin KhuranaPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Resume FormatDocument3 pagesResume FormatNitin KhuranaPas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- JobsDocument1 pageJobsNitin KhuranaPas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Ashok Leyland's ProfileDocument12 pagesAshok Leyland's ProfileNitin Khurana100% (1)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- F7.1 Chap 11 - Financial Instruments 2Document35 pagesF7.1 Chap 11 - Financial Instruments 2NapolnzoPas encore d'évaluation

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- IntroductionDocument58 pagesIntroductionSumit AgarwalPas encore d'évaluation

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- East West University: Final Assignment + Term PaperDocument5 pagesEast West University: Final Assignment + Term PaperHossain Mohamod IbrahimPas encore d'évaluation

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Revision Exercise - Question OnlyDocument6 pagesRevision Exercise - Question OnlyCindy WooPas encore d'évaluation

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Zakat Ul MalDocument7 pagesZakat Ul MalshiraaazPas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Financial Analysis ProblemDocument16 pagesFinancial Analysis ProblemShreyashi DasPas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Accounting Conservatism and Cost of Equity Capital Evidence From IndonesiaDocument9 pagesAccounting Conservatism and Cost of Equity Capital Evidence From IndonesiaMstefPas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- BSE Limited National Stock Exchange of India LimitedDocument28 pagesBSE Limited National Stock Exchange of India LimitedkrrkumarPas encore d'évaluation

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Breaking Up: Is Good To DoDocument12 pagesBreaking Up: Is Good To DoAnuroop BethuPas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Sw01 Shareholders Equity Key PDF FreeDocument5 pagesSw01 Shareholders Equity Key PDF FreePola PolzPas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Finance Aptitude Test: Profit & Loss AccountDocument2 pagesFinance Aptitude Test: Profit & Loss AccountjordanPas encore d'évaluation

- Navneet Publications Strategy - FLAME School of BusinessDocument20 pagesNavneet Publications Strategy - FLAME School of Businesschandramohan.patelPas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- 74736bos60488 m2 cp8Document40 pages74736bos60488 m2 cp8Vignesh VigneshPas encore d'évaluation

- Ifrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument80 pagesIfrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeReinch ClossPas encore d'évaluation

- Problems EPSDocument3 pagesProblems EPShukaPas encore d'évaluation

- Compiled Question File FSPDocument22 pagesCompiled Question File FSPsyed aliPas encore d'évaluation

- Real-Time Stock Market News FeedDocument2 pagesReal-Time Stock Market News FeedSeudonim SatoshiPas encore d'évaluation

- 5500 Sample PDFDocument3 pages5500 Sample PDFMwangi JosphatPas encore d'évaluation

- Kunci Jawaban Pt. Kharisma DigitalDocument92 pagesKunci Jawaban Pt. Kharisma DigitalChoyingOOying80% (25)

- Preparation of Single Entity Financial Statements - Part 1Document18 pagesPreparation of Single Entity Financial Statements - Part 1Vasileios LymperopoulosPas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Stocks and BondsDocument15 pagesStocks and BondsKobe Bullmastiff0% (1)

- Corporate and Business Law (Zimbabwe) : Monday 8 December 2014Document12 pagesCorporate and Business Law (Zimbabwe) : Monday 8 December 2014Phebieon MukwenhaPas encore d'évaluation

- Dilutive Securities and EPS: ACCT 320 Spring 2021 Samia AliDocument47 pagesDilutive Securities and EPS: ACCT 320 Spring 2021 Samia AliHassanAliPas encore d'évaluation

- Group Assignment 3 - Fall 2021 - Ashwin BaluDocument16 pagesGroup Assignment 3 - Fall 2021 - Ashwin Baluhalelz69Pas encore d'évaluation

- Session 4 of CSDocument8 pagesSession 4 of CSHaji HalviPas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Sun Life App Form Reg SR02829058Document10 pagesSun Life App Form Reg SR02829058Precious J Alolod ImportantePas encore d'évaluation

- Ifrs VS Us - GaapDocument20 pagesIfrs VS Us - Gaapalokshri25Pas encore d'évaluation

- Upmost Amended by Laws ADocument28 pagesUpmost Amended by Laws ACharmicah AquinoPas encore d'évaluation

- Ias32 SN PDFDocument8 pagesIas32 SN PDFShiza ArifPas encore d'évaluation

- Lembar Jawaban Siklus DagangDocument56 pagesLembar Jawaban Siklus DagangSuci Agriani IdrusPas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)