Vous aimerez peut-être aussi

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

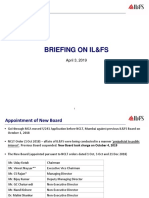

- ILFS Briefing (April 2019)Document15 pagesILFS Briefing (April 2019)Richard DierdrePas encore d'évaluation

- Anti-Money Laundering Risks To Financial InstitutionsDocument16 pagesAnti-Money Laundering Risks To Financial InstitutionsLexisNexis Risk Division100% (7)

- UPSA 2019 Tutorial Questions Fs WITH ANSWERSDocument14 pagesUPSA 2019 Tutorial Questions Fs WITH ANSWERSLaud ListowellPas encore d'évaluation

- Sohrabi 2019Document42 pagesSohrabi 2019Brayan TillaguangoPas encore d'évaluation

- (Springer Finance) Dr. Manuel Ammann (Auth.) - Credit Risk Valuation - Methods, Models, and Applications-Springer Berlin Heidelberg (2001)Document258 pages(Springer Finance) Dr. Manuel Ammann (Auth.) - Credit Risk Valuation - Methods, Models, and Applications-Springer Berlin Heidelberg (2001)Amel AmarPas encore d'évaluation

- Commerzbank AG: Issuer Rating ReportDocument12 pagesCommerzbank AG: Issuer Rating ReportvaishnaviPas encore d'évaluation

- Tutorial 1 PresentDocument12 pagesTutorial 1 PresentLi NiniPas encore d'évaluation

- SOE11144 Global Business Economics and FinanceDocument12 pagesSOE11144 Global Business Economics and FinanceNadia RiazPas encore d'évaluation

- Dipolog Rice Mill Journal EntriesDocument4 pagesDipolog Rice Mill Journal EntriesRenz RaphPas encore d'évaluation

- Suryaa Hotel Bal SheetDocument3 pagesSuryaa Hotel Bal Sheetarjun chauhan100% (1)

- 705 - PGBP AdjustmentsDocument10 pages705 - PGBP AdjustmentsKumar SwamyPas encore d'évaluation

- Desirable Corporate Governance: A CodeDocument16 pagesDesirable Corporate Governance: A CodesiddharthanandPas encore d'évaluation

- Fin Ca2 FinalDocument6 pagesFin Ca2 FinalVaishali SonarePas encore d'évaluation

- Finance Master Thesis PDFDocument7 pagesFinance Master Thesis PDFafkojbvmz100% (2)

- Analysis of Factors Influencing Bank ProfitabilityDocument35 pagesAnalysis of Factors Influencing Bank ProfitabilityA M DraganPas encore d'évaluation

- Payment 4310725205Document1 pagePayment 4310725205Radoslav TsvetkovPas encore d'évaluation

- Winter Project Report (Mba) "Risk Management in Debt Funds of State Bank of India"Document79 pagesWinter Project Report (Mba) "Risk Management in Debt Funds of State Bank of India"ShubhampratapsPas encore d'évaluation

- SAP MiningDocument2 pagesSAP Miningsaikiran100% (1)

- FirstStrike PlusDocument5 pagesFirstStrike Plusartus14Pas encore d'évaluation

- Bajaj Allianz InsuranceDocument93 pagesBajaj Allianz InsuranceswatiPas encore d'évaluation

- Q1. Write Down The Accounting Entries Passed While Issuing A Dd/Po ? AnsDocument6 pagesQ1. Write Down The Accounting Entries Passed While Issuing A Dd/Po ? Ansabhishek gautamPas encore d'évaluation

- Financial Daily: Putrajaya Files Rm680M Forfeiture ActionDocument33 pagesFinancial Daily: Putrajaya Files Rm680M Forfeiture ActionPG ChongPas encore d'évaluation

- Week 012-Presentation Key Concepts of Simple and Compound Interests, and Simple and General Annuities - Part 002Document18 pagesWeek 012-Presentation Key Concepts of Simple and Compound Interests, and Simple and General Annuities - Part 002Alleona EmbolodePas encore d'évaluation

- Swift MT RulesDocument2 pagesSwift MT RulesJit JackPas encore d'évaluation

- Central Bank-Monetary Policy ReviewDocument6 pagesCentral Bank-Monetary Policy ReviewAda DeranaPas encore d'évaluation

- Financial Report (October 2017)Document2 pagesFinancial Report (October 2017)Marija DukićPas encore d'évaluation

- Eduardo Tabrilla Business Plan AssignmentDocument4 pagesEduardo Tabrilla Business Plan AssignmentJed Jt TabrillaPas encore d'évaluation

- Engineering Economy1Document13 pagesEngineering Economy1Roselyn MatienzoPas encore d'évaluation

- Ssi FinancingDocument7 pagesSsi FinancingAnanya ChoudharyPas encore d'évaluation

- MouthfreshenerdprDocument22 pagesMouthfreshenerdprSumit SharmaPas encore d'évaluation