Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Risk Assessment of E-BankingDocument15 pagesRisk Assessment of E-Bankingsamankhan_01Pas encore d'évaluation

- This Is ItDocument47 pagesThis Is Itsamankhan_01Pas encore d'évaluation

- GROUPDocument17 pagesGROUPsamankhan_01Pas encore d'évaluation

- Principles of ManagementDocument18 pagesPrinciples of Managementsamankhan_01Pas encore d'évaluation

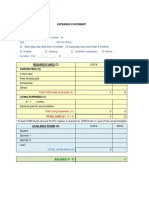

- F&ADocument14 pagesF&Asamankhan_01Pas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Description: Tags: Sar34Document48 pagesDescription: Tags: Sar34anon-862701Pas encore d'évaluation

- Financial Management - Part 1 For PrintingDocument13 pagesFinancial Management - Part 1 For PrintingKimberly Pilapil MaragañasPas encore d'évaluation

- Cashflow 2004Document137 pagesCashflow 2004goodman123123Pas encore d'évaluation

- Meenu Chopra Income Tax BasicsDocument66 pagesMeenu Chopra Income Tax BasicsRvi Mahay100% (1)

- 2015 Bar Exam Suggested Answers in Mercantile LawDocument14 pages2015 Bar Exam Suggested Answers in Mercantile Lawargao100% (1)

- Islamic Law ProjectDocument8 pagesIslamic Law ProjectSami UllahPas encore d'évaluation

- Impact of Microfinance on Women EmpowermentDocument15 pagesImpact of Microfinance on Women EmpowermentPankaj sharmaPas encore d'évaluation

- Two Envelope Bidding Section I InstructionsDocument111 pagesTwo Envelope Bidding Section I InstructionsCUTto1122Pas encore d'évaluation

- Accounting RatiosDocument5 pagesAccounting RatiosNaga NikhilPas encore d'évaluation

- GBF Unit - IVDocument50 pagesGBF Unit - IVKaliyapersrinivasanPas encore d'évaluation

- A Simple FTP Model For A Commercial BankDocument80 pagesA Simple FTP Model For A Commercial BankMaratAyaibergenovPas encore d'évaluation

- GTAI Industry Overview Medical TechnologyDocument12 pagesGTAI Industry Overview Medical TechnologyphilatusPas encore d'évaluation

- Big Bank Business: The Ethics and Social Responsibility of The Finance IndustryDocument2 pagesBig Bank Business: The Ethics and Social Responsibility of The Finance IndustryFaculty of the ProfessionsPas encore d'évaluation

- Corporate Law ProjectDocument15 pagesCorporate Law ProjectAyushi VermaPas encore d'évaluation

- Loan Statement SummaryDocument2 pagesLoan Statement SummaryNewsletter Online Technical supportPas encore d'évaluation

- Financing Infrastructure in the Philippines: Assessing Fiscal Resources and OpportunitiesDocument64 pagesFinancing Infrastructure in the Philippines: Assessing Fiscal Resources and OpportunitiesCarmelita EsclandaPas encore d'évaluation

- Offer To Purchase Assets of Business (Long Form)Document7 pagesOffer To Purchase Assets of Business (Long Form)Legal Forms100% (1)

- Annamalai 2nd Year MBA FINANCIAL MANAGEMENT 349 Solved Assignment 2020 Call 9025810064Document5 pagesAnnamalai 2nd Year MBA FINANCIAL MANAGEMENT 349 Solved Assignment 2020 Call 9025810064Palaniappan NPas encore d'évaluation

- Different Loans/Financing Schemes for Rooftop Solar ProjectsDocument4 pagesDifferent Loans/Financing Schemes for Rooftop Solar ProjectsnaveenkumargmrPas encore d'évaluation

- Why Is The BSP The Main Government Agency Responsible For Promoting Price StabilityDocument4 pagesWhy Is The BSP The Main Government Agency Responsible For Promoting Price StabilityMarielle CatiisPas encore d'évaluation

- Surname: First Name: Campus France Registration Number: IN Age: Marital StatusDocument2 pagesSurname: First Name: Campus France Registration Number: IN Age: Marital StatusSahil ShahPas encore d'évaluation

- Obligation and Contracts-ECEDocument45 pagesObligation and Contracts-ECECrisJoshDizon50% (6)

- E.W.F. LOAN APPLICATION FORMDocument2 pagesE.W.F. LOAN APPLICATION FORMapi-3710215Pas encore d'évaluation

- Success Is in Our Own HandsDocument12 pagesSuccess Is in Our Own HandsEnp Gus AgostoPas encore d'évaluation

- Dacion en PagoDocument2 pagesDacion en PagoJC93% (15)

- Domondon Tax Q&ADocument54 pagesDomondon Tax Q&AHelena Herrera0% (1)

- Learning From Dr. Michael J. Burrys Investment Philosophy 2Document25 pagesLearning From Dr. Michael J. Burrys Investment Philosophy 2Leonard WijayaPas encore d'évaluation

- Extrajudicial Foreclosure of Real Estate MortgageDocument3 pagesExtrajudicial Foreclosure of Real Estate Mortgageclifford b cubianPas encore d'évaluation

- ReturnDocument1 pageReturnFaisal Islam ButtPas encore d'évaluation