Vous aimerez peut-être aussi

- Loan Agreement Corporate SimpleDocument2 pagesLoan Agreement Corporate SimpleJennifer Deleon100% (1)

- Payday Loans PDFDocument33 pagesPayday Loans PDFRyan HayesPas encore d'évaluation

- Finance 100Document865 pagesFinance 100jhamez16Pas encore d'évaluation

- Macroeconomics Key GraphsDocument5 pagesMacroeconomics Key Graphsapi-243723152Pas encore d'évaluation

- The Behavior of Interest RatesDocument39 pagesThe Behavior of Interest RatesRhazes Zy100% (1)

- Levich Ch13 Net Assignment SolutionsDocument24 pagesLevich Ch13 Net Assignment Solutionsveda20Pas encore d'évaluation

- Financial Management - PPT - Pgdm2010Document94 pagesFinancial Management - PPT - Pgdm2010Prabhakar Patnaik100% (1)

- Economics/05 Monetary and Fiscal PolicyDocument45 pagesEconomics/05 Monetary and Fiscal PolicyHarshavardhan SJPas encore d'évaluation

- Wings 2017Document197 pagesWings 2017amarPas encore d'évaluation

- TML Gasket vs. BPI Family Savings Jan 2013Document2 pagesTML Gasket vs. BPI Family Savings Jan 2013Sam LeynesPas encore d'évaluation

- Etextbook 978 0132992282 MacroeconomicsDocument61 pagesEtextbook 978 0132992282 Macroeconomicslee.ortiz429100% (49)

- Economics 302 (Sec. 001) Intermediate Macroeconomic Theory and Policy Theory and PolicyDocument15 pagesEconomics 302 (Sec. 001) Intermediate Macroeconomic Theory and Policy Theory and Policytai2000Pas encore d'évaluation

- Week 2 Part OneDocument20 pagesWeek 2 Part OneLisimoana TupouPas encore d'évaluation

- Eco ch4Document2 pagesEco ch4fatema hosseiniPas encore d'évaluation

- Money and BankingDocument10 pagesMoney and BankingMaruf AhmedPas encore d'évaluation

- Money Supply and Money Demand: Chapter EighteenDocument16 pagesMoney Supply and Money Demand: Chapter EighteenSharad Ranjan TyagiPas encore d'évaluation

- The Financial Sector of The Economy: Money and BankingDocument12 pagesThe Financial Sector of The Economy: Money and BankingNefta BaptistePas encore d'évaluation

- Assignment 1Document6 pagesAssignment 1Ken PhanPas encore d'évaluation

- Topic 4 Saving and Investment (Updated 15 May 2017)Document15 pagesTopic 4 Saving and Investment (Updated 15 May 2017)Arun GhatanPas encore d'évaluation

- Practice For Chapter 5 SolutionsDocument6 pagesPractice For Chapter 5 SolutionsAndrew WhitfieldPas encore d'évaluation

- MIT14 02F09 Lec10Document27 pagesMIT14 02F09 Lec10mkmusaPas encore d'évaluation

- 10 Rules of EconomicsDocument4 pages10 Rules of EconomicsJames GrahamPas encore d'évaluation

- Chapter#04: Financial MarketsDocument4 pagesChapter#04: Financial Marketshifza anwarPas encore d'évaluation

- 5 WEEK GEHon Economics IIth Semeter Introductory MacroeconomicsDocument14 pages5 WEEK GEHon Economics IIth Semeter Introductory Macroeconomicskasturisahoo20Pas encore d'évaluation

- Presentation EcoDocument9 pagesPresentation EcoDipayan DebnathPas encore d'évaluation

- Task M3Document2 pagesTask M3bendermacherrickPas encore d'évaluation

- Money Growth and Inflation: The Classical Theory of InflationDocument5 pagesMoney Growth and Inflation: The Classical Theory of InflationIzzahPas encore d'évaluation

- Financial MarketsDocument32 pagesFinancial MarketsArief Kurniawan100% (1)

- A. Money and The Banking SystemDocument9 pagesA. Money and The Banking SystemShoniqua JohnsonPas encore d'évaluation

- ECON1132 Midterm2 2013springDocument4 pagesECON1132 Midterm2 2013springexamkillerPas encore d'évaluation

- Financial IntermediariesDocument3 pagesFinancial IntermediariesSanchit MiglaniPas encore d'évaluation

- Chapter 25Document7 pagesChapter 25Tasnim SghairPas encore d'évaluation

- Unit V Behavioural Foundations: InvestmentDocument10 pagesUnit V Behavioural Foundations: InvestmentRonak PoddarPas encore d'évaluation

- Money Is Defined As Any Asset That People Are Willing To Accept in Exchange For Goods andDocument4 pagesMoney Is Defined As Any Asset That People Are Willing To Accept in Exchange For Goods andVũ Hồng PhươngPas encore d'évaluation

- The Money Supply and Inflation PPT at Bec DomsDocument49 pagesThe Money Supply and Inflation PPT at Bec DomsBabasab Patil (Karrisatte)Pas encore d'évaluation

- Group 3 Money Banking and Monetary PolicyDocument46 pagesGroup 3 Money Banking and Monetary PolicyjustinedeguzmanPas encore d'évaluation

- Chapter 13 & 14 Money, Banks, The Federal Reserve System and Monetary PolicyDocument7 pagesChapter 13 & 14 Money, Banks, The Federal Reserve System and Monetary PolicyDiamante GomezPas encore d'évaluation

- Principles of MacroeconomicsDocument52 pagesPrinciples of Macroeconomicsmoaz21100% (1)

- Money and Inflation: Questions For ReviewDocument6 pagesMoney and Inflation: Questions For ReviewErjon SkordhaPas encore d'évaluation

- Financial Markets: ECON 2123: MacroeconomicsDocument40 pagesFinancial Markets: ECON 2123: MacroeconomicskatecwsPas encore d'évaluation

- Chapters 26 and 27 Principles of Economics, Fourth Edition N. Gregory MankiwDocument42 pagesChapters 26 and 27 Principles of Economics, Fourth Edition N. Gregory MankiwDao Tuan Anh100% (2)

- PP6Document10 pagesPP6Sambit MishraPas encore d'évaluation

- Group 6.time Value of Money and Risk and Return - FinMan FacilitationDocument95 pagesGroup 6.time Value of Money and Risk and Return - FinMan FacilitationNaia SPas encore d'évaluation

- Money and Monetary Policy: Chapter 11Document18 pagesMoney and Monetary Policy: Chapter 11Ji YuPas encore d'évaluation

- Goods and Money Market: Unit 3Document28 pagesGoods and Money Market: Unit 3Mrigesh AgarwalPas encore d'évaluation

- Money Lecture 1 2020Document40 pagesMoney Lecture 1 2020vusal.abdullaev17Pas encore d'évaluation

- The Money MarketDocument20 pagesThe Money MarketNick GrzebienikPas encore d'évaluation

- Chapter 3Document11 pagesChapter 3Tasebe GetachewPas encore d'évaluation

- Learning OutcomesDocument10 pagesLearning OutcomesRajesh GargPas encore d'évaluation

- Money Supply NotesDocument10 pagesMoney Supply Notesmary wanjiruPas encore d'évaluation

- Problem Set (LSE)Document3 pagesProblem Set (LSE)ARUPARNA MAITYPas encore d'évaluation

- Monetary PolicyDocument10 pagesMonetary PolicykafiPas encore d'évaluation

- Engaging Activity A Financial MarketsDocument2 pagesEngaging Activity A Financial MarketsMary Justine ManaloPas encore d'évaluation

- Session 11 - Money Demand - Equil Interest RateDocument7 pagesSession 11 - Money Demand - Equil Interest Rates0falaPas encore d'évaluation

- Summary-Chapter 8Document3 pagesSummary-Chapter 8DhrushiPas encore d'évaluation

- FM Unit 4 Lecture Notes - Time Value of MoneyDocument4 pagesFM Unit 4 Lecture Notes - Time Value of MoneyDebbie DebzPas encore d'évaluation

- Groups 3 Qna The Monetary System What It Is and How It Works PDFDocument8 pagesGroups 3 Qna The Monetary System What It Is and How It Works PDFNing Ai SatyawatiPas encore d'évaluation

- 6 Money SupplyDocument6 pages6 Money SupplySaroj LamichhanePas encore d'évaluation

- Lecture Yeid To MaturityDocument32 pagesLecture Yeid To MaturityUmerPas encore d'évaluation

- Ec103 Week 03 s14Document20 pagesEc103 Week 03 s14юрий локтионовPas encore d'évaluation

- TVM Stocks and BondsDocument40 pagesTVM Stocks and Bondseshkhan100% (1)

- Chapter 2Document22 pagesChapter 2Tiến ĐứcPas encore d'évaluation

- Macroeconomics Unit 4 Multiple ChoiceDocument13 pagesMacroeconomics Unit 4 Multiple ChoiceAleihsmeiPas encore d'évaluation

- Time Value of Money - TheoryDocument7 pagesTime Value of Money - TheoryNahidul Islam IUPas encore d'évaluation

- Modern Measures of MoneyDocument6 pagesModern Measures of MoneyCrisly-Mae Ann AquinoPas encore d'évaluation

- Loans ReceivableDocument3 pagesLoans ReceivableGee Lysa Pascua VilbarPas encore d'évaluation

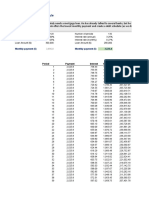

- Excel Student Loan Amortization TableDocument18 pagesExcel Student Loan Amortization TableIsmail UsmanPas encore d'évaluation

- Tobin's Theory of Demand For MoneyDocument6 pagesTobin's Theory of Demand For MoneyShofi R Krishna100% (20)

- Mortgage Pools, Pass-Throughs, and CmosDocument24 pagesMortgage Pools, Pass-Throughs, and CmossamuelPas encore d'évaluation

- Home Loan EMI Calculator Amortization ScheduleDocument4 pagesHome Loan EMI Calculator Amortization ScheduleMahatoPas encore d'évaluation

- B.Sc. Economics Honours - Detailed SyllabusDocument49 pagesB.Sc. Economics Honours - Detailed SyllabusNeelarka RoyPas encore d'évaluation

- Al-Rahnu VS Conventional Pawn Broking: Group 12 Maybank Islamic BankDocument14 pagesAl-Rahnu VS Conventional Pawn Broking: Group 12 Maybank Islamic BanknghingliungPas encore d'évaluation

- EMI Calculator 02/02/2022: Please Click On The Link Below To Download The ApplicationDocument11 pagesEMI Calculator 02/02/2022: Please Click On The Link Below To Download The ApplicationAmar KambalePas encore d'évaluation

- Loan Application ProcessDocument17 pagesLoan Application Processsamm yuuPas encore d'évaluation

- 3.2 70. Exercise Loan Schedule SolvedDocument6 pages3.2 70. Exercise Loan Schedule SolvedAniket KarnPas encore d'évaluation

- MakroekonomiDocument3 pagesMakroekonomiYew SeangPas encore d'évaluation

- GI Book 6e-170-172Document3 pagesGI Book 6e-170-172ANH PHAM QUYNHPas encore d'évaluation

- You Exec - Ultimate Loan FreeDocument174 pagesYou Exec - Ultimate Loan FreeVíctor Hugo TeránPas encore d'évaluation

- Simple Interest GameDocument4 pagesSimple Interest GameCarmina CunananPas encore d'évaluation

- Chapter 20 Problems and SolutionsDocument5 pagesChapter 20 Problems and Solutionsfahmeed786Pas encore d'évaluation

- Loan Prob SolDocument3 pagesLoan Prob SolAnonymous pH3jHscX9Pas encore d'évaluation

- 1 GENMATH DiomampoAyessa Brochure SA2Document2 pages1 GENMATH DiomampoAyessa Brochure SA2Marjorie ChavezPas encore d'évaluation

- Credit Eda Case Study: Aparna Trivedi Ashish Nipane DS C29Document13 pagesCredit Eda Case Study: Aparna Trivedi Ashish Nipane DS C29aparnaPas encore d'évaluation

- Singapore Property Weekly Issue 284Document11 pagesSingapore Property Weekly Issue 284Propwise.sgPas encore d'évaluation

- Money Demand, The Equilibrium Interest Rate, and Monetary PolicyDocument29 pagesMoney Demand, The Equilibrium Interest Rate, and Monetary PolicyAbood AlissaPas encore d'évaluation

- TVR Format - Shrikrushn Namdev Kavar - TF4343554Document19 pagesTVR Format - Shrikrushn Namdev Kavar - TF4343554Nikhil MohanePas encore d'évaluation

- Caraga Administrative Region Division of Surigao Del NorteDocument21 pagesCaraga Administrative Region Division of Surigao Del NorteLex AmariePas encore d'évaluation

- Chapter 18Document4 pagesChapter 18Alex GuPas encore d'évaluation