Vous aimerez peut-être aussi

- The LLC Launchpad: Navigate Your Business Journey with ConfidenceD'EverandThe LLC Launchpad: Navigate Your Business Journey with ConfidencePas encore d'évaluation

- Auditing 2020 21 Cabrera 1 5Document148 pagesAuditing 2020 21 Cabrera 1 5MisshtaCPas encore d'évaluation

- Chapter 1 AuditDocument13 pagesChapter 1 AuditMisshtaC100% (1)

- AAS CH1 2 1 - MergedDocument19 pagesAAS CH1 2 1 - MergedRoel PaistePas encore d'évaluation

- Client Due Diligence Factsheet 0621Document4 pagesClient Due Diligence Factsheet 0621Robinson JeybarajPas encore d'évaluation

- Case 2.2 and 2.5 AnswersDocument4 pagesCase 2.2 and 2.5 AnswersHeni OktaviantiPas encore d'évaluation

- MEH - Combined (1) - 7Document9 pagesMEH - Combined (1) - 7Gandhi Jenny Rakeshkumar BD20029Pas encore d'évaluation

- Sample Due Diligence Report PDFDocument47 pagesSample Due Diligence Report PDFIbukun Sorinola70% (20)

- The Role of Auditors With Their Clients and Third PartiesDocument5 pagesThe Role of Auditors With Their Clients and Third PartiesInamul HaquePas encore d'évaluation

- Why Confidentiality Is Important: Jessica A. Paquera Bsa-Ii Quiz No. 4 Prelim June 27,2019Document4 pagesWhy Confidentiality Is Important: Jessica A. Paquera Bsa-Ii Quiz No. 4 Prelim June 27,2019febelovePas encore d'évaluation

- Code of Ethics Reviewer - CompressDocument44 pagesCode of Ethics Reviewer - CompressGlance Piscasio CruzPas encore d'évaluation

- 2-6int 2002 Dec ADocument14 pages2-6int 2002 Dec AJay ChenPas encore d'évaluation

- Pillars of Corporate GovernanvceDocument8 pagesPillars of Corporate GovernanvceabcPas encore d'évaluation

- Copy (3) of Copy of Corporate Governance 1Document20 pagesCopy (3) of Copy of Corporate Governance 1bappa85Pas encore d'évaluation

- SecurityIT Report (Dhane Naidu)Document12 pagesSecurityIT Report (Dhane Naidu)Dhaneletcumi Naidu VijayakumarPas encore d'évaluation

- Company Law Research PaperDocument10 pagesCompany Law Research PaperRohit RajuPas encore d'évaluation

- The Accountancy ProfessionDocument12 pagesThe Accountancy ProfessionJessica CorpuzPas encore d'évaluation

- Legal Importance of Due Diligence ReportDocument6 pagesLegal Importance of Due Diligence Reportmanish88raiPas encore d'évaluation

- The Importance of Forensic AuditDocument6 pagesThe Importance of Forensic AuditkharismaPas encore d'évaluation

- How To Revive A Struggling Business Back To LifeDocument42 pagesHow To Revive A Struggling Business Back To Lifejohn ChukwuemekaPas encore d'évaluation

- Chapter 03 - Answer PDFDocument8 pagesChapter 03 - Answer PDFjhienellPas encore d'évaluation

- Doctrine of Indoor Management: Holistic Analysis From Legal and Business PrismDocument7 pagesDoctrine of Indoor Management: Holistic Analysis From Legal and Business PrismKaustubh PatilPas encore d'évaluation

- Auditing Principles and PracticesDocument58 pagesAuditing Principles and PracticeskainatPas encore d'évaluation

- Accounting Information SystemDocument7 pagesAccounting Information SystemWahida AmalinPas encore d'évaluation

- Solution Manual For Auditing and Assurance Services Arens Elder Beasley 15th EditionDocument15 pagesSolution Manual For Auditing and Assurance Services Arens Elder Beasley 15th EditionMeredithFleminggztay100% (86)

- Acca f4 Notes Part HDocument9 pagesAcca f4 Notes Part HBryan TengPas encore d'évaluation

- Exam For Non Accountants UPDATEDDocument3 pagesExam For Non Accountants UPDATEDWycliffe Luther RosalesPas encore d'évaluation

- Due Diligence BookDocument50 pagesDue Diligence Bookgritad100% (2)

- Midterm ExaminationsDocument4 pagesMidterm ExaminationsBea Czarina NavarroPas encore d'évaluation

- Lifting The Veil in Company Law Additional Notes LubogoDocument19 pagesLifting The Veil in Company Law Additional Notes LubogolubogoPas encore d'évaluation

- Auditing Principle 1 - ch1Document7 pagesAuditing Principle 1 - ch1Duguma BejigaPas encore d'évaluation

- Forensic Accounting ReportDocument11 pagesForensic Accounting ReportNike ColePas encore d'évaluation

- Summary of IFRS 3 PDFDocument15 pagesSummary of IFRS 3 PDFIvy Gail PamplonaPas encore d'évaluation

- Due Diligence in Concept With Financial Due DiligenceDocument58 pagesDue Diligence in Concept With Financial Due DiligenceZoya SayyedPas encore d'évaluation

- The Credibility CrisisDocument2 pagesThe Credibility CrisisEditor IJTSRDPas encore d'évaluation

- Investment Banking: Submitted ToDocument19 pagesInvestment Banking: Submitted ToklhthPas encore d'évaluation

- Midterm Home Take Exam - Entrepreneurship & SMEsDocument7 pagesMidterm Home Take Exam - Entrepreneurship & SMEsmohamed fathyPas encore d'évaluation

- Who Can Hear The Whistle Blow Whistleblowing and Its Impact On Corporate Governance in IndiaDocument3 pagesWho Can Hear The Whistle Blow Whistleblowing and Its Impact On Corporate Governance in IndiaVikram DasPas encore d'évaluation

- FORENSIC ACCOUNTING - Accounting Information SystemsDocument8 pagesFORENSIC ACCOUNTING - Accounting Information SystemsCharlene Estrella MatubisPas encore d'évaluation

- Auditing 1Document3 pagesAuditing 1Jolina I. BadoPas encore d'évaluation

- Module 6 Part 1 Internal ControlDocument21 pagesModule 6 Part 1 Internal ControlHailsey WinterPas encore d'évaluation

- Chapter 3 - Assignment - Marcellana, Ariel P. - Bsa-31Document5 pagesChapter 3 - Assignment - Marcellana, Ariel P. - Bsa-31Marcellana ArianePas encore d'évaluation

- Case StudiesDocument2 pagesCase StudiesSania Syed HassanPas encore d'évaluation

- Define Fraud, and Explain The Two Types of Misstatements That Are Relevant To Auditors' Consideration of FraudDocument3 pagesDefine Fraud, and Explain The Two Types of Misstatements That Are Relevant To Auditors' Consideration of FraudSomething ChicPas encore d'évaluation

- Chapter 1 - AACA P1Document7 pagesChapter 1 - AACA P1Toni Rose Hernandez LualhatiPas encore d'évaluation

- Module 6 Part 1 Internal ControlDocument21 pagesModule 6 Part 1 Internal ControlKRISTINA CASSANDRA CUEVASPas encore d'évaluation

- Module 1 Financial Accounting For MBAs - 6th EditionDocument15 pagesModule 1 Financial Accounting For MBAs - 6th EditionjoshPas encore d'évaluation

- Learning The LegaleseDocument30 pagesLearning The LegaleseapachedaltonPas encore d'évaluation

- Chapter Twelve Role of Various Agencies in Ensuring Ethics in CorporationsDocument51 pagesChapter Twelve Role of Various Agencies in Ensuring Ethics in CorporationsMuhammad TariqPas encore d'évaluation

- Distinguish Between Ethical Issues and Legal IssuesDocument4 pagesDistinguish Between Ethical Issues and Legal IssuesSharmaine manobanPas encore d'évaluation

- F8 Small NotesDocument22 pagesF8 Small NotesAnthimos Elia100% (1)

- Auditing AssignmentDocument5 pagesAuditing AssignmentHarry K. MatolaPas encore d'évaluation

- KYC QuestionsDocument11 pagesKYC QuestionshariPas encore d'évaluation

- BE Module 5Document5 pagesBE Module 5Thanmayi VanteruPas encore d'évaluation

- Summary of Andrew Sherman's Mergers and Acquisitions from A to ZD'EverandSummary of Andrew Sherman's Mergers and Acquisitions from A to ZPas encore d'évaluation

- Summary of Gregory R. Caruso's The Art of Business ValuationD'EverandSummary of Gregory R. Caruso's The Art of Business ValuationPas encore d'évaluation

- Textbook of Urgent Care Management: Chapter 7, Exit Transactions: The Process of Selling an Urgent Care CenterD'EverandTextbook of Urgent Care Management: Chapter 7, Exit Transactions: The Process of Selling an Urgent Care CenterPas encore d'évaluation

- Investment Reviewer With Answer SolutionsDocument39 pagesInvestment Reviewer With Answer SolutionsYmmymmPas encore d'évaluation

- Market Value Vs Historical CostDocument6 pagesMarket Value Vs Historical Costassime_hPas encore d'évaluation

- Credit Card Industry in IndiaDocument124 pagesCredit Card Industry in IndiaMandar KadamPas encore d'évaluation

- Definition Explained:: Liabilities A Liability Is ADocument26 pagesDefinition Explained:: Liabilities A Liability Is ACurtain SoenPas encore d'évaluation

- Nedim Halilagic HWDocument4 pagesNedim Halilagic HWNedim HalilagicPas encore d'évaluation

- Books of AccountDocument41 pagesBooks of AccountA cPas encore d'évaluation

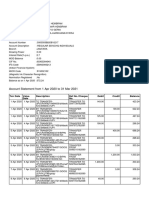

- Account Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument14 pagesAccount Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceHyper GamingPas encore d'évaluation

- ACC 101 MidtermDocument2 pagesACC 101 MidtermNguyen Ngoc Minh Chau (K15 HL)Pas encore d'évaluation

- Warren Adaptasi Edisi 2 - Ch05-1Document83 pagesWarren Adaptasi Edisi 2 - Ch05-1AninditaNurAnnisaPas encore d'évaluation

- Final Report: Submitted By: TAIMOOR RIAZ 13044954-030 Submitted ToDocument65 pagesFinal Report: Submitted By: TAIMOOR RIAZ 13044954-030 Submitted ToSherryMirzaPas encore d'évaluation

- Summary ReportDocument68 pagesSummary ReportLizanne GauranaPas encore d'évaluation

- Sales Promotion and Customer Awareness of The Services, Standerd Charterd Finance Ltd. by Shiv Gautam - MarketingDocument67 pagesSales Promotion and Customer Awareness of The Services, Standerd Charterd Finance Ltd. by Shiv Gautam - MarketingRishav Ch100% (1)

- The Accounts 002 MTDocument40 pagesThe Accounts 002 MTIan BelmontePas encore d'évaluation

- MT2 App1Document8 pagesMT2 App1api-3725162Pas encore d'évaluation

- Cash & Cash Equivalent Lecture NotesDocument6 pagesCash & Cash Equivalent Lecture NotesRena Lyn ManzanoPas encore d'évaluation

- Comprehensive Problem 2Document4 pagesComprehensive Problem 2Nicole Anne Santiago SibuloPas encore d'évaluation

- Training - Term LoanDocument33 pagesTraining - Term Loancric6688Pas encore d'évaluation

- Intermediate Accounting 2 First Grading ExaminationDocument12 pagesIntermediate Accounting 2 First Grading ExaminationJamie Rose AragonesPas encore d'évaluation

- Fundamentals of Accountancy, Business and Management 1 (Second Quarter)Document67 pagesFundamentals of Accountancy, Business and Management 1 (Second Quarter)Niña Gloria Acuin ZaspaPas encore d'évaluation

- Week6 AComprehensiveIllustrationDocument86 pagesWeek6 AComprehensiveIllustrationyow jing pei89% (28)

- Accounting Dashboard: Dashboard WP ERP Accounting. Once You Get There You Will See The FollowingDocument40 pagesAccounting Dashboard: Dashboard WP ERP Accounting. Once You Get There You Will See The FollowingusmanPas encore d'évaluation

- Partnership Reading MaterialDocument4 pagesPartnership Reading MaterialLawish KumarPas encore d'évaluation

- Basics Accounting PrinciplesDocument22 pagesBasics Accounting PrincipleshsaherwanPas encore d'évaluation

- Subsidiary Ledgers and Control AccountsDocument4 pagesSubsidiary Ledgers and Control AccountsHafidzi DerahmanPas encore d'évaluation

- Unpacking Bleisure - Traveler TrendsDocument39 pagesUnpacking Bleisure - Traveler TrendsTatianaPas encore d'évaluation

- Nature and Formation of Partnership - 2021Document6 pagesNature and Formation of Partnership - 2021LLYOD FRANCIS LAYLAYPas encore d'évaluation

- Account TitlesDocument28 pagesAccount TitlesEfrelyn Grethel Baraya Alejandro100% (1)

- Internship ReportDocument75 pagesInternship ReportAsma AzamPas encore d'évaluation

- Pretest L1 FloristDocument5 pagesPretest L1 FloristnisasuriantoPas encore d'évaluation

- Fedwire Funds Format Reference GuideDocument19 pagesFedwire Funds Format Reference GuideMakarand Lonkar100% (1)