Vous aimerez peut-être aussi

- Lean for Service Organizations and Offices: A Holistic Approach for Achieving Operational Excellence and ImprovementsD'EverandLean for Service Organizations and Offices: A Holistic Approach for Achieving Operational Excellence and ImprovementsPas encore d'évaluation

- Creating a Balanced Scorecard for a Financial Services OrganizationD'EverandCreating a Balanced Scorecard for a Financial Services OrganizationPas encore d'évaluation

- UntitledDocument376 pagesUntitledpoobalanipbPas encore d'évaluation

- Ratios Analysis: Lahore Leads UniversityDocument24 pagesRatios Analysis: Lahore Leads UniversityZee ShanPas encore d'évaluation

- Financial Statement Analysis of HDFC BankDocument58 pagesFinancial Statement Analysis of HDFC BankArup SarkarPas encore d'évaluation

- Mba8101: Financial and Managerial Accounting Financial Statement Analysis BY Name: Reg No.: JULY 2014Document9 pagesMba8101: Financial and Managerial Accounting Financial Statement Analysis BY Name: Reg No.: JULY 2014Sammy Datastat GathuruPas encore d'évaluation

- Financial PlanDocument15 pagesFinancial PlanIshaan YadavPas encore d'évaluation

- Annual Report 2010Document281 pagesAnnual Report 2010gogiadhirajPas encore d'évaluation

- Annual Report 2010 11Document80 pagesAnnual Report 2010 11infhraPas encore d'évaluation

- Financial Accounting & AnalysisDocument6 pagesFinancial Accounting & AnalysisAmandeep SinghPas encore d'évaluation

- M/S Multimetals LTD., Kota: A Presentation ofDocument23 pagesM/S Multimetals LTD., Kota: A Presentation ofmanishbansalkotaPas encore d'évaluation

- Finanicial Analysis ThomscookDocument45 pagesFinanicial Analysis ThomscookAnonymous 5quBUnmvm1Pas encore d'évaluation

- Target: Our Brand PromiseDocument26 pagesTarget: Our Brand Promisejennmai85Pas encore d'évaluation

- Macro Perspective: Pakistan Leasing Year Book 2009Document7 pagesMacro Perspective: Pakistan Leasing Year Book 2009atifch88Pas encore d'évaluation

- File 28052013214151 PDFDocument45 pagesFile 28052013214151 PDFraheja_ashishPas encore d'évaluation

- Managerial Accounting FiDocument32 pagesManagerial Accounting FiJo Segismundo-JiaoPas encore d'évaluation

- Suggested Answer - Syl2012 - Jun2014 - Paper - 20 Final Examination: Suggested Answers To QuestionsDocument16 pagesSuggested Answer - Syl2012 - Jun2014 - Paper - 20 Final Examination: Suggested Answers To QuestionsMdAnjum1991Pas encore d'évaluation

- Strategic Financial Management: Presented By:-Rupesh Kadam (PG-11-084)Document40 pagesStrategic Financial Management: Presented By:-Rupesh Kadam (PG-11-084)Rupesh KadamPas encore d'évaluation

- Axis 2013Document212 pagesAxis 2013Abhishek AroraPas encore d'évaluation

- Annual Report 2013 Axis BankDocument211 pagesAnnual Report 2013 Axis BankRahul PagariaPas encore d'évaluation

- AssignmentDocument10 pagesAssignmentahmadfaiq01Pas encore d'évaluation

- Financial Analysis of The Surat Mercantile Co-Op. Bank LTD."Document19 pagesFinancial Analysis of The Surat Mercantile Co-Op. Bank LTD."Ankur MeruliyaPas encore d'évaluation

- Company: IDFC Project Cost Years 2003 2004 2005 2006 2007 2008 2009 2010 ProjectedDocument68 pagesCompany: IDFC Project Cost Years 2003 2004 2005 2006 2007 2008 2009 2010 Projectedsumit_sagarPas encore d'évaluation

- Searle Company Ratio Analysis 2010 2011 2012Document63 pagesSearle Company Ratio Analysis 2010 2011 2012Kaleb VargasPas encore d'évaluation

- Ratio Analysis PrintDocument45 pagesRatio Analysis Printfrancis MagobaPas encore d'évaluation

- ITC Annual ReportDocument19 pagesITC Annual Reportanks0909Pas encore d'évaluation

- IUBAT-International University of Business Agriculture and TechnologyDocument10 pagesIUBAT-International University of Business Agriculture and Technologysajal sahaPas encore d'évaluation

- AXIS Bank AnalysisDocument44 pagesAXIS Bank AnalysisArup SarkarPas encore d'évaluation

- Kbank enDocument356 pagesKbank enchead_nithiPas encore d'évaluation

- Chapter 14 Financial Statement AnalysisDocument40 pagesChapter 14 Financial Statement AnalysisJenalyn OrtegaPas encore d'évaluation

- Analysis & InterpretationDocument34 pagesAnalysis & InterpretationArunKumarPas encore d'évaluation

- Financial StatementDocument115 pagesFinancial Statementammar123Pas encore d'évaluation

- Financial Analysis of Samsung PLCDocument17 pagesFinancial Analysis of Samsung PLCROHIT SETHI90% (10)

- Financial Management: M. Usman 15324Document13 pagesFinancial Management: M. Usman 15324Muhammad UsmanPas encore d'évaluation

- Research Paper On Working Capital Management Made by Satyam KumarDocument3 pagesResearch Paper On Working Capital Management Made by Satyam Kumarsatyam skPas encore d'évaluation

- Walmart ValuationDocument24 pagesWalmart ValuationnessawhoPas encore d'évaluation

- A PresentationDocument28 pagesA PresentationAvantika ViholPas encore d'évaluation

- DELL LBO Model Part 1 CompletedDocument21 pagesDELL LBO Model Part 1 CompletedMohd IzwanPas encore d'évaluation

- What Are Quantitative FactorsDocument5 pagesWhat Are Quantitative FactorsJunaid CheemaPas encore d'évaluation

- Balance Sheet As at 31st March 2012 (Rs in Lakhs)Document20 pagesBalance Sheet As at 31st March 2012 (Rs in Lakhs)Ranu SinghPas encore d'évaluation

- HDFCDocument78 pagesHDFCsam04050Pas encore d'évaluation

- Chap-6 Financial AnalysisDocument15 pagesChap-6 Financial Analysis✬ SHANZA MALIK ✬Pas encore d'évaluation

- Business ProjectDocument16 pagesBusiness Projectlaiba khanPas encore d'évaluation

- FSK ProjectDocument16 pagesFSK Projectlaiba khanPas encore d'évaluation

- Kotak Mahindra Bank Balance Sheet of Last 5 YearsDocument10 pagesKotak Mahindra Bank Balance Sheet of Last 5 YearsManish MahajanPas encore d'évaluation

- TV3 AnalysisDocument3 pagesTV3 AnalysishotransangPas encore d'évaluation

- Annual Report 2011Document233 pagesAnnual Report 2011Khalid FirozPas encore d'évaluation

- Project Titels: Study On Overall Financial Performance of Central Bank of IndiaDocument24 pagesProject Titels: Study On Overall Financial Performance of Central Bank of IndiaVishwas NayakPas encore d'évaluation

- 2011 Annual ReportDocument96 pages2011 Annual ReportOsman SalihPas encore d'évaluation

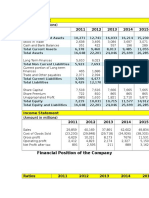

- Financial Position of The Engro FoodsDocument2 pagesFinancial Position of The Engro FoodsJaveriarehanPas encore d'évaluation

- Investment VI FINC 404 Company ValuationDocument52 pagesInvestment VI FINC 404 Company ValuationMohamed MadyPas encore d'évaluation

- Annual Report 07 08Document142 pagesAnnual Report 07 08jagat_sabatPas encore d'évaluation

- Financial Statement AnalysisDocument17 pagesFinancial Statement AnalysisMylene CandidoPas encore d'évaluation

- AuditedStandaloneFinancialresults 31stmarch, 201111121123230510Document2 pagesAuditedStandaloneFinancialresults 31stmarch, 201111121123230510Kruti PawarPas encore d'évaluation

- Ratio Analysis in Business Decisions@ Bec DomsDocument85 pagesRatio Analysis in Business Decisions@ Bec DomsBabasab Patil (Karrisatte)Pas encore d'évaluation

- A&F Assignment 2Document4 pagesA&F Assignment 2Tech PerusalPas encore d'évaluation

- Financial Management Group AssignmentDocument25 pagesFinancial Management Group AssignmentGliten Anand RoyPas encore d'évaluation

- Implementing Beyond Budgeting: Unlocking the Performance PotentialD'EverandImplementing Beyond Budgeting: Unlocking the Performance PotentialÉvaluation : 5 sur 5 étoiles5/5 (1)

- Commercial Bank Revenues World Summary: Market Values & Financials by CountryD'EverandCommercial Bank Revenues World Summary: Market Values & Financials by CountryPas encore d'évaluation

- Working Capital Management: Applications and Case StudiesD'EverandWorking Capital Management: Applications and Case StudiesÉvaluation : 4.5 sur 5 étoiles4.5/5 (4)

- In The Helen Galope Matter - Plaintiffs Revised Statement of Genuine IssuesDocument28 pagesIn The Helen Galope Matter - Plaintiffs Revised Statement of Genuine Issues83jjmack100% (1)

- RESPA Letter To GreentreeDocument19 pagesRESPA Letter To GreentreeMark R.Pas encore d'évaluation

- File BRPD Circular No 05Document3 pagesFile BRPD Circular No 05Arifur RahmanPas encore d'évaluation

- 2015 SALN Form - (Blank)Document4 pages2015 SALN Form - (Blank)ENRICO SANORIA PALER, M.A.Pas encore d'évaluation

- Abella Vs Abella DigestDocument2 pagesAbella Vs Abella DigestJasielle Leigh UlangkayaPas encore d'évaluation

- Securities Lending Best Practices Mutual Funds 2012Document20 pagesSecurities Lending Best Practices Mutual Funds 2012swinki3Pas encore d'évaluation

- Leonardo Bognot V RRI Lending CorporationDocument10 pagesLeonardo Bognot V RRI Lending CorporationMarchini Sandro Cañizares KongPas encore d'évaluation

- A Study On Bancassurance at State Bank of India, AgraDocument108 pagesA Study On Bancassurance at State Bank of India, AgrasuryakantshrotriyaPas encore d'évaluation

- Hamilton Properties and CitySquare Sue Dallas City HallDocument72 pagesHamilton Properties and CitySquare Sue Dallas City HallRobert WilonskyPas encore d'évaluation

- LTD Finals Reviewer (Sec. 93-117)Document5 pagesLTD Finals Reviewer (Sec. 93-117)Florence RosetePas encore d'évaluation

- Bank of Maharashtra ProjectDocument32 pagesBank of Maharashtra Projectpratik kitlekar100% (1)

- HSBC Branchless BankingDocument5 pagesHSBC Branchless BankingSKSAIDINESHPas encore d'évaluation

- Bank Accounts and Credit SecuritiesDocument13 pagesBank Accounts and Credit SecuritiesJay Alcain OrpianoPas encore d'évaluation

- Topic 2 - BondDocument53 pagesTopic 2 - BondHamdan HassinPas encore d'évaluation

- Form X-17A-5 Part Iia (FOCUS Report) : General InstructionsDocument8 pagesForm X-17A-5 Part Iia (FOCUS Report) : General InstructionshighfinancePas encore d'évaluation

- Role of Central Bank With Special Reference To The Nepal Rastra BankDocument2 pagesRole of Central Bank With Special Reference To The Nepal Rastra BankShambhav Lama100% (1)

- Hemedes v. CA DigestDocument3 pagesHemedes v. CA DigestDonvidachiye Liwag CenaPas encore d'évaluation

- RMK 354 - Construction Law Apr May 2010.Document4 pagesRMK 354 - Construction Law Apr May 2010.Amran'sDaughterPas encore d'évaluation

- Times Leader 07-18-2011Document40 pagesTimes Leader 07-18-2011The Times LeaderPas encore d'évaluation

- 17.MARK-monserrat Vs CeronDocument2 pages17.MARK-monserrat Vs CeronbowbingPas encore d'évaluation

- Quiz - QUIZ 1Document17 pagesQuiz - QUIZ 1Jimbo ManalastasPas encore d'évaluation

- MILAGROS HOMEOWNERS ASSOCIATION Registered at Social Housing FinanceDocument2 pagesMILAGROS HOMEOWNERS ASSOCIATION Registered at Social Housing FinanceLelaine RicoPas encore d'évaluation

- UN, Land Admin in UNECE Region, Dev Trends & Main PrinciplesDocument112 pagesUN, Land Admin in UNECE Region, Dev Trends & Main PrinciplesConnie Lee Li TingPas encore d'évaluation

- Annual Report 2008 PDFDocument83 pagesAnnual Report 2008 PDFDhivya SivananthamPas encore d'évaluation

- The New Math of Reverse Mortgages For Retirees - WSJ (June 2022)Document5 pagesThe New Math of Reverse Mortgages For Retirees - WSJ (June 2022)ejbejbejbPas encore d'évaluation

- Not PrecedentialDocument10 pagesNot PrecedentialScribd Government DocsPas encore d'évaluation

- Presentation, Results and Discussion: Facing Legal Consequences in Performing Money Lending BusinessDocument13 pagesPresentation, Results and Discussion: Facing Legal Consequences in Performing Money Lending BusinessDiana Faye CaduadaPas encore d'évaluation

- QBE Corporate BrochureDocument13 pagesQBE Corporate BrochureQBE European Operations Risk ManagementPas encore d'évaluation

- ObliCon Cases 3rd ExamDocument140 pagesObliCon Cases 3rd ExamJennica Gyrl G. DelfinPas encore d'évaluation

- Death Notification ChecklistDocument3 pagesDeath Notification ChecklistAnonymous zGFqoXPas encore d'évaluation