Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (120)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Financial Markets and Institutions - PART1Document75 pagesFinancial Markets and Institutions - PART1shweta_46664100% (3)

- Portfolio Analysis-Case On Alex SharpeDocument30 pagesPortfolio Analysis-Case On Alex SharpeKomalDewanandChaudharyPas encore d'évaluation

- Monetary and Fiscal PoliciesDocument27 pagesMonetary and Fiscal PoliciesSean Bofill-Gallardo100% (1)

- A Study On Dividend PolicyDocument75 pagesA Study On Dividend PolicyVeera Bhadra Chary ChPas encore d'évaluation

- Mastering The Art of Tape ReadingDocument2 pagesMastering The Art of Tape ReadingAnupam Bhardwaj100% (1)

- Solution of Corporate Finance Exams On 14th April Phuong Anh MDE10Document8 pagesSolution of Corporate Finance Exams On 14th April Phuong Anh MDE10api-3729903100% (1)

- Synopsis of Merger and AcquisitionDocument8 pagesSynopsis of Merger and Acquisitionajay008751608857% (7)

- KTQTDHQG2006 Chapter 6Document13 pagesKTQTDHQG2006 Chapter 6api-3729903Pas encore d'évaluation

- Tuyen Tap Thanh Ngu - Tuc Ngu - CA DaoDocument304 pagesTuyen Tap Thanh Ngu - Tuc Ngu - CA Daoapi-3729903100% (1)

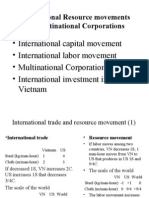

- Course International Economics - UpdatedDocument3 pagesCourse International Economics - Updatedapi-3729903Pas encore d'évaluation

- KTQTDHQG2006 Chapter 7Document18 pagesKTQTDHQG2006 Chapter 7api-3729903Pas encore d'évaluation

- Chap 6Document20 pagesChap 6api-3729903Pas encore d'évaluation

- Chap 7Document32 pagesChap 7api-3729903Pas encore d'évaluation

- Chap 2Document20 pagesChap 2api-3729903Pas encore d'évaluation

- Chap 5Document23 pagesChap 5api-3729903Pas encore d'évaluation

- Chap 3Document20 pagesChap 3api-3729903Pas encore d'évaluation

- Chap 1Document20 pagesChap 1api-3729903Pas encore d'évaluation

- PCM Manual 2004 enDocument158 pagesPCM Manual 2004 enAydın FenerliPas encore d'évaluation

- NGAS 2019 eBOOKDocument128 pagesNGAS 2019 eBOOKGabinu AngPas encore d'évaluation

- Module-2 Export-Import Trade - Regulatory FrameworkDocument12 pagesModule-2 Export-Import Trade - Regulatory Frameworksudhir.kochhar3530100% (2)

- AglforDocument179 pagesAglforlenovojiPas encore d'évaluation

- History of DerivativesDocument29 pagesHistory of Derivativeshanunesh100% (1)

- Portfolio Optimization Under Liquidity Costs: Dieter Kalin Rudi ZagstDocument16 pagesPortfolio Optimization Under Liquidity Costs: Dieter Kalin Rudi Zagstzouzou93Pas encore d'évaluation

- Interim Order in The Matter of SCL Steel Corporation LimitedDocument19 pagesInterim Order in The Matter of SCL Steel Corporation LimitedShyam SunderPas encore d'évaluation

- Gnlumsil 2017 - Moot ProblemDocument10 pagesGnlumsil 2017 - Moot ProblemShashwat DroliaPas encore d'évaluation

- Wikipedia Book FinanceDocument105 pagesWikipedia Book FinanceEduardo AranibarPas encore d'évaluation

- TK BAI2Document23 pagesTK BAI2saurabh_565Pas encore d'évaluation

- Alcatel Lucent CasestudyDocument12 pagesAlcatel Lucent CasestudySudarshan SharmaPas encore d'évaluation

- Tutorial Answers FDIDocument6 pagesTutorial Answers FDISong YeePas encore d'évaluation

- Assest Liability Management On HeritageDocument76 pagesAssest Liability Management On Heritagearjunmba1196240% (1)

- 3er. SET DE EJERCICIOSDocument3 pages3er. SET DE EJERCICIOSCesar CameyPas encore d'évaluation

- Approximating Total Stock Market - BogleheadsDocument4 pagesApproximating Total Stock Market - BogleheadsOladipupo Mayowa PaulPas encore d'évaluation

- Chapter 13 International FinanceDocument35 pagesChapter 13 International FinanceDivyesh GandhiPas encore d'évaluation

- For Mba Student Summer Assignment IfsDocument17 pagesFor Mba Student Summer Assignment IfsRajan ShrivastavaPas encore d'évaluation

- Economic 3Document42 pagesEconomic 3Jerry WidePas encore d'évaluation

- Premium Announces Private Placement of Senior Secured DebenturesDocument5 pagesPremium Announces Private Placement of Senior Secured DebenturesCielo RamonePas encore d'évaluation

- Treasury & Risk Management: Post Graduate Diploma in Management (ePGDM)Document13 pagesTreasury & Risk Management: Post Graduate Diploma in Management (ePGDM)Jitendra YadavPas encore d'évaluation

- DR Stanisław Kubielas: International FinanceDocument4 pagesDR Stanisław Kubielas: International FinanceGorana Goga RadisicPas encore d'évaluation

- Wallstreetjournaleurope 20170824 TheWallStreetJournal-Europe PDFDocument20 pagesWallstreetjournaleurope 20170824 TheWallStreetJournal-Europe PDFepustakakoranPas encore d'évaluation

- Documents - Ienergizer Admission Document 27 8 101 PDFDocument120 pagesDocuments - Ienergizer Admission Document 27 8 101 PDFShubham ChahalPas encore d'évaluation

- Linear Programming Formulation Problems Set 3Document3 pagesLinear Programming Formulation Problems Set 3amit056100% (1)

- 2021-10-01 World Coin NewsDocument48 pages2021-10-01 World Coin NewsWalter MaikPas encore d'évaluation