Vous aimerez peut-être aussi

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsD'EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsÉvaluation : 5 sur 5 étoiles5/5 (1)

- 0 C 58 Cea 5Document16 pages0 C 58 Cea 5ayaPas encore d'évaluation

- AnswersDocument11 pagesAnswersEkin SapianPas encore d'évaluation

- 8sgp 2005 Dec ADocument10 pages8sgp 2005 Dec Aapi-19836745Pas encore d'évaluation

- Chapter 6Document8 pagesChapter 6Jesther John VocalPas encore d'évaluation

- Chapter 12 Example Questions ANSWERDocument9 pagesChapter 12 Example Questions ANSWERSavy DhillonPas encore d'évaluation

- Audit Final Exam (2021)Document4 pagesAudit Final Exam (2021)Falay MemPas encore d'évaluation

- Before Commencing The Audit WorkDocument4 pagesBefore Commencing The Audit WorkFalay MemPas encore d'évaluation

- Auditing Part 3Document10 pagesAuditing Part 3Trisha BanzonPas encore d'évaluation

- Audit 1Document6 pagesAudit 1Goi Cai EnPas encore d'évaluation

- T8uk 2009 Jun ADocument8 pagesT8uk 2009 Jun AKläRens AhiaborPas encore d'évaluation

- How Do Different Levels of Control Risk in The RevDocument3 pagesHow Do Different Levels of Control Risk in The RevHenry L BanaagPas encore d'évaluation

- Quiz Auditing II Before Midtest Ubakrie April 23, 2021Document9 pagesQuiz Auditing II Before Midtest Ubakrie April 23, 2021Wisnu Aldi WibowoPas encore d'évaluation

- GORISK330-C08 Discussion No. 1 - Suggested Answers Case No. 1 The Following Short Cases Describe Some Specific Internal Control WeaknessesDocument8 pagesGORISK330-C08 Discussion No. 1 - Suggested Answers Case No. 1 The Following Short Cases Describe Some Specific Internal Control WeaknessesMa Tiffany Gura RoblePas encore d'évaluation

- Week 10Document5 pagesWeek 10Anonymous lGgyXRNvgBPas encore d'évaluation

- AnswerDocument8 pagesAnswerRaselPas encore d'évaluation

- Chapter 5Document20 pagesChapter 5temedeberePas encore d'évaluation

- 10 Auditing The Expenditure CycleDocument9 pages10 Auditing The Expenditure CycleJude AlbaniaPas encore d'évaluation

- Chapter 11 Audit of Acquisi-1Document39 pagesChapter 11 Audit of Acquisi-1Vianney Claire RabePas encore d'évaluation

- Chapter 9: Auditing The Revenue CycleDocument42 pagesChapter 9: Auditing The Revenue CycleSweet Emme100% (1)

- Auditing The Revenue CycleDocument63 pagesAuditing The Revenue CycleJohn Lexter MacalberPas encore d'évaluation

- Identify An Internal Control Procedure That Would Reduce The Following Risks in A Manual SystemDocument2 pagesIdentify An Internal Control Procedure That Would Reduce The Following Risks in A Manual SystemArthenemis FortalejoPas encore d'évaluation

- Auditing PDF 1.1Document18 pagesAuditing PDF 1.1anilanitha974Pas encore d'évaluation

- Tutorial 3 Chapter 3 Fraud, Ethics and Internal ControlsDocument4 pagesTutorial 3 Chapter 3 Fraud, Ethics and Internal ControlsWael Ayari0% (1)

- Baf Ii-Tutorial QuestionsDocument15 pagesBaf Ii-Tutorial Questionsrobinkaby06Pas encore d'évaluation

- IC3 Audit Procedures by Transaction Cycle Part 1Document12 pagesIC3 Audit Procedures by Transaction Cycle Part 1ReynaLyn TangaranPas encore d'évaluation

- Auditing Principles and Practice IiDocument4 pagesAuditing Principles and Practice IiDavid TPas encore d'évaluation

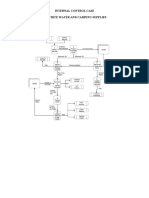

- Outdoor Adventure: White Water and Camping Supplies A. Data Flow DiagramDocument8 pagesOutdoor Adventure: White Water and Camping Supplies A. Data Flow DiagramShi GiananPas encore d'évaluation

- NAMEDocument7 pagesNAMEMarinella LosaPas encore d'évaluation

- Q3 MJ18 DavisDocument2 pagesQ3 MJ18 DavisFarPas encore d'évaluation

- Aguila, Paulo Timothy - Cis c10Document5 pagesAguila, Paulo Timothy - Cis c10Paulo Timothy AguilaPas encore d'évaluation

- IT Audit 4ed SM Ch9Document62 pagesIT Audit 4ed SM Ch9randomlungs121223Pas encore d'évaluation

- IT Audit 4ed SM Ch9Document62 pagesIT Audit 4ed SM Ch9randomlungs121223Pas encore d'évaluation

- ABC Internal Controls PDFDocument2 pagesABC Internal Controls PDFice manga100% (3)

- Chap 010Document73 pagesChap 010Amit JindalPas encore d'évaluation

- Marks Q.1 (A) Risk Associated With Revenue and General Operations: (Any Six at 1 Mark Each)Document7 pagesMarks Q.1 (A) Risk Associated With Revenue and General Operations: (Any Six at 1 Mark Each)sohail merchantPas encore d'évaluation

- Test 1 - 2022Document3 pagesTest 1 - 2022Ten Lee0% (1)

- Discussion QuestionsDocument3 pagesDiscussion QuestionsAzelie JuddPas encore d'évaluation

- Aguila, Paulo Timothy - Cis c9Document3 pagesAguila, Paulo Timothy - Cis c9Paulo Timothy AguilaPas encore d'évaluation

- Aactg16a Final Exam - Canceran, Michelle M.Document5 pagesAactg16a Final Exam - Canceran, Michelle M.Michelle Manalo Canceran100% (1)

- Auditing The Expenditure CycleDocument56 pagesAuditing The Expenditure CycleJohn Lexter Macalber100% (1)

- FMGT 3310 Midterm ReviewDocument12 pagesFMGT 3310 Midterm ReviewAndre WardPas encore d'évaluation

- A. Data Flow Diagram: Internal Control Case 6. Outdoor Adventure: White Water and Camping SuppliesDocument4 pagesA. Data Flow Diagram: Internal Control Case 6. Outdoor Adventure: White Water and Camping SuppliesShi GiananPas encore d'évaluation

- HW 4.24 9.26 9.18Document2 pagesHW 4.24 9.26 9.18lephanminhthu.34Pas encore d'évaluation

- Audit 101Document3 pagesAudit 101Jonard AlterPas encore d'évaluation

- True False QuestionDocument3 pagesTrue False Question공부Pas encore d'évaluation

- F20Document7 pagesF20Zubair KhanPas encore d'évaluation

- AUDITINGDocument3 pagesAUDITINGSharn Linzi Buan MontañoPas encore d'évaluation

- Acctg 16a Final Exam AnswerDocument4 pagesAcctg 16a Final Exam AnswerLy JaimePas encore d'évaluation

- Biltrite Case Module I Through X 04 16 2014Document8 pagesBiltrite Case Module I Through X 04 16 2014nknknknPas encore d'évaluation

- GOVBUSMAN MODULE 9 (12) - Chapter 15Document4 pagesGOVBUSMAN MODULE 9 (12) - Chapter 15Rohanne Garcia AbrigoPas encore d'évaluation

- Discussion Question:: 1. What Documents Constitute The AP Packet? What Evidence Does Each Document Provide?Document4 pagesDiscussion Question:: 1. What Documents Constitute The AP Packet? What Evidence Does Each Document Provide?Rizza L. MacarandanPas encore d'évaluation

- HowtoidentifyariskDocument5 pagesHowtoidentifyariskHitekani ConsolationPas encore d'évaluation

- Aud Su7Document39 pagesAud Su7Jane GavinoPas encore d'évaluation

- 427 Final Spring 2021Document2 pages427 Final Spring 2021MD SomratPas encore d'évaluation

- Auditing and Assurance ServicesDocument69 pagesAuditing and Assurance Servicesgilli1tr100% (1)

- ACCTG16A FinalExamDocument5 pagesACCTG16A FinalExamJeane BongalanPas encore d'évaluation

- Textbook of Urgent Care Management: Chapter 13, Financial ManagementD'EverandTextbook of Urgent Care Management: Chapter 13, Financial ManagementPas encore d'évaluation

- Inventory Accounting: A Comprehensive GuideD'EverandInventory Accounting: A Comprehensive GuideÉvaluation : 5 sur 5 étoiles5/5 (1)

- Psychopathy Is The Unified Theory of CrimeDocument18 pagesPsychopathy Is The Unified Theory of Crimebıind jonnPas encore d'évaluation

- Institutional Correction SyllabusDocument16 pagesInstitutional Correction SyllabusLeslie May Cardines AntonioPas encore d'évaluation

- Digest of Maniago v. CA (G.R. No. 104392)Document2 pagesDigest of Maniago v. CA (G.R. No. 104392)Rafael Pangilinan50% (2)

- NTF ELCACAccomplishment Report August 2023Document12 pagesNTF ELCACAccomplishment Report August 2023cictmu.bcpoPas encore d'évaluation

- 2010 Health Care Fraud Annual ReportDocument43 pages2010 Health Care Fraud Annual ReportMike DeWinePas encore d'évaluation

- Art 212 Pub OfficialsDocument3 pagesArt 212 Pub OfficialsJustine M.Pas encore d'évaluation

- Attachment A - Letter To Nevada Commission On Judicial DisciplineDocument4 pagesAttachment A - Letter To Nevada Commission On Judicial DisciplineRiley SnyderPas encore d'évaluation

- Jimmy Savile Sexual Abuse ScandalDocument16 pagesJimmy Savile Sexual Abuse ScandalMercilessTruth0% (1)

- PEOPLE Vs Montinola DigestDocument3 pagesPEOPLE Vs Montinola DigestEric Pajuelas Estabaya100% (1)

- Chapter 3Document31 pagesChapter 3chanikyaPas encore d'évaluation

- Sree Rayalaseema Hi-Strength Hypo LTD.: GroupDocument2 pagesSree Rayalaseema Hi-Strength Hypo LTD.: GroupRantyPas encore d'évaluation

- Death Penalty: Going Beyond Moral Claims Ivan James Francisco Tuazon, BSC 1FDocument4 pagesDeath Penalty: Going Beyond Moral Claims Ivan James Francisco Tuazon, BSC 1FIvan James Francisco TuazonPas encore d'évaluation

- Lancaster County Warrant SweepDocument2 pagesLancaster County Warrant SweepPennLivePas encore d'évaluation

- 11Document346 pages11kuntal854uPas encore d'évaluation

- Beautiful Red Krovvy: The Violence in A Clockwork OrangeDocument8 pagesBeautiful Red Krovvy: The Violence in A Clockwork OrangePadla NemeckovaPas encore d'évaluation

- Eoi 101Document7 pagesEoi 101Yusuf MunnaPas encore d'évaluation

- Lecture Notes BT 3-1 LawDocument117 pagesLecture Notes BT 3-1 LawE-Lie Nartey100% (1)

- Bonifacio V EraDocument1 pageBonifacio V EraAndrew NacitaPas encore d'évaluation

- Ranger Academy Information and ApplicationDocument17 pagesRanger Academy Information and ApplicationBill DeWeesePas encore d'évaluation

- People vs. Nicolas Guzman y Bocbosila. - DigestDocument2 pagesPeople vs. Nicolas Guzman y Bocbosila. - DigestHazel KatipunanPas encore d'évaluation

- Crimpro 115.Document125 pagesCrimpro 115.Reyleyy1Pas encore d'évaluation

- Constitutional Law II - Arrest Searches and SeizuresDocument6 pagesConstitutional Law II - Arrest Searches and SeizuresKhryz CallëjaPas encore d'évaluation

- People v. MandoladoDocument2 pagesPeople v. MandoladoVia Rhidda Imperial100% (1)

- Text 28Document3 pagesText 28api-272517869Pas encore d'évaluation

- 2015-06 Power To Arrest Training ManualDocument83 pages2015-06 Power To Arrest Training ManualchieflittlehorsePas encore d'évaluation

- Affidavit CourtDocument11 pagesAffidavit Courtjoe100% (10)

- 2015-06-11 Calvert County TimesDocument24 pages2015-06-11 Calvert County TimesSouthern Maryland OnlinePas encore d'évaluation

- Julian The Apostate - Gaetano Negri Transl 1905 - Vol 2Document338 pagesJulian The Apostate - Gaetano Negri Transl 1905 - Vol 2Kassandra M Journalist100% (1)

- Odontology: Forensic ServicesDocument2 pagesOdontology: Forensic ServicesIntan FajrinPas encore d'évaluation

- (DLB) (HC) Braley v. Wasco State Prison, Et Al. - Document No. 4Document2 pages(DLB) (HC) Braley v. Wasco State Prison, Et Al. - Document No. 4Justia.comPas encore d'évaluation